The Subject line of the Outcome of Board Meeting submitted on August 20, 2016 inadvertently read as “Outcome of Board Meeting - Reduction of Capital”. It should have only read as “Outcome of Board Meeting”.

Today again new pledge created. Though the % is not big and still it does not negate the unpledgeing of shares recently.

0.86% shares pledged. Now, 4.48% are pledged. Reason given for pledge: short term loan.

Overall, something big is happening there. Unpleasant or pleasant!!!

Don’t company has cash?

257143 shares multiplied by 107 is equal to Rs 27,514,301. It is 2.75 crores.

Why SAST news is not captured in disclosures on BSE? I used to see it there.

News: Trigyn Technologies Ltd has informed BSE regarding a Press Release dated August 29, 2016 titled “Empanelment by Andhra Pradesh State Fibrenet Limited (APSFL) as one of the Vendor for Procurement of Customer Premise Equipment (CPE) for Delivery of Triple Play Services - Internet, Telephone, IPTV or CATV & Value Added Services (On Rate Contract)”.

Management expects to add 35-40 cr revenue in first year due to the above news.

Management says other states are also working on same line and confident of winning more.

Andhra order can add Rs 35-40cr to revenue in first year: Trigyn

(Speaking to CNBC-TV18, R Ganapathi, Chairman and Executive Director of Trigyn Technologies said this order can add Rs 35-40 crore to revenue in first year)

I talked to CS earlier and he informed me that this the reason why they are amending object clause in line with that of Wipro to participate in such proposals where they think they have the expertise. Now it stands verified.

Any detailed description/presentation on Trigyn Tech. So that i can understand the company’s business in detail. Thanks

Mohammed bro, I agree that OCF was pretty low before 2016 despite Trigyn posting good increasing profits year after year. I was trying to dig as to where the cash was being consumed prior to 2016. Can you please point where should i look? Current liabilities prior to 2016? Or somewhere else?

Currently, they have bank balance/cash in hand around 60 odd cr, and is trading at 315 cr mkt cap.

Br Mridul

Br Hemant CA has done great analysis in this thread at the top. Please look at his post dated Feb 14 detailing the liquidation of subsidiaries.

I have gone through the whole thread and already and have understood the narrative (company’s distressed position and winding up of subsidiaries). My question is more in terms of the accounting entries for write offs or paying of contingent liabilities due to liquidations and stuff. From one of Hemant’s posts -

“As a part of this whole exercise, as specified on page 47 of the FY2013 AR, Provision for diminution was made for 603 cr as against the required 649 cr. Balance would be around 45 - 46 cr.”

So these are contingent liabilities or does it come under some other accounting head?

Also, i see that there is still over 50 cr of contingent liabilities at present. Do you know what are those?

From the recent Annual Report -

“to reduce

the Securities Premium Account of the Company amounting to Rs. 661,02,27,115 /- (Rupees Six Hundred and Sixty one Crore Two Lakhs Twenty Seven Thousand One Hundred and Fifteen only), that such reduction be effected by writing off the accumulated losses in full amounting to Rs. 528,25,91,328/- (Rupee Five Hundred and Twenty Eight Crore Twenty Five lakhs Ninety one Thousand Three Hundred and Twenty Eight only) to give true and fair view of books of accounts of the Company”

How is this going to impact the balance sheet? And how does this impact existing shareholders? On further digging the annual report -

“OBJECTS/ BENEFITS ARISING OUT OF THE SCHEME

a. Under this Scheme, if approved, the Company will represent true financial position which would benefit both shareholders as their holding will yield better results and value and also enable the Company to explore opportunities to benefit of the shareholders of the Company including in the form of dividend payment as per the applicable provisions of the Act.

b. The adjustment/set off, of the Securities Premium Account would not have any impact on the shareholding pattern, and the capital structure of the Company.

c. The Scheme does not involve any financial outlay / outgo and therefore, would not affect the ability or liquidity of the Company to meet its obligations/ commitments in the normal course of business. Further, this Scheme would also not in any way adversely affect the ordinary operations of the Company.

d. The Scheme, if approved, may enable the Company to foresee business opportunity that it may be unable to take advantage because of it experiencing Accumulated Losses.

e. The proposed Scheme will enable the Company to use the amount which is lying unutilized in the Securities Premium Account of the Company in an effective manner for the benefit of the Company.

f. The true financial statement of the Company would ensure the Company to expand & smoothen the business activity and to attract new source of avenue and in turn enhancement of its shareholders’ value.”

So this is merely an accounting entry? What will be the impact on the balance sheet and Profit & Loss stmt post this reduction?

Dear Mridul

Where is contingent liability of 50 cr ?

Scheme as said will have no impact on the balance sheet. Old liquidations being cleared from the book after getting RBI etc approvals. There is debit and credit entry on the liability side only. This should clear up the balance sheet and make it simple and easy to read from now on.

From HDFC Sec report

Recent proposal to write off the accumulated losses against share premium account could enable the company to start paying dividends

The Company has Accumulated Losses reflecting in the books of the Company, from the previous years, primarily, due to diminution in value of investments made in the year 2000. As on 31 March 2016, as per the audited financial results of the Company, the Accumulated Losses amounts to Rs. 528,25,91,328/- represented as ‘Deficit in Statement of Profit & Loss’ in the Reserves & Surplus Account. Further, the Company also has balance in the Securities Premium Account amounting to Rs. 661,02,27,115/- as on 31 March 2016. The Board of Directors of the Company has proposed to write-off the Accumulated Losses amounting to Rs. 528,25,91,328/- reflecting in the book of the Company, by reducing the amount standing to the credit of the Securities Premium Account from Rs. 661,02,27,115/- to Rs. 132,76,35,787/- as on 31 March 2016. Under this Scheme, if approved, the Company will represent true financial position which would benefit both shareholders as their holding will yield better results and value and also enable the Company to explore opportunities to benefit of the shareholders of the Company including in the form of dividend payment as per the applicable provisions of the Act. The true financial statement of the Company would ensure the Company to expand & smoothen the business activity and to attract new source of avenue and in turn enhancement of its shareholders’ value.

HDFC Report

Thanks for the HDFC Report.

Yeah, i understood that capital reduction is merely an accounting entry. May be capital reduction here is a misnomer (as it is reducing securities premium a/c), not the actual share capital?

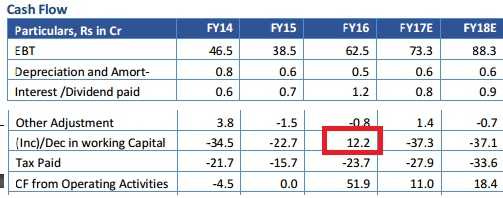

Question on Operating cash flow- As per screener, working capital is increasing from 2015 → 2016 ( by 44 odd cr)

Here in HDFC report, is isn’t mathcing (see red highlighted box)

What is there that i am missing?

Also, how is Trump Presidency going to impact Trigyn (considering) a lot of revenues here are coming from US government bodies? Any insights?

I think the screener Working Capital does not reflect the correct picture as it takes only other asset and other liability for its calculation. HDFC report has taken directly from AR 16 page 95 and I think that is the true reflection.

This company is American Centric and so any policy changes due to Trump would have an impact. That is one major risk for this company. Company is diversifying its geography like having more domestic business in the future.

Let apart screener. Look at page 93 of annual report -

working capital = curr. assets - curr. liabilities

2016 → 220-57 = 163 cr (2016)

2015 → 172-50 = 122 cr (2015)

Shouldn’t the change in working capital be 41 cr (increase)…

Regarding Trump,i am wary! The way he has given his inauguration speech, there is certainly going to have an impact on Indian IT companies if globalization takes a back seat.

Dear Mridul

You are technically right I think. But the point to be noted is that the Working Capital theoretically has gone up mainly because of cash going up from 11 to 66 cr from 2015 to 2016 which in itself is a great sign. Receivable going down and payable going up itself is a sign that working capital requirement situation has improved favourably for the company. This despite good increase in revenue.

Look at Sept 2016 half yearly results and picture becomes even more rosy.

Receivable has remained same but payable has gone up and cash has gone up further to 86 cr. This analysis makes me even more bullish on the business. Thanks for motivating me to look deeper.

2 Likes

I agree… The Sep’16 picture looks even better from Mar’16 one…

Based on all the analysis, the stock still looks super undervalued at this point in time …

There will be several triggers in the coming months such as possible dividend pay-out, receiving of some new orders, etc

However, IT with focus especially on the US markets is under stress because of Trump’s words.

Disc: Invested from low levels with high expectations !!

1 Like

Trigyn Tech USA wins a 3 years contract from new York City Financial services Agency. This could get extended to a 9 year contract. Trigyn 29th Apr.pdf (97.0 KB)

Scheme of Reduction of Share Capital by virtue of Section 100 to 104 of Companies Act, 1956 and Section 52 of Companies Act, 2013 has been approved by the National Company Law Tribunal (‘NCLT’)

below is the link of the same-

http://www.bseindia.com/corporates/ann.aspx?scrip=517562&dur=A&expandable=0

It will be great if some one can throw some light on this topic, I am unable to understand this.

Thank you

Dear @suru27 and @phreakv6 , you both have a good command on these Tech Companies. Can you guide here on this company if you have looked at it in past or so.

My findings were not enough to say that the company is cooking up but certain things looks strange

- Auditors of trigyn is same as that of Gitanjali Gems.

- They give Interest free loans to subsidiaries and then write off the same. Lot of subsidiaries liquidated in past.

- Lot of revenue comes from the subsidiaries as like that of 8k Miles but can not find anything from Auditor’s Notes that which subsidiaries are audited by them and their corresponding revenue share.

- Managerial Remuneration is very high and company use stock options of 2.5 Lakh at Rs 10 a share each to 2 main persons. While it issue only 50000 shares to the employees as stock option.

On linkedin , Company has around 750 employees so people are definitely working here.

2 Likes

Even though point no 1 itself is enough to stay away and rest of points second the stance, let us go ahead. Usually, I try to go in history and find patterns. Long term price chart is 1 such indicator. Have never come across this company earlier, so, starting from scratch

So, looks like they doomed in IT bubble. So, IT sector was an opportunity which capable Indian IT companies have leveraged it well but this company failed and then from 2002 to 2014 nothing and again there is a renewed interest. So, this period of 1999 to 2002 is very important as 90% wealth was lost. What happened? Unfortunately, companies website does not have annual reports exactly before 2003. Not sure if it is a coincidence.

Also, will you like to ride on a management which has spent more than a decade doing nothing? Looks at ARs from 2003 which is available.

Now, let us take more academically.

As per 2018 AR, count of permanent employees is

Total employee expense:

Have not seen employees taking such salaries home and dont think bulk of salaries are going to contract employees if there are any ![]()

High goodwill is another common thread between all these unique IT companies ![]() With your points and above few points, do not see point spending more time .

With your points and above few points, do not see point spending more time .

Also, with so much of cash n 0 other incomes. Not worth digging in my opinion. Let it become another multibagger. Thanks @bharat19 for educating about one more company ![]()

5 Likes