Yes, spike in interest and depreciation is due to IndAS 116 from June 2019 onwards. Leases are capitalised which leads to lower expenses and high interest and depreciation

Has anyone been able to do some channel checks/store visits over the past 2-3 months? While online channel has been doing 2X of what it was pre COVID-19, any sense on when the traditional channels are likely to come into YoY growth more again?

The other point to get a finer handle on is the realistic annual growth rate for the organized segment in the women’s ethnic wear non saree segment. The pre IPO growth rate of 25%+ is unlikely to come back on a sustainable basis.

Other than these two, rest of the aspects of this business look fairly simple.

Disclosure: I am a SEBI registered individual IA. No position

4 Likes

Like Tcns. Wrote down certain key points.

Strong organic growth underappreciated

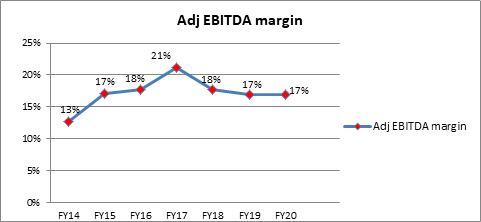

Heavy ramp up in store count, focus on being product centric vs channel centric, multi-channel approach, has led to an impressive ~37% sales cagr for FY13-FY20. It’s difficult to grow so fast without fumbling, testament to their execution skills. Retail comes down to execution, which in turn depends on getting the supply chain right backed by a good product fit. Discretionary spends in general have been under pressure in India for the past 3-4 years, and once the up cycle is strongly underway, the potential remains to surprise on the upside on sales growth. The company admittedly has an extensive ESOP policy (~10-11% dilution over next 3 years), but growth has not come on the back of increasing debt. BS has remained debt light.

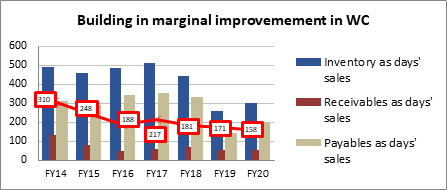

BS strength, Gm vs Lower payable days, approach towards expansion

Manufacturing is 100% outsourced, while design is 100% in-house. 40% of its stores are run by franchisees. Building an agile supply chain in ethnic wear is relatively tough, given a high number of fabrics+trim materials to sort through, to ensure a good product fit year after year. Navigating the seasonality in the business i.e fashion trends, separates the winners from the losers over time. Feel the company has embarked on a correct strategy of paying its vendors before time, supporting them, shifting vendors to low cost areas away from Delhi-Ncr. While this may elevate the WC due to lower payable days, the bigger priority is to ensure a smoothly running efficient supply chain. That is key!

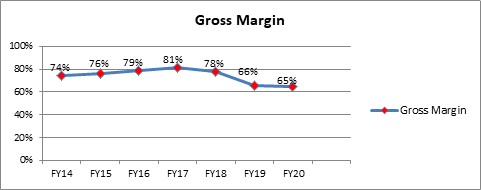

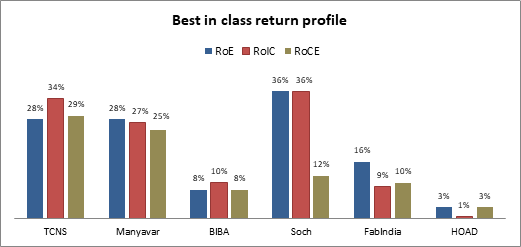

Instead, the company has focused on lower discounting & ensuring GM% is high. While larger fashion companies operate on gross margins of 50-55%, Tcns is at 62-63% gross margin. The combination of minimal capex, higher GM%, franchisee share %, lower payable days has resulted in higher ROIC% vs peers.

“we are not in a standard product business where we sell the same thing season after season = in our business at times depending upon fabric, fashion, depending upon whether you are selling one piece dress or you are selling three different pieces, your ASPs and volumes both can go in any direction, but this is something which is fashion. A person might buy three different pieces to make a combination or another person might get one dress and that is how consumers behave.”

“we have taken a route of slightly protecting our gross margins.”

“our focus is to get products on time, we think the gain from selling it full price would be much more than whatever inventory carrying cost that we have.”

“we have repeatedly said that we are trying to set up a low-cost base and we are also using cash on our balance sheet to get better rates for our products and that gain is reflected in gross margin. We are deliberately paying creditors before time, this is something that we actually can reverse any time”

“We have been paying our suppliers ahead of time which can be reviewed as per current situation. However, we will continue to be equitable partners and will continue to support our vendors.”

“we have been able to negotiate better in terms of fabric cost by giving better credit terms.”

“if you look at our working capital days generally it is about 100 days to 120 days and this is what we have been able to maintain over seasons, so last year, this year all these are in the similar range.”

“So, as a company we are focused on gross margins because we believe that in the long term that is what protects the brand integrity. Also, rather than just gaining revenue share in the short term by selling stuff on discount, which is not anyway great for margins, it’s better to control inventory and try to increase your full price sales. So lot of the efforts that the company is taking is on these lines, we have a rethink on the way we are creating the merchandise mix we are rethinking the way we are thinking of supply chain. So, for example today lots of our products are getting delivered in 60 days/in less than 60 days, which was not the case earlier.”

Valuations

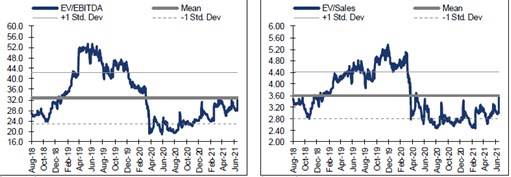

Prevailing valuations provide comfort. Retail is an extremely tough business, and one shouldn’t fool oneself on the historical unit economics of this industry, sustainability of franchises, constant evolving trends, fading away of very good cos & managements. It’s tough!

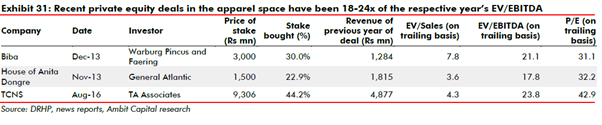

Interestingly, Branded apparel retail was a space which enjoyed premium multiples in 2016-2018. On a forward basis, cos traded at 4-5x EV/Sales & 18-20x EV/Ebitda. Today, Tcns trades at ~2.5x EV/Sales & ~14x EV/Ebitda FY23. While being cognizant of the risks prevailing in this industry, do feel the risk-reward is in one’s favour.

- Stable, incentivized & professional management team: The promoters have taken a backseat. Bulk of the executive team has been with the company for over eight years, carry esops. The MD has been with the company since 2011 & owns ~6%.

- Proactive focused approach towards online: Has not been caught off-guard post covid, unlike other retailers who were not focused towards the digital channel.

Online share to mix: FY16 7%, FY19 12%, FY20 10%, FY21 27%. Is growing its share of online sales from own websites vs. primarily 3rd party earlier.

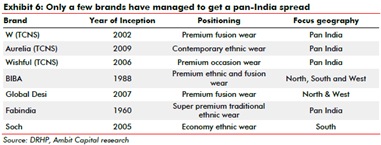

“Now, if you look at this channel right now, it’s contributing to about 23%, in midterm, about three years’ time, it should anywhere between at least 1/4 to 1/3 of the total sales. And we ourselves, as a company, are trying to push this” - Inorganic potential: Tcns has primarily 3 brands W(introduced in 2002), Aurelia(introduced in 2009), Wishful(introduced in 2006). Now trying to grow Elleven(coordinates foray), raise share of footwear & accessories. Healthy cash on the BS.

“one of the stated objectives for us has been inorganic growth; we see many small brands with tremendous potential which due to reasons of managerial bandwidth or probably risk appetite or financial constraints could not scale up. While we have seen multiple attractive assets in the past, we could not align on the right pricing. We see possibility of such assets coming at the right price now. Our industry is extremely fragmented with multiple small players with limited financial resources.” - Shift towards casual/light wear(WFM) vs heavy ethnic risk: Product offerings of W (Key revenue contributor ~55-60%) are inclined toward Indo-western fusion vs contemporary ethnic. Biba for example has a higher share of contemporary ethnic.

Disclosure: Invested.

8 Likes

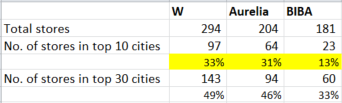

1 data point from a recent report on proportion of stores in Top 10/30 cities for Tcns & Biba.

1 Like

Notes from Q2 concall -

-

Q2 saw sustained recovery vs Q1 despite severely impacted July. Q2 revenues up 2.5X of Q1 revenues. Q2 Offline sales at 75 pc of pre Covid sales. Online business continues to see significant growth on an already substantial base. **As on date ( ie 12 Nov 21 ) revenues are tracking near pre covid levels ** Gunning for business to hit pre Covid levels and go beyond in H2 FY 22. ( Pre covid FY 18-19 Sales and PAT were - 591 cr and 70 cr )

-

Key focus areas for Q2 -

(a) Online business - continues to do well across own website and marketplaces. Omni channel stores fulfilment which was launched last Qtr scaling up well to cover most large demand centers and is now contributing to 5 pc of sales.

(b) Store expansion - Aim to add 60+ EBOs this year. Will open a store every third day in H2. This will take store count to above 600 + for the first time.

(c) Project Rise - Upgrading presence in key markets ( in up-mkt areas like CP showcasing the complete range of products ). Opened 5 large stores, clocking 1.5X pre COVID sales. Should help the brand to grow can consumer’s mind in a big way.

(d) Cash conversion and cost control - Q2 has been cash accretive. Last 3 out of 4 Qtrs have been cash accretive taking total cash to 160 vs 110 cr YoY. Reduced rent commitments by 20 pc. Continue to invest in ppl, infra and processes.

(e) Swifter thought to shelf - improved inventory management, consolidation of warehouse ops, express replenishment mechanisms and design incubation - fully on track.

-

Have built a differentiated footwear range, finding good acceptance. Footwear already contributing in double digits in EBO stores. Complete roll out of footwear range in second half of current FY.

-

Fusion Folk wear- being tested through 20 W stores. Seeing good traction here, will roll them out to 90 W stores now.

-

Aim to open 15 exclusive ‘Eleven’ branded stores in second half. This can be scaled massively if the pilot project is successful.

-

Over time, aim to make W a complete lifestyle brand. Piloting beauty products in EBOs and Online channels under the W brand. Getting good response here as well. Aim to make W a complete top to toe brand.

-

Qtly sales at 239 cr, up 66 pc yoy. Gross margins at 63pc vs 52 pc last yr. EBITDA at 45 cr vs 7 cr loss last yr. PAT at 11 cr vs loss of 27 cr last yr. Opened 17 new stores and closed 9 stores during the Qtr taking the total count to 557 EBOs.

-

Overall blended gross margins across clothes, footwear, cosmetics should settle around the current gross margins profile of the company. Sale of cosmetics and footwear in the Rise stores ( large format stores ) has been very encouraging.

-

Currently 37 pc stores are franchisee led and rest are company owned. Company chooses franchisee partners very carefully. Most stores in Tier 1 and 2 cities are company owned. Franchisee stores are in Tier-3,4 cities.

-

B2C in online is now at 50 pc. Rest 50 pc comes from other channel partners.

Disc : not invested. May take up a tracking position.

3 Likes

2 Likes

Aditya Birla Fashion and Retail ABFRL is acquiring TCNS Clothing and an open offer is being made for a consideration of INR 503 per equity share.

“On Amalgamation of the Target Company with the Company, the Company will issue its equity shares to the shareholders of the Target Company (other than itself towards the equity shares held by it in the Target Company) as per the below share exchange ratio: Brief details of change in shareholding pattern (if any) of listed entity 11 fully paid up equity shares of INR 10 each of the Company, for every 6 fully paid-up equity shares of INR 2 of the Target Company (“Share Exchange Ratio”).”

3 Likes

Promoters get cash for their stake at Rs503/share.

Minorities get 11 shares of ABFRL for 6 shares of TCNS.

So give 6 TCNS shares = 3,087

Get 11 ABFRL shares = 2,354

This sounds extremely anti-minority. Am I missing something?

This is one of the big risks of investing in a company where promoters hold stake less than 50%. I am sure promoters would have got some nice deal on sidelines to sell listed company for a pittance

3 Likes

If anyone well versed in legal matters can help clarify the below issues, it will be very helpful:

- The open offer price is determined in accordance with SEBI regulations. Do similar regulations apply for share exchange ratio, and if so, have they been adhered to here? (deal disclosures state exchange ratio is based on a valuation report confirmed by a fairness opinion, but the implied valuation of TCNS is much below the open offer price)

- Are there regulations that disallow promoters to receive higher returns vs non-promoter shareholders in a sale transaction?

- Lastly, at what stage(s) is non-promoter shareholder approval required? Is it required separately for the delisting via share exchange, once the open offer is concluded?

1 Like

TCNS Clothing … A Nifty 500 company ruling at 2 year low today at 384.

FII’s have reduced stake from 16.68 to 12.20 % in 1st quarter.

Anyone sees value in it ?

The company is being acquired by ABFRL. The first step of the process - open offer - is over. Now you will receive shares of ABFRL in 11:6 ratio - so the shares should be expected to trade in line with ABFRL’s stock. There is some arbitrage but not much. There is no deep value as such.

1 Like