Hi @Mas24,

As you mentioned above, understanding impact of interest rates is so important to understand the life insurance business. I have two specific questions in this matter.

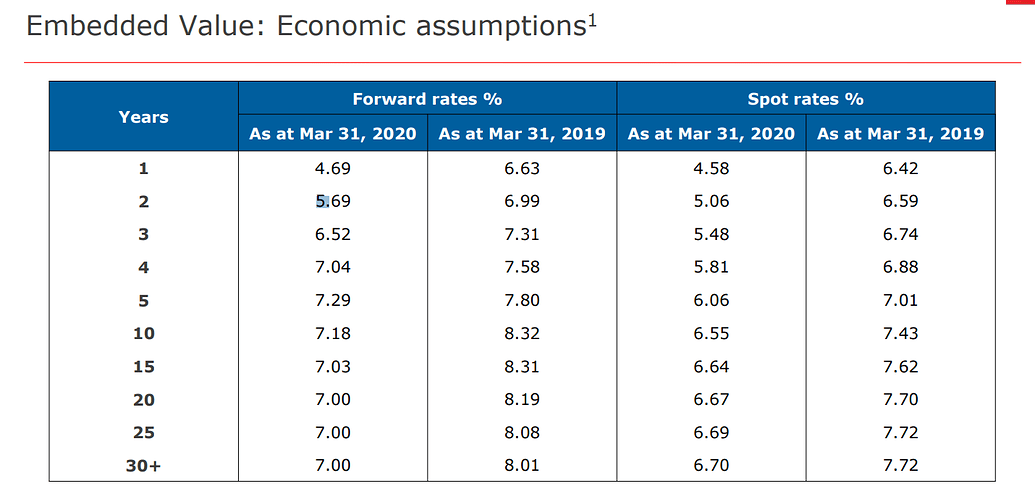

First one is risk-free interest rate assumptions in either coming to actuarial liability or in EV/VNB calculation.

The way I read above table is - projected cash flow that will be generated in year 20 will be reverse discounted at 7% whereas potential cash flow generated in year 2 will be reverse discounted by 5.69% as of Mar 31, 2020. So this is like weighted reverse discounting using a curve instead of a fixed rate. Is this correct?

If above understanding is correct, then this sounds very risky to me. E.g. take a case of calculating current liability in case of protection where sum assured will be paid after 30 years. The liability at 29th year will be x/(1.07).

In reality, risk free interest rate in year 29 from today might be 4% or even 2%. So aren’t liabilities vastly understated?

I do understand that this curve is a technical curve that is used by everybody but what stops companies from using their own estimate of the curve?

If above understanding is incorrect, can you please give us a texture with an example - e.g. can we calculate current liability sitting in balance sheet or P&L for a protection policy of 1Cr and tenure of 30 years? We can ignore mortality angle if required.