NISUS Minerva Report

Looks like Transaction advisory charges something like a combination

of Investment Banking deal advisory+ AIF AUM +…

Looks Segment 1 Transaction Advisory charges followed by AUM fees bigger so far

Annual results can throw more light on NISUS segment wise followed by Any report or concall

1 Like

Yes, I bought the stock recently. I recently orderd from their website to check the authenticity of their claims. I received the products as promised without any quality issues, quality of packaging was good, but was delivered 1 day late by Delhivery. So, this may be a problem with the delivery partner, but I am happy with the overall experience.

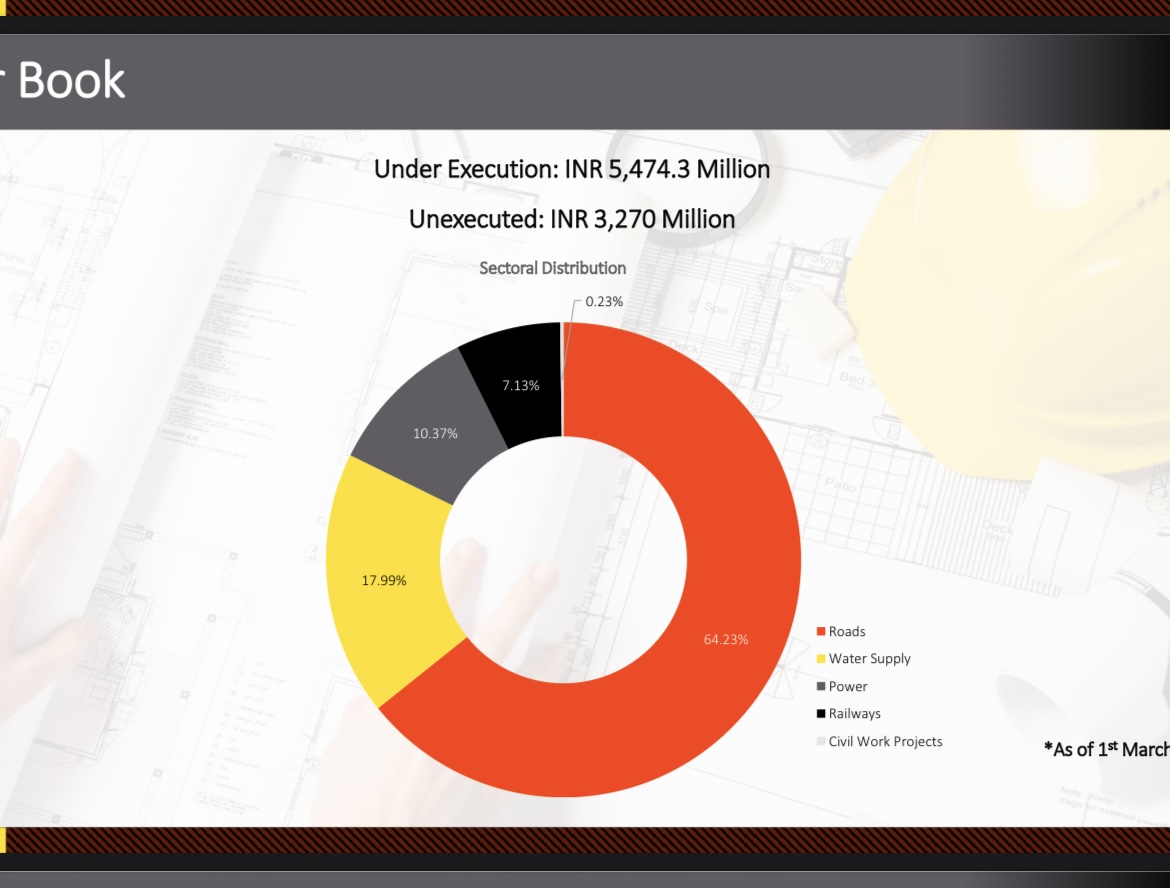

Anyone tracking k2 infragen?

Stock has fallen from 300 to 65

As per presentation released by company in may

Under Execution orders were 547 crores

As per presentation released in june

Under execution orders were 423

Implying 124 cr revenue already billed in 3 months

That is about 40 cr per month

If we discount for rain we can assume 20-25 cr revenue in July, august, september

Which amounts to 180 cr in revenue in H1 FY26

3 Likes

Hi Guys, anyone tracking EMA Partners. Stock has corrected quite a lot, valuations look pretty attractive and even the management feedback has been good. Would love to get some views on exec search business growth and their positioning.

Hi anyone here tracking goblin india, last result good and company looking attractive, give some view members

Thanks for bringing this to notice. Management quality is excellent and current valuations do provide margin of safety.

Blended margin of 18 percent this year, growth between 15-20 percent is key monitorable.

Bad news is CFO resigned due to health reasons on 30th June goes contradictive to management assertion of very less attrition.

I have starter a small position and will increase if stock goes down by another 5 percent and will also monitor this half results.

Goblin India never financially recovered since the challenging days of Covid lockdown. Better consider Brand Concepts in similar space. I have no position in either of them but may add the latter.

I know the CFO who has retired personally, so the exit reason was genuine I can assure. So won’t read that anyway otherwise.

1 Like

Any update on Sahasra electronic