I have looked at few data and based on that I think TBZ is going to have a very good Q4 1.Lower Base in FY16Q4

TBZs last year Q4 took a big hit because of few things : -

a).Jewelers strike which started on 2nd of march and lasted for whole march and went beyond till April End

I have observed TBZ store being closed that time

So basically sales happened for only two months

b).Lower gold price

Jan 2016

Lowest Gold Price on 01 January 2016

24,910

24 Karat - Rs/10gm

Highest Gold Price on 28 January 2016

26,851

24 Karat - Rs/10gm

Lowest Gold Price on 01 February 2016

26,633

24 Karat - Rs/10gm

Highest Gold Price on 12 February 2016

29,976

Gold price in January was very less last year.(It had good recovery in feb)

It would have causes Inventory loss and also loss of revenue on making charges .

Poor wedding season

Q4 2016 seen very few weddings. From April 2015 to Nov 2016 there were a very few wedding muhurats .

Since TBZs most of the revenue comes from wedding jewellery ,less wedding had also caused lower revenue

All these points had a big multiplier impact on TBZ revenue

2.Forecast of Good sale

1.Gold price are bit stable now

2.Wedding season

3.Festive season

3.Migration to Organized sector Player

I am recently observing a shift to the organized players .

There are lots of reasons for that :-

a).Demonetization

b).Trust level of organized players

c).Consumer behavior shift because of better designs

For a long term investment TBZ still looks like a wait and watch story There are few things which needs to be watched every quarter : -

A).Management is talking about reducing working capital

They are taking various steps to do this : -

Improve inventory management

2 .Increasing Gold on Loan which reduces effective Interest rate

B).Expansion Plan

They are planning to expand to more cities with a hybrid model of Company Owned stores and Franchisee stores . Let see how this expansion plan goes . Usually it takes 24- 30 months to turn a store into a good shape (Read somewhere in conference call ,though not sure)

So basically its all depends on working capital management and execution of expansion (And of-course stable gold price)

Disclosure : - I am invested for the short term bet. At the same time I am keenly watching the developments and would be interested for long term. At the same time Thangamayil looks a better long term story .The hing I liked about thangamayil is their inventory management . They have one of the best inventory management in jewelry sector.

Hello Friends, Now that PCJ and Gitanjali got stuck for their reasons which most know and Titan trading at such high valuation. Last few quarters i could see franchise led business is been showing a uptick and new shops in mall to target retail customer is showing some traction and management is putting effort to improve overall business although numbers are yet to impress with close to 5% sales growth. I see from Nov onwards no has been talking about this business which has the most unorganized players. There was news on hall marking to be made compulsory and draft guidelines were supposed to be released by Jan. I would appreciate if senior member from the group share their thoughts on the same.

Disclosure: I don’t hold any position in the above company.

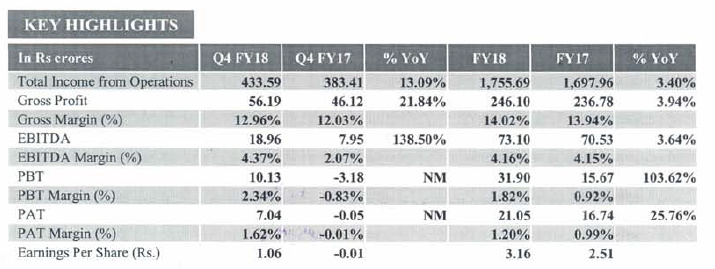

The total income from operations during Q4 FY18 grew 13.09% YoY to Rs. 433.59 crores. Q4

FY18 EBITDA grew 138.50% YoY to Rs. 18.96 crores with an EBITDA margin of 4.37%. Q4

FY18 PBT grew to Rs. 10.13 crores with a PBTmargin of2.34%. Q4 FY18 PAT grew to Rs. 7.04

crores with a PAT margin of 1.62%.

The total income from operations during FY18 grew 3.40% YoY to Rs. 1,755.69 crores. FY18

EBITDA grew 3.64% YoY to Rs. 73.10 crores with an EBITDA margin of 4.16%. FY18 PBT grew

103.62% YoY to Rs. 31.90 crores with a PBT.

Mr. Shrikant Zaveri, Chairman and Managing Director of the company stated that “The fourth

quarter displayed healthy revenue growth on the back of ongoing wedding season. The new range

of gold and diamond jewellery designs for the wedding season received an encouraging response

from the customers. Our operational profitability and cash flows improved in line with the revenues

whilst we maintained strict control on operating costs. We opened our 3ih store in Phoenix Market

City Mall, Pune in March 2018. With an improving macroeconomic scenario and encouraging

customer demand trends, we plan to aggressively open new stores in the coming financial year. We

shall continue to add new stores through a mix of own and franchise stores which will provide us

profitable growth and expand our pan India brand presence”

Originally they had little receivables,given they were just a retailer.That might explain the increase in receviables,since they have now taken the franchise route.

Any one attending the con call tomorrow . Please do ask about what they have to say about the proposal to increase salary of the Directors which amounts to 2/3rd of 2017-18 profits.

This quarter results are worse already.

The total income from operations during QI FYI9 decreased by 7.45% YoY to Rs. 410.93 crores.

QI FYI9 ESITDA decreased by 29.71% YoY to Rs. 13.87 crores with an EBITDA margin of

3.38%. QI FYI9 PST decreased by 76.95% YoY to Rs. 2.04 crores with a PBT margin of 0.50%.

QI FYI9 PAT decreased by 77.52% YoY to Rs. l.31 crores with a PAT margin of 0.32%.

Isn’t the proposed salary above the maximum limit of 11% of annual profit. Senior members please guide - can we shareholders do something if the salary actually exceeds the prescribed limit.

what is the point in breaking one’s head to find out optimum level of compensation when it is clearly not linked with any logic or performance. They want top dollar for consistently underperforming the sector. I have attended few calls and felt that promoter’s daughter reads the quarterly performance review to justify her salary. It is beyond ridiculous.

You can try asking question in the con call but I doubt CFO who responds in the call will say anything on this matter. My interest was aroused when I found that their Ranchi and Patna franchisees were outselling Tanishq in their micro markets. I don’t hold but I would exit and include promoter compensation in my checklist if not already.

Promoter compensation has ceiling but the calculation is complex. Firstly till 36 lakhs there is not limit. After 36 lakhs there is a ceiling but , we minority share holder cant do much if it is getting passed . This would be a very valid question in the concal. If they increase their Net profit significantly in the same proportion as they proposed to increase their salary , it may make some sense. Else its just playing with the money of minority shareholders.

Personally feel there is value is there in the company. For Ex : The total market Cap is equal to the inventory available with the company. Any minor margin improvement should result in substantial increase in PAT. Feels like downside is limited. However the risk mentioned above still exists.

I dont think there is any need of a turnaround here,the company is earning profit,it is just not earning a good ROE.But according to the company the new expansion will be based on loans taken with inventory as collateral.

I dont think there is any serious risk of company going under from here.

One point i have not analyzed till now is the impact of online retail (if any) on TBZ,thangamayil) etc.

Can anyone tell me what the contingent liabilities of around 150 crores are for TBZ.That must be a major factor to decide whether or not to invest in this company.