Hi,

Your portfolio heavily tilted towards Small and micro cap. Would love to know your thoughts on this ?

Why not consider some large to midcap which are growing equally well ?

Regards

Gaurang

Hi,

Your portfolio heavily tilted towards Small and micro cap. Would love to know your thoughts on this ?

Why not consider some large to midcap which are growing equally well ?

Regards

Gaurang

Yea, that’s a weak point. Last buy transaction I mentioned was all large-caps (almost).

I like a stock story (primary growth orientation) and market cap is factored into that, restricting to a certain cap universe would have reduced the choices. All my current buys are of VP-brand kind-of, where I found sound discussion of company fundas on VP forum, this is the overwhelming background to the majority.

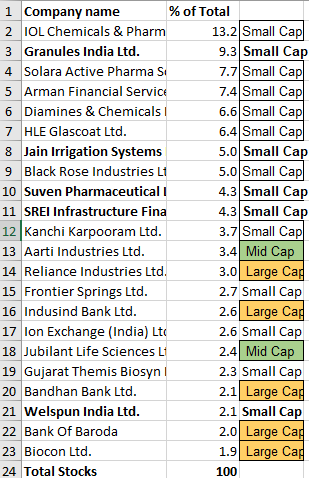

I did a quick check of cap, my rough estimate was 15% large cap and 25% mid-caps and that turns out to be roughly true. Capness is defined in 2 ways, based on ranking of cap and the other being bands of cap-sizes.

I generally follow the IIFL approach above.

Then there is the MF industry which must follow a strict definition here:

https://www.amfiindia.com/research-information/other-data/categorization-of-stocks

Based on the SEBI / MF catgorization, my PF would look like this:

Altogether 17.5% of PF would be Large and Mid-caps.

But if the IIFL cap-bands are applied, then total grows to 42.5%, this would include the stocks highlighted.

Jain and SREI are pretty much my only long term buys and they were definitely mid-caps when I bought them, I am still betting on their survival, post-Modiji, post-DeMoji, post-ILnFS and post-COVID etc.

And if they are able to convince the market about their long-term growth then my majority would be mid-caps!

I get scared of big-cap quality, seeing stagnation/decline of Tata motors/steel, Godrej Ind, Cipla, Yes bank, SBI, this list can be pretty big. If a person has to invest time and in this day and age with information revolution and such excellent fora such as VP, then why make the effort to just pick the slow but safe bet. If I had not found VP then indeed I would have stuck to only big-caps, well-known names, perhaps given up altogether and reverted to MFs.

Thanks for your feedback.

Your smallcaps are indeed hitting new highs and growing well.

I came across you when you started Gujarat Themis thread. Then you added diamines in your portfolio at near new highs.

I do lot of reverse engineering by looking at the companies only when they touch new all time highs.

Good luck for future

Regards

Gaurang

Good to see such quality inputs. Balaji n Diamines n Alkyl all doing well. What cud be the reason? Similar sounding names or what?

Whats your investment thesis for Ril? What’s abt investor doubts on so many subsidaries n quality of balance sheet of Ril? Cud it be the only Faang stock from India?

WHATS YOUR VIEW ON FINANCIALS SPECIALLY Bajaj fin,HDFC BANK & SBI card

Thanks! owe Suven pharm to your kind input!

Amines could be flavor of the season! Background to this might be as pharma and agro input, and import substitution, in an oligopoly-like market.

RIL is trust in the ability of Mukesh to keep on delivering value. Yes, maybe he can converge digital and retail etc. to be a FAANG-like entity.

I like all the three financials you mentioned, only Bajaj fin may have some issues with its model in the coming quarters and somehow SBI card may be little overbought, maybe buy on dips if you will.

Hi Harsha,

It would clutter that thread, so not right place to have this discussion!

Overall I have not followed the govt policy sector-wise for preferences post-covid, except I know of some incentives to Pharma etc.

Telecom yes, will be hit with anti-China policy for govt orders etc. but already BSNL is complaining that it is useless to give them a bail-out and then kill them again by forcing to buy only from Indian vendors! So, basically in telecom we do not have any company worth talking about, except maybe Tejas, and it is now quite cheap, so downside may be limited, but size of BSNL orders may just keep it alive, this one also has problems growing!

Also, heard about the ban on electrical gear, so power generation/transmission eqpt., but nothing great for this sector which overall has been struggling, some market share maybe saved, that’s all.

All Govt. tenders are avoiding China but there are other competitors for most such orders.

Textiles, no clue!

Hi Vikas,

Thanks for the insight

UPDATE:

Reduced IOLCP, Diamines by equal amounts, fully exited Aarti Ind.

Added Laurus 3.5% of PF and Aarti Drugs 2.5% of PF.

Wanted some comfort by reducing some concentrated holdings (with considerable run-up in the holding period) and diversifying into some well researched, good mid-caps. Thanks to VP members!

Cheers!

Hi Vikas,

Any rationale behind your reduction?

In short term - I see a good jump in PE breaking EPS - Q2 we can expect a good result with promoters having to wait for 3 years to exit their position

The company is undervalued in a long term scale with PE under 10 and High EPS of 40-45

Hi Vikas,

Considering the prospects and future earnings of IOL especially since they have ventured into other API formulations and management being very vocal on increase in revenue by around 400 crores next FY, doesn’t it still seem to be a good bet. Or have you exited partly from IOL just to avoid concentration in your PF?

Also sir, I would like to know whether you follow Tyche industries and if so what is your take on it as very little is available in the thread at VP.

Thank you

Disc - Invested in IOL

@nithin_Shenoy @Sajju Yeah, previously also booking profits in IOLCP turned out to be really bad idea, so this time I only took a very small bite out of it, it is still 16% of my PF, biggest by far, almost double the second in the list.

Maybe I am little jittery, my first 2x bagger!

Yes, it is bit difficult to track, the other 2 are more publicly discussed, that is a factor.

Not followed Tyche Industries.

Thanks!

I have been following this thread for a long time, I need clarification from @vikas_sinha, isn’t the strategy

To do deep dives

Learn all about the business, management & the fundamentals of the company

Wait for 3-5 years for the Large caps to multiply 1-2 times & the small caps by 2-4 times

Sell only if the company fundamentals changes or the market conditions doesn’t favor the business

I see you frequently doing buy & sell, although its your personal decision, but I am curious to know why you do so, is it because you are an impatient investor or because you are more of a trader than an investor?

Hi Sham,

Of course I will offer clarification!

To begin with I will try to deny the allegations of frequent buying and selling!

The intent is definitely to follow somewhat the steps you have outlined.

I only reduced positions somewhat and did not exit.

Yes, there have been sales of IOLCP and Granules, and I agree that both were big mistakes! (transaction worth ~10% of PF)

These two had reached ~40% of PF and I needed some cash for Suven Pharm, Reliance etc. so thought of milking the big, fat ones rather than the lossy ones.

Mea culpa, I got a bit scared with the valuations and thought of reducing concentration.

The buys were done from cash otherwise.

Yes, DACL I reduced for Laurus (transaction worth ~1.5% of PF)

Yes, I switched Aarti Ind to Aarti drugs. (transaction worth ~3% of PF)

I am just doing minor tweaks, other than the 2 big mistakes.

Yes, sometimes I find better stocks than the ones I am currently invested in.

A weakness is over-diversification, definitely. It is a defensive tactic, in light of lack of enough depth in diving.

PS: A minor sale of Kanchi was made also. (transaction worth ~1% of PF)

Totally missed this play, very temporary bump in RT-PCR testing, bought Kilpest 5% of PF today!

(cut SREI and JISL holdings by little over half, risk profile being somewhat similar)

Sold off three financials, IndusInd, Bandhan Bank, Bank of Baroda, past week, overall just 6% of PF. Hitesh bhai may be right, macro conditions will be tough for this sector for some time, no rush here.

Added to Jubilant Life, Laurus, Suven Pharm, Aarti Drugs and Kilpest, in increasing order of amount added.

Want to reduce below 20 stocks in PF.

I agree with your sentiments… my portfolio is vastly different to what it used to be. Some sectors like finance, travel, auto seem like they’ve hit a wall. They cannot got up any higher since there’s not much growth expected in these sectors for a while so they cannot be priced at pre covid levels… and they came up from their april lows since things were really bad then with the lockdowns and things are relatively better now. So they just seem stagnant. Whereas with pharma and chemical industries they look like they can easily continue breaking resistances since we can expect to see actual grwoth in those sectors. Same with IT and FMCG. My portfolio has gone from VIP, Sirca, Idfc etc to almost full pharma and chemical since. I jumped in a bit late (a month ago) but that’s only because it took me a while to understand the sector and the companies. I realised that not studying them And hence not investing in them was just an excuse from me and I did the hard work after. Everything seems brighter now. I have however, kept my entire stake in sbi cards which I bought at 500. The way the business is set up it feels like it runs independant of the problems of the financial industry and feels like its own seperate sector.

Thanks! I never bought pharma actively or chem either!

The only noticeable fact about Pharma was that PEs showed people respected this something like FMCG as a steady biz. That the sector seemed ready for break-out, performance and valuation wise, after stagnating for 5 years almost, with years of spectacular returns before the stagnation.

But I only bought 3 (or 4) stocks:

Chem. I only bought 2 companies:

But yes, these were big or sufficient size bets! My target was as close to 10 stocks as possible overall.

No buy or sell in March, April and May, just watched PF nose dive to half.

Fresh entries/churn happened mainly this month.

In Pharma: (no chems now)

HLE is play on both pharma and chem.

Kilpest is kind of like pharma, if they start exporting from August, it can be like a jack-pot.

Guj Themis is a very small part, hopefully the macros are good for it to grow. Or I sell it when I need to buy some quality stock.

My biggest bet by far, which is not possible to liquidate coz of losses, is Arman.

Disc:

Exited Frontier springs, like you have explained, will stagnate for a year and promoter quality is suspect, was smallest cap stock in PF.

My portfolio is currently just Laurus, iolcp, Suven, granules and Deepak(and the aforementioned SBI cards and idfc first since I just love VVs management lol). I had stake in solara too but something about it doesn’t let me sleep properly at night. As you may have noticed on that thread first it was ICD, then corporate governance regarding where they parked some money and the last straw was the random increase in pledged shares to 51 percent last quarter! I took out all my money from there and put it in laurus yesterday and I feel I’m on the better horse ATM. Considering investing even more in laurus since it looks an unbelievable bet long term. Was interested in kilpest but the way it’s rising scares me. Just 7 down days in 3 months or so. One unexpected result and I fear being trapped. Maybe just my paranoia but I don’t see how they’ll be able to benefit post covid and I can see the market looking ahead at some point and suddenly downgrading it. Haven’t studied it in detail though. Just know the basic story behind it. Anyway good luck

PF update:

Consolidated into 15 holdings only.

Bought more of the ones highlighted in bold.

Sold off mostly the tiny holdings, around the 2-4% region, Biocon, Jubilant Life, Ion-Exchange, Reliance and Welspun Ind.

Trimmed a little bit from IOLCP and Granules (these two have paid off more than their entire buy value, now it is a free ride).

| Company name | Last price | Cost per share | % of Total |

|---|---|---|---|

| Laurus Labs Ltd. | 1029 | 862 | 21.1 |

| Kilpest India Ltd. | 472 | 325 | 10.0 |

| IOL Chemicals & Pharmaceuticals Ltd. | 750 | 270 | 9.7 |

| Solara Active Pharma Sciences Ltd. | 874 | 702 | 8.1 |

| Aarti Drugs Ltd. | 1882 | 1610 | 8.0 |

| Granules India Ltd. | 317 | 152 | 7.7 |

| Diamines & Chemicals Ltd. | 413 | 233 | 6.5 |

| Suven Pharmaceutical Ltd. | 661 | 492 | 6.2 |

| Arman Financial Services Ltd. | 456 | 837 | 5.7 |

| HLE Glascoat Ltd. | 1005 | 835 | 4.6 |

| Black Rose Industries Ltd. | 145 | 144 | 4.1 |

| Kanchi Karpooram Ltd. | 353 | 262 | 2.6 |

| Gujarat Themis Biosyn Ltd. | 184 | 180 | 2.5 |

| Jain Irrigation Systems Ltd. | 11 | 16 | 1.6 |

| SREI Infrastructure Finance Ltd. | 7 | 15 | 1.5 |

| Total Stocks | 100 |

The figures in right-most column are based on current value.

50% up since end Jan 2020.

10% to go for break-even from the carnage since after 2017, overall PF life is little less than 3 years.

Congrats on nice returns

Few observations