This action reminds me of Blue Chip stamps purchase by Charlie Munger and WEB and how they used this vehicle to buy See Candies and other opportunities. Quite a parallel!!

Disc: Invested

This action reminds me of Blue Chip stamps purchase by Charlie Munger and WEB and how they used this vehicle to buy See Candies and other opportunities. Quite a parallel!!

Disc: Invested

Hi can you rework the assumptions post the quess stake sale and reduction in debt

Hi @parthabpl - I fully trust Mr. Isaac and Mr. Watsa as partners and in their capital allocation decisions which has been proven by their long track record. I am not too worried by the finer details of this quess stake sale corporate announcement. I am sure Mr. Isaac understands “dilution” very well since his skin-is-in-the-game. I am sure he would not acquire something if it is not going to add value in future.

Also, I don’t think they have given complete clarity of how the funds will be utilized. I am going to monitor the details they share as part of next quarterly earnings call. I feel Warren’s quote is very apt to your ask here - “A company should be viewed as an unfolding movie, not as a still photograph.”

Disc: invested

Group Consolidated results:

Revenues up 51.6% to Rs. 3044.1 crore as against Rs. 2008.5 crore in 3Q FY17

Profit before tax increased by 4.6 times to Rs. 87.8 crore as against Rs. 18.9 crore in 3Q FY17

Material events & outlook:

1 The proceeds from TCIL’s stake sale in Quess Corp during the quarter are being used for repayment of TCIL’s long term borrowings as well as for working capital requirements.

2 Repayment of borrowings and efficient use of the proceeds is expected to contribute approximately Rs. 36.0 crore to TCIL’s bottom-line annually.

3 TCIL remains open to suitable and attractive M&A opportunities.

Forward bookings show marked improvement, up by 32% on a YoY basis.

TCIL opened 5 new foreign exchange counters across Bhubaneswar, Varanasi, Guwahati, Madurai & Gaya in CY 2017

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=863a7037-a9d0-41f2-85e7-7ac831df4f1c

Thanks

Ashit

The UDAYAN scheme is already providing a filip to the retail ops of the company providing them a platform to open kiosks at new airports or airports which are now operational. This provides them massive tailwinds from a captive customer perspective!!

Couldn’t find anything on UDAYAN scheme. Can you please explain what is the scheme and how will it benefit TC? Thanks.

Discl: not invested

I thought it is important to point out that reading Thomas Cook results requires a little more care. At first glance, while PBT may have increased 4.6x, giving an impressive read; but what matters is profits attributable to shareholders of Thomas Cook.

You may see from the attached Thomas Cook Dec 2017 results on page 7 that 59.77 crores were earned by Thomas Cook and its subsidiaries, but after deducting what is due to non-Thomas Cook shareholders, the profits come down to 10.03 crores; i.e. only 20% of total. This seems quirky can potentially mislead.

This reduction of 80% is because Quess, of which is now owns 49%, has generated bulk of the profits. Quess earned Rs 70.13 crores, ( Quess Q3) of which Thomas Cook earned 34.5 crores by virtue if 49% ownership. This means that rest of the Thomas Cook business made a loss of about Rs 24.5 crores for its owners in the quarter.

This is not very apparent from a quick read and it requires some mental adjustment to note that while Thomas Cook made profits of Rs 60 crores in Q3, its owners ultimately get only 10 crores.

my apologies it was UDAN scheme which i was refering to here.

Agreed but Thomas Cook has funded all other businesses be it Quess (not now but earlier) and Sterling and therefore all the debt was in TC books at hold co level. By have sold the 7-8% stake in Quess this debt at hold co including pref shares would be liquidated thereby generating a +ve cashflow of INR 36 crs. With Sterling turning around this qtr, this would bring in better results at TC level.

Sure, as long as you know it. I haven’t seen such a gap between the consolidated earnings and earnings for owners and seemed surprising enough to point that out.

Extremely honest and transparent group

See this interview CEO himself telling honestly that travel is no entry barrier businesses so our margin will be steady on question that it will increase or not , they know Branding and product offering is key

Roughly they have done 6 to 7 acquisition and Quess has done 22 all are turning profitable (few r round corner)All in all efficient acquiring record

Thanks

Ashit

I’m not an accounting expert, but from my limited knowledge there’s some misunderstanding here. On p.7 of the results, as you mentioned, consolidated Q2 profit is ~60Crs. Out of this, ~10Crs is attributable to companies where TCIL has controlling stake (for simplicity sake, say, 100% owned businesses) while ~Rs.50Crs is attributable to subsidiaries where Thomas Cook has non-controlling stake, which includes Quess.

So TCIL’s share of Quess profit is part of this 50Crs, and you should not reduce that from Rs.10Crs remaining, which has nothing to do with Quess. In fact, you can say that all other units of TCIL are not earning much compared to non-controlling companies like Quess.

Subject matter experts can pitch-in

Slight correction in what you have written but with large implications:

No, ₹ 10 cr is Thomas Cook’s earnings in all the businesses it has ownership in. In part or in full. So if a company in which I have say a 40% stake earns ₹ 20 crores, ₹ 8 crore is my share. Sum of all such earnings is ₹ 10 cr.

No, ₹ 50 cr is earnings belonging to those owners other than Thomas Cook across all subsidiaries. It is not Thomas Cook’s earnings from its ‘subsidiaries where it has a non-controlling stake’

This may be cross validated by multiplying the EPS with Total number of shares giving net profits earned by shareholder. EPS is ₹0.27 as per item 13. Total shares outstanding is 36.704 crores as arrived at from item 12 (Face Value is ₹ 1 and Share Capital is 36.704 crores). Multiplying them gives ₹9.91 crores or about ₹ 10 crores.

I hope this clarifies.

The board meeting outcome looks very interesting. The holding company discount will disappear if shareholders are directly given Quess Corp shares. This should be a major positive for the stock. Based on CMP alone (forget Quess Corp valuations) Quess shares value will be >80% of Thomas Cook valuation. Negative for Quess as liquidity in Quess will now increase and many holding Thomas Cook may not be too keen to hold Quess.

Interesting to imagine how this will be done.

Thomas Cook holdco will create a subsidiary.

The subsidiary will issue shares to Thomas Cook holdco in exchange for shares of Quess holdco issued by Thomas Cook holdco. Thus Quess holdco shares will move to subsidiary without cash consideration received by Thomas Cook holdco.

This subsidiary is sold by Thomas Cook holdco to Quess holdco; and in consideration Thomas Cook holdco shareholders are given exactly the shares that are housed in the subsidiary bought by Quess holdco in exchange for the shares of subsidiary.

Simultaneously the subsidiary is merged with Quess holdco and the Quess holdco shares in the subsidiary are extinguished.

Thus in an entirely cashless transaction Thomas Cook shareholders get Quess shares directly. Not the Income Tax may take a view that this was done solely for the purpose of tax avoidance and may kick in some rules and contest. Now to avoid that Thomas Cook holdco may color the transaction with a small business also attached with it.

Will be interesting to study as it emerges.

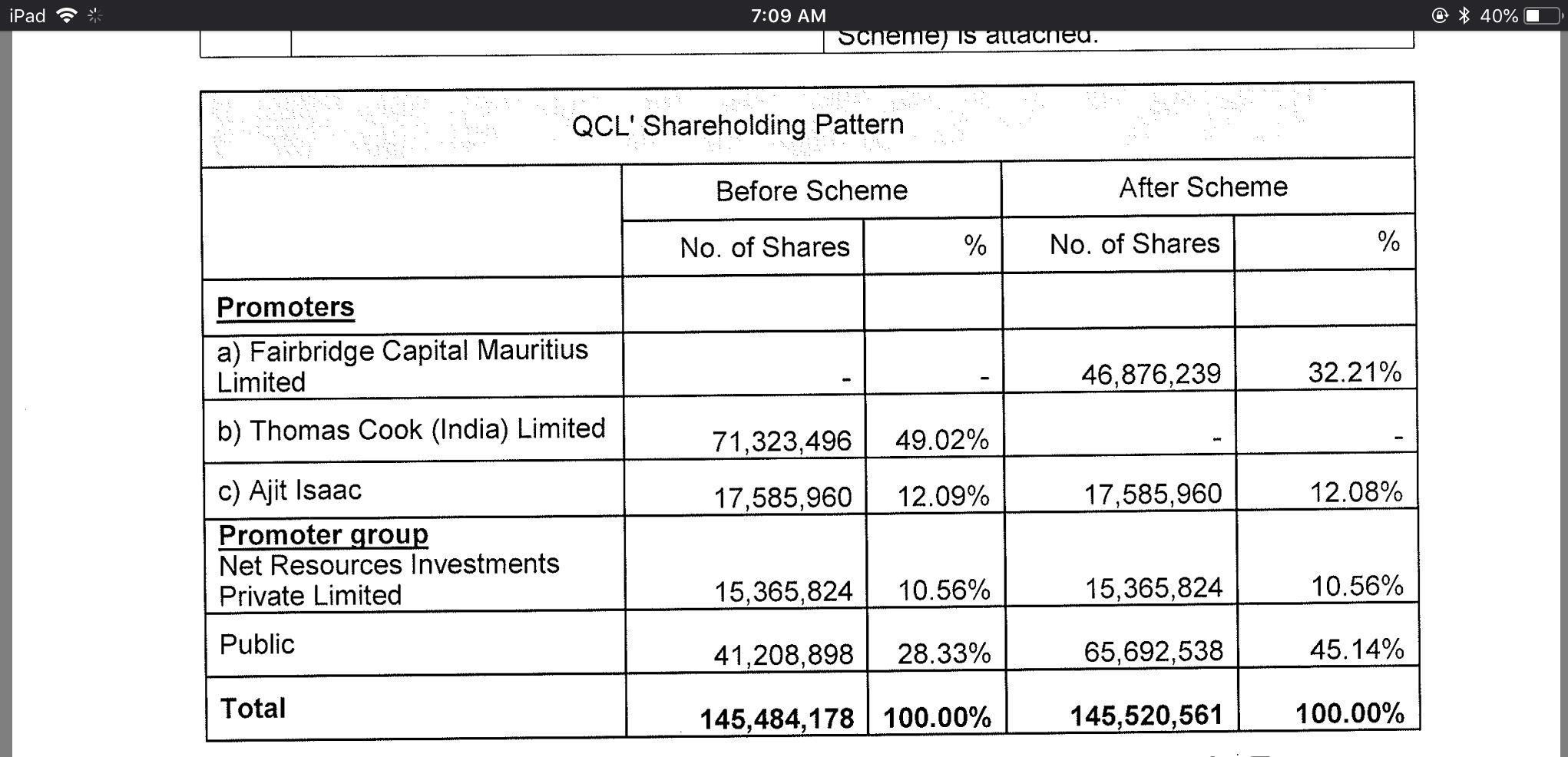

Board has approved restructuring- swap ratio of 1889: 10000. 1889 shares of quess for every 10000 Thomas cook shares

Thanks @Augi

Interesting and simpler than I envisaged, but colored in a different way.

The HR business of TCIL (which includes shares of Quess) with a turnover of 3.3 crores ![]() will be demerged and merged into Quess for '…increased competitive strength, productivity gains…significantly contributing to future growth’. In return shareholders will get 1889 shares of Quess for every 10,000 held.

will be demerged and merged into Quess for '…increased competitive strength, productivity gains…significantly contributing to future growth’. In return shareholders will get 1889 shares of Quess for every 10,000 held.

TCIL will transfer 7,13,23,496 shares it holds to Quess and in return the shareholders of TCIL will get 6,99,32,173 shares of Quess directly (being 37,02,07,374 total shares of TCIL * 1889 / 10,000). This shortfall of 2% maybe the fees for the transaction. It is not mentioned what Quess will do with the shares it will get as part of the acquiring the undertaking. But since it says shareholding will be broadly be the same, I guess it will extingush the shares.

However, there seems to an anomaly in the math provided on the total number of shares after the scheme, in the Quess announcement.

As per our computation above, after the scheme, there should be a reduction of total shares of Quess by the difference between 7,13,23,296 and 6,99,32,173; i.e. 13,91,323. However the Quess announcement shows an increase of 36,383 shares as can be seen below:

If someone can shed light on the anomaly, would be great. The one reason could be fractional shares after conversion, but that leads to reduction, and not an increase.

Hi Can you please explain what will happen to shareholders who own less than 10000 Shares. Not sure if we will get Quess Corp shares.

Let us say you have ‘x’ shares. You will get 1889/10,000*x rounded down to the nearest number. The balance you will typically get as cash, based on the values of Quess on record date.

Hi Sorry when I read the document I coudn’t find this info. All I found is “Pursuant to the Scheme, TCIL shareholders will

receive 1,889 equity shares of Quess (of Rs. 10

each) for every 10,000 equity shares (of Re. 1

each) held in TCIL.

No cash consideration shall be paid by QCL to the

shareholders of Thomas Cook (India) Limited.

Further, no cash consideration shall be paid by SOTC

TRAVEL to Thomas Cook (India) Limited”.

Not sure If I am missing something