Last year was best in the history of the company with record profits and cash flows.

Malaysian subsidiary has completed revamp and expansion and has started showing strong results.

Raw material prices are linked to crude but so are the product prices and hence margins are protected.

The government has been supportive with respect to duties on imports.

Future focus is on Growth and Value addition and Market Position.

Company is modernising older manufacturing facilities (funded from internal accruals). Ongoing revamp at Ranipet will be completed by Q4 resulting into excellent technology, lower costs and better productivity & safety.

New manufacturing facility at Dahej (PA) which will bring company closer to 80% of the customers and to a major supplier (> 95% is sourced from Reliance). First phase will be on stream next year and will be funded from internal accruals.

Indian market is large enough to absorb additional production from Dahej.

Company believes there is a good opportunity of growth in MAN (Maleic Anhydride)

Malaysian subsidiary to do more CAPEX to increase capacity to 65000 Tons in next 2 years. Maleic Derivatives plant, a new product range for the Company, will be commissioned in Q3.

Company is exploring to build a manufacturing facility in the US for food ingredients.

QnA:

Total planned CAPEX and desired IRR:

Cannot disclose this information as it is confidential. It is rigorously looked at. Company first looks at getting best capacities from existing plants. But they also have to plan for next 3 years as it takes about 3-4 years to get the approvals and build a plant.

Oversupply of ortho-xylene (raw material) resulted in improved margins?:

There is no oversupply of ortho-xylene. There is a long term contract with the main supplier from India.

Anti-dumping:

5 years period is over and government will decide if they want to extend or not. Company has been interacting with the government since past 25 years and they have been very helpful.

Food ingredients and derivatives:

Company has been in this business since 1993 in a small way. Mostly worked in Europe. Started work in India in last 5 years and grown from very small beginnings to a fairly large manufacturer. There are few companies in this niche worldwide and Thirumalai is one of them. It is company’s own technology which has been developed since 1991 and constantly upgraded. Company is very competitive and the quality is excellent. It takes 3-4 years to get an approval which itself is a barrier for a new entrant. They are also difficult technology. recently expanded and doubled the capacity last year. Still not able to satisfy the market (Europe, Middle East and India). They used to be in the USA 20 years ago but had to withdraw as they did not have products. Approved by most of the global majors. It is still a small business compared to their commodity Phthalic Anhydride or fine chemicals. Company sees this as an important part of the future because of it’s value addition and there are very few competitors worldwide with the technology.

Competition:

There are 3 players (one of them is IG Petro) for Phthalic Anhydride. Asian Paints was also a competitor but they stopped producing 2 years ago. Many other small players in India, Europe and Asia closed down. It is a very large capacity industry. Thirumalai’s capacity is global and is amongst large companies globally but focus is mainly India.

Mainly 2 players in India produce 350000 - 400000 tons. Globally, there are many small players. In Mumbai, there is one with 10000 tons capacity as against company’s 140000 tons which they may go upto 200000 tons. So there is wide variation.

Globally, there are 10-15 large players which is also shrinking and they control over 70% market. It’s more of a regional business.

Whether the capacities are interchangeable:

Plants are completely dedicated and can not be used interchangeably. Cannot convert any plant to make Phthalic Anhydride or Maleic Anhydride. These are purpose built plants and it takes 3-4 years to build them and atleast 10-15 years to run these plants. These are large petrochemical plants with high risks.

Dahej plant:

Strategic decision taken over many years. It will take them closer to their customers. Also, the supplier of the raw material (Reliance) will be closer. Presently, they are far away and yet competitive. It will help them save transportation as well as improve working capital. They need additional capacity as presently they are running at 85-90% capacity which is optimum.

Plant Shut down:

Some of the existing plants are 25-30 years old and it is difficult to push them beyond 85-90% capacity without risks. This is why company is revamping plants with new equipments completely. It is a step by step process as they are also operating the plant and cannot be out of production. Took a necessary maintenance shutdown which normally takes 20 days in a year but this time it took more than a month. Since plants are very hazardous, this should be done very carefully. This was an exceptionally long shut down in India as well as in Malaysia. There will be a shutdown every year. Plant runs 24x7 for 340 days in a year.

Margins: Phthalic Anhydride: Gross margins fluctuate. Over the last few years, gross margins have been good as many players dropped out. Food ingredients and derivatives: They are much better than Phthalic Anhydride. However, the opportunity size is huge for Phthalic Anhydride compared to food ingredients.

China:

China is an importer of Phthalic Anhydride for last 50 years. Company could sell in China but does not want to as the prices are a bit lower.

How much of production is using Naphthalene? Is it cheaper compared to ortho-xylene?:

China is the only country which makes and uses Naphthalene. It is carcinogenic. It is slightly cheaper but is also very volatile. It depends on the steel industry. You get more Naphthalene when the steel industry does well. Technology is very similar and company can do it if they want but they will not. ortho-xylene is very clean raw material which is easy to handle and not as hazardous as Naphthalene. So there is no threat of competition from these plants and China is a net importer.

Exports:

India exports around 40000 - 50000 tons. Gujarat plant will help reach the middle east markets faster which are very large. Globally company is competitive to export however do not have enough capacity to export. They do not propose to export too much. Will export to nearby countries but not too much.

Will the expansion by us and IG petro (around 65000 tons) result in oversupply?:

Present expansion by IG petro and ongoing / proposed expansion by the company will be significant. It will still not meet entire demand in India. India will still need to import. So there is no threat of oversupply after these capacity expansions. US expansion: Still studying this market and already worked on it for 2 years. It is an extra-ordinarily good market and they were active in this market in the past. Company is not able to supply due to distance and also the volumes. North America and Canada is 20 times larger than our market. Company is very competitive, has a good product, has all the approvals that are needed, technology is good and raw material is extremely competitive there. These are the main reasons for going there and company will be very careful throughout the process.

Increase in Working capital (mainly decline in trade payables):

Company had a lot of free cash. So instead of investing in mutual funds, they paid their suppliers ahead of time as the returns were favorable.

Capacity Utilisation:

Effective Capacity Utilisation is around 95%. However, original name plate Capacity Utilisation is around 85% as some of the plants are old. In 2 years time these problems will be solved.

Technology threat:

Technology threat is not much. Plants are very large and it takes years to learn to run these plants.

Organisational changes:

Lot of young people have been inducted into middle and senior management teams. Taking special efforts as much of the senior management is ageing.

Maleic Anhydride:

Malaysian company is doing a major expansion. Everything is managed by Directors in Malaysia. It is an independent board and they call the shots. Indian company guides them but do not control them.

Customers:

Supplies to construction, auto, coatings and 20 other industries but mainly construction and auto.

Dear sir,

Firstly thanks for sharing the wonderfully informative notes. This is what makes this platform click!

Secondly, may I ask you to elaborate on point 15. What explains the difference between name plate capacity utilization and effective one? Is name plate by specific product and hence lower compared to effective which looks at gross utilization based on MT produced versus max capacity?

Reg.: Analysts and Investors meet on July 24, 2018 at 4.15 pm The Chairman Mr Parthasarathy, the CEO Mr. Sethuram and the Executive Director Ms Ramya Bharathram, spoke about the performance of the Company and the plans. ,

The key takeaway from the investor meet was that the Co. is in a bit of a sweet spot, despite a subdued Q1. As stated by the mgt., Q1 results pertain to two months working. Extrapolating for the full year, even with the existing Q1, the Co. could on a consolidated basis do sales of about 1420 crs for 2018-19. Assuming the operating margins remain at Q1 levels, though they could easily get progressively better with each passing qtr due to modernization & value added products, the Co. could manage to have an operating profit of about 318 crs & PAT in the vicinity of 180 crs for the full year with an EPS of about 175. The current Enterprise value of the Co. is only about 1500 crs.

About the sustainability of current operating margins, the mgt. said that this did not happen overnight & that they have been working at it for the last 4-5 years, making continuous efforts at reducing the working capital cycle & not accepting orders under a certain level of profitability. I guess they may also have succeeded partially there is no supply glut in the market.

The moneycontrol article above is based on the assumption that anti dumping duty on imported PA will actually end in December 2018. The fact is that the Govt. has to take a fresh call by then, about whether to increase, decrease or leaving it unchanged. Needless to say that a fair bit of lobbying will be done by the industry as a whole. Besides, net imports of PA are only about 14% & the rest is supplied by Indian manufacturers like Thirumalai.

Even assuming the worst case scenario of anti dumping duty being abolished, it logically should impact prices only marginally. It’s not that the price of PA would reduce by the amount of duty as replacing Indian made PA with imported stuff is not an option. Besides, the production from the Malaysian plant will be unaffected by any change in the anti dumping duty structure, as also the value added derivatives / food chemicals business.

I have following your posts about Thirumalai chemicals and they have been very useful.I have few questions about the company.

information on Revenue generated by the company split geographically?

Also please help me understand regarding the overall demand for PAN worldwide and in India?

I think irrespective of the anti-dumping duty, there would be no threat of cheap imports once the dahej plant comes up as it would lead to huge logistics cost savings thereby giving advantage to the company to reduce prices to 10-15% extent in case of competition without affecting margins

Hi @Manojlion,

At the outset I cannot claim to have great insights into either the working of the Co. or the sector as a whole. Whatever understanding I may have has come from going through the Annual reports & attending the last couple of AGMs. Though I must confess that the investor meet post the AGM was most productive.

There is no supply overhang as far as PA is concerned. This has to be our main concern. The mgt. is extremely conservative & cautious when it comes to expanding capacities. The same is the case of the competitor IG Petro. These guys have burnt their fingers in the past by creating huge capacities about a decade ago. Even the Dahej expansion was started after much deliberation, after the infrastructure was in place. Likewise, the proposed manufacturing unit in the US has been under consideration for the last 2 years. Interestingly, even though PA is a commodity, a fair bit of technology, some of which is patented, goes into making of food derivatives / fine chemicals. Same is the case with MA. Also to be noted is that for the US plant, the technology will be provided by the Co., & the main purpose of the plant will be two fold- supplies to the US & Europe which is a huge market & the cheap feed stock (Gas). If anything the mgt. is erring on the side of caution.

Asia is where the main growth in PA is coming from. Currently the mgt. is focused on the Indian market for PA & not exports. That is likely to change somewhat post Dahej going on stream.

While it is always a good idea to have great insights into the industry / working of the Co., I have often struggled to master them. As individual equity investors, we don’t exactly have mgt.'s falling head over heals to entertain us, which is unfortunate but true. In the end, based on whatever info we have, we have to take a gut call. I see earnings visibility here, which is why I am invested. I also got the feeling that the Thirumalai mgt. was capable of creating wealth & sharing it with their share holders, but lingering doubts are what we investors have to learn to live with!!

I have started following IG Petro and Thirumalai Chemicals recently and understand that its Duopoly market for PAN with above players catering to nationwide demand ( Keeping exports out which may grow in near future if there is further clampdown on China Plants. Would appreciate your help in following areas:

Why are IGP and Thirumalai trading at such a low valuations when they have entire nationwide market to themselves. There are instances where loot of other chemical companies are trading over twice the valautions compared to them.

With PAN demand expected to grow by 6% in India, and no additional capacity from other player likely to come due to high entry barier, what wold be the threats to growth of IGP/Thirumalai

Do we have visibility of what would be the prices at which PAN is currently being imported? and what would be the impact incase if the antidumping duty is removed.

BOth IGP and Thirumalai seems to be identical in most of the value parameters, are there any differentiating value difference which makes one prefer over other.

One reason could be that market still treats Thirumalai as commodity player. PAN is a commodity but they are now deriving around 25 % revenue from speciality chemicals used in other FMCG applications. A few years back CEO mentioned in an interview that mission is to get 40% revenue from speciality that way company doesn’t become cyclical.

Descl: Invested from very early stage (23/share as per split).

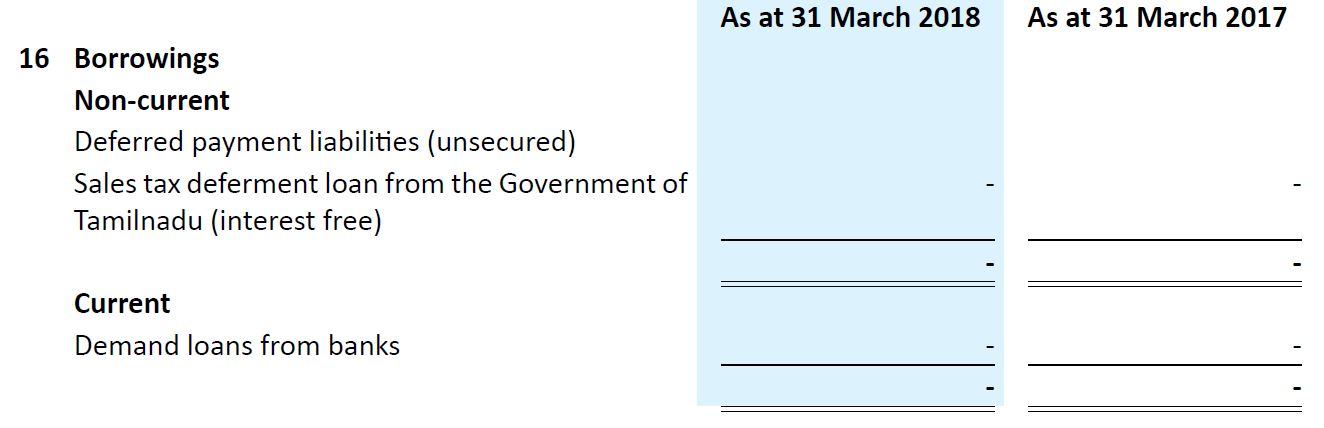

While going through the standalone financials in the Annual report 2017-18, the borrowings (long term as well as short term) have been stated to be zero but the finance cost of INR 1093 lakhs is still appearing.

Finance cost at consolidated level is perceivable but standalone level should ideally be zero.

The Company does not have deposits either. Is something amiss here?

Rising crude oil prices are negative but the company has some portion of fixed price contracts…Also the increase is passed through to the customers with a lag. Depreciation of rupee is positive for them as the imports get cheaper thereby giving both the domestic manufacturers room for increasing prices

The Thirumalai stock has taken a beating in the last couple of months or so, primarily because of the removal of anti dumping duty on PAN which also hurt the sentiment towards the stock in an already troubled market.

What is interesting to note is that bulk of PAN imported into the country was in any case coming without the anti dumping duty being imposed on it. This is also visible from the prices of PAN over the last 6 months or so. The PAN price (Retail) ex Mumbai as of today is Rs. 87 per kg, which was about the same in March 2018. Of course, it has fluctuated in the interim in a range of Rs. 80 to 90 per kg. The point being that there is negligible impact on pricing, if any at all after the removal of anti dumping duty.

Another interesting observation is that during Q3 of last year when the Co. came out with its best ever quarter, the PAN prices ex Mumbai fluctuated between Rs. 68 to Rs. 80 per kg. The input costs have also gone up in the interim, but the larger point being that perhaps the current share price correction is more news driven that the actual changes on the ground. However, the picture should get clearer when the Co. announces its September qtr. results in a few days.