Well without going into any direct question related to any buy/sell questions at any specific price point and for any specific time horizon, here is a a bit of homework that I did recently. Hope you find some pointers -direct or subtle - worth evaluating. So, here you go…

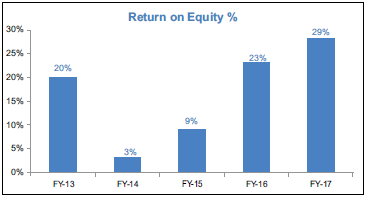

Quite curious case where ROE has increased at an envious cliff - straight from 9% to 29% in under 3 years. Any one will go head over heels just by these numbers.

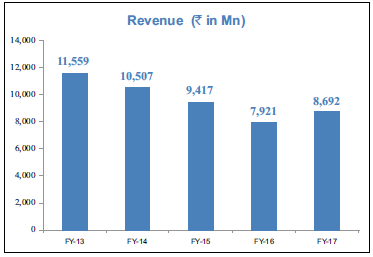

However, what really is at stark difference is the top line growth. Struggling for past 4 years.

Contradictory…very very contradictory and unusual. How can it be that a company with shrinking sales yet improving ROE. Whats better than a DuPont analysis to see what is driving the ROE:

What is evident here is that Net Margin is reason behind improved ROE. Now, next drill down, what is improving the Net Margin? Here is a common size break down of cost (i.e. all heads presented in % value).

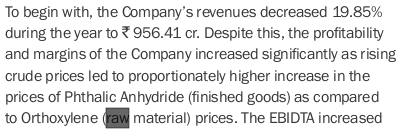

As evident, raw material is coming down for the same time frame. Non of the other header so significant to drive cost down and improve the profitability.

Have spent some time and will do so further in coming days, however, for now, I really dont have any firm explanation as to what is it that is leading to this reduction in raw material cost. Have gone through couple of previous ARs and sell side reports however, have not come across to find if they have got any backward integration or strategic partnership etc.

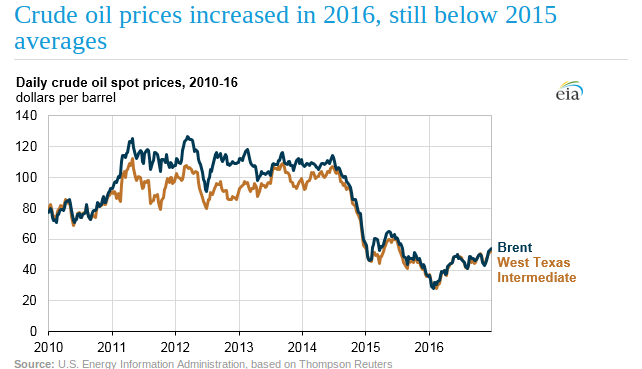

At the cost of sounding generic theory and little presumptive, is this has to do with the crude price fall? I am not very certain at this juncture but can be a possibility.

In conclusion, ROE is good and (comparatively speaking) stock is available at a reasonable P/E, However, so far I have not been able to notice any moat/edge or even a significant differential factor. Even not a short of any niche in its operating areas.

Regards,

Tarun

Disc: Not invested