Quarterly Update -Q4 FY 2021-22

Titan YoY slow growth is only due to issues like Gold prices - Lockdowns

We have marriage season in April which as per management is a better season

Titan has always traded on rich multiples and it has proven to be a steady multibagger for me. It’s in my core holding with 15% weightage.

For prolonged time it may consolidate, but then it will make up for one’s patience.

Jewellery and consolidation of this market from local players to branded is a multi decade growth opportunity.

These occasional hiccups are par for the course.

My journey:

We all might know Titan rise over last decade, this is A good clip on time prior to that

- Why a watch company forayed into Jewelllery

- How it made in roads on market dominated by unorganized

- Why it took losses in initial years

Business Case Study")

Hello, fellow members, I was going through the historical annual reports.

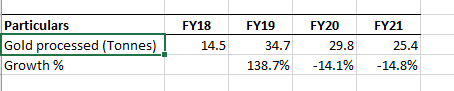

I found the quantity ‘gold processed’ under the heading of ‘Our Business Model’ (AR 21 Pg 42) in their Annual Reports since FY18, does anyone know what exactly does this mean and can this quantity be construed as volumes for the company? There have been significant fluctuations in this value of gold processed.

Off topic question…

Does Titan share holder rewarded with discount coupon to buy jewellery from Tanishq ? If so, how often and what is the minimum number of share to hold to get this

They had sent coupons via email in 2020. Didn’t receive it last year. Typically the coupons give few % off on diamond jewelry or making charge in Tanishq along with other coupons for Titan. Not sure on minimum number of shares. I think even 1 share will do.

4th Quarter 2022

Presentation

Financials

https://www.bseindia.com/xml-data/corpfiling/AttachLive/d8df6f6e-ff60-4bbe-906f-72343029d610.pdf

I have a position.

Yes, one share will also work. But the company haven’t shared the coupon last year.

Nopes it can’t crash. Gold is at a great level. Given the uncertainity Gold is going to do well

Plus titan is consumption theme and marriages are going to be a great push

Yes, current scenarios such is gold price, geo political tension, the consumers have shift their consumptions of gold buying due to higher inflationary environment. But according to the Titan’s call management is quite positive on the demand side. so growth will be back in the second half. other than that Titan’s other segments in the jewelllery is doing well such as golden harvest, studded jewellery, gold exchange.

I was reading that Titan management had given guidance of 50,000 cr sales in Fy 18 or 19 till Fy23…But I dont think its possible…They many not even reach 35,000 cr.

also Just by reading this thread, one thing is clear that This stock is not a secular story and future is uncertain and depends on many ifs and buts…Please correct me if I am wrong.

Really haven’t come across this management guidance of 50k. But given it were so in fy18 or 19, they would have no way to predict a devastating event like COVID which have a prolonged impact and will be felt for years even decades.

To me it’s a secular growth story but certainly not linear in terms of revenue, profit and consequently share price movement. Dependent on a commodity like Gold there would be significant factors impacting this company which is beyond it’s control.

However as India’s per capita income increases, luxury as a category will be disproportionately benefitted. To me there’s no bigger Lux brand in India than Titan.

This is a company which has innovation as part of its DNA and does not fear taking bold bets. The spirit of Xerxes Desai lives on.

There are huge adjacencies possible in future that the market does not factor in today.

Titan’s best IMHO is yet to come.

PS: Highly recommended book on this company.

Guidance of 50 K revenue is mentioned in this thread only…I think reference of some concall given…

What I meant is

- Titan as a business model can be called fragile ( Nassim Taleb terminology)

- They need to be constantly on their toes, ever changing and ever-gauging the mood swings of the consumer, and trying to experiment the things.

- Sometimes I feel, its more comparable to those Pharma companies, which needs to do innovation continuously in order to survive and those innovations are just not sure shot.

- Also Titan may be the only Brand in India in Lifestyle segment and it may go into adjacencies , going forward…but again why restrict the competition only to Indian brands?

In Electrical Vehicle segment, we are not just talking of competition between Maruti and Tata motors…we are talking of Tesla and many other future entrants, whose names, we are not even aware. - In lifestyle segment, when per capita income increases and aspirations of middle class bulges, they will very well try foreign brands too, and wont restrict to only Titan.

Disc. I hold Titan with small position…Trying to collect antithesis pointers…Also this is more to do with my personality. I want my portfolio constituents to be more anti-fragile and less innovators. They dont need to be perennially on the innovation treadmill.

as Warren says…“business should be such that even monkeys can run it” Those are my words…but meaning of warren.

I must have missed the 50k revenue piece…I would like to share my feel on the points highlighted by you.

-

If you look at major disruptions in recent memory - Demonetization, GST and COVID. The stock has strongly benefitted in terms of market share and the same has reflected in its share price. In fact I would argue that this has shown Antifragile characteristics. With adversity this company is growing stronger.

-

In this globalized world the lifecycle of companies are getting shrunk faster than before.

So companies have to keep on innovating to stay relevant. Titan is no exception. In fact one of the moats in current world would be a company that has a strong innovation culture and does not hesitate to take bold experimentations. IMO TITAN has shown that trait. Other moats are increasingly getting diluted with technology.

3 & 4. Titan WILL face competition from global luxury brands for sure. In fact I feel it already does and coming out favourably. It’s jewellery/making charges are priced higher compared to the neighbourhood shops. I think people who buy Titan are mostly from the upper middle / affluent class who already have knowledge and access to Global luxury brands and yet choose Titan. I am exclusively referring to Tanishk here. Indian’s penchant for traditional desi designs is an advantage to Titan. In other categories it may not be so.

- This will certainly happen/happening. However as the country becomes more prosperous - the demand for home grown Luxury brands will increase disporportionately. If we look at China and its luxury segments - Fashion, Jewellery etc similar trends are playing out.

On the Anti Thesis points -

-

If pace of innovation/ customer satisfaction does not keep pace with expectation, some other home grown brand may eventually eat into its dominance. Does not seem to be a case today but anything can happen in 5-10 years.

-

Luxury and Technology has merged and created a huge market opportunity e.g; Apple products, which Titan is yet to dent. I reckon wearable fashion with technology component will be a major thrust area world over, so there is no visibility/roadmap for Titan on that. Its foray in Smartwatch does not seem to have a very good traction.

-

As India’s affluence keeps on rising, the aspirational factor of existing brands will be continuously diluted.

For example Titan Watches do not have the same premium positioning that it used to have 10-15 years back with abundant availability of International brands.

So company has created/creating new premium categories such as Raga, Xylys etc etc. But this transition needs to be carefully monitored.

All in all. this is a company and segment that requires astute management and continuous execution. Unlike a Coca Cola which according to WB “even a fool can run”. Titan is certainly not one of those.

Even middle and lower middle classes have been shifting to Titan because they realized that they have been lower quality gold(compared to stated purity) from local jewelers though they had lower making charges. After Gitanjali gems episode where people paid lakhs to only realize they were sold pieces of glass in name of diamonds even rich realize importance of sticking to trusted brands.

So TRUST is their most important moat in jewellery business.

Global companies can never match demands of local tastes. Titan has created manufacturing ecosystem to cater to local tastes which is very difficult to replicate at scale. So ability to manufacture at scale catering to local tastes is their next moat.

Watches is a mature category.

Smart wearables is big opportunity but I doubt Titan will ever succeed because it does not have technology DNA.

Precision manufacturing, glasses are other opportunities.

But it is a company which has shown that it can evolve to grow, create new markets or take market share away from others. Definitely has a decade of runway left. Should be able to capture 25% of jewelry market share as undisputed market leader. That itself is 4x growth.

On Titan; undoing business mistakes (Titan Eye) is TOUGH as it costs a career… I would say fighting luck (random variables like perception) is much tougher than building abilities in retail!! … people managing career risk always choose mediocrity (clinging benchmark too tightly while managing funds, choosing watch brand name to sell eye-care products) …failing conventionally (instead of taking bold decision) is safest way to hide ability-flaws …Mr. Venkat becoming emotional on ability driven success (u see how it helps in maintaining reputation!) in Tanishq doesn’t hold true for mediocrity in Eyewear performance (more than a decade is sufficient time to accept strategic defeat …perception is one of the random variable (what we call luck!!) that plays large-enough role to make/break success in category …specs are put over our eyes, the sacred place, at the joint of which you put TILAK (godly stuff!!) …eye becomes an area of respect (love songs written on eye outnumbers songs written over wrists!!) …treating both wrist and eyewear brand with same brand name (Titan) is a classic marketing mistake …peole want superior brand for eyewear compared to watches that they wear (also to show off as it’s more visible than watch)…if, even after more than a decade can’t teach enough lessons, correcting price and retail format (abilities) won’t be of much help … fighting luck (random variables like perception) is much tougher than building abilities in retail!!

Nicely Put. I thought, I am reading Nassim Taleb…Your words resonate with his. Alternate Histories…I am a big fan of Taleb