Did someone do a detailed management analysis? How’s the management in tci express? Did anyone meet the management? Hows the management in the terms of Integrity, and competence? With the company’s performance competence of management can be clearly seen. But what about integrity? Are there any redflags? @mylu @vivek_mashrani @ramanhp @ankush12495

1 Like

Never met the management. But one observation over many quarters concall that I have attended- on topline growth the management always over-guides and underdelivers period.

But I don’t think they are unethical, TCI is an old & respected group in transportation space.

6 Likes

As per latest concall of Gati, in express segment gold standard ebidta margins are 13-14%, how sustainable are 20% ebidta margins of tci express ( not only that but management’s guidance of increasing it by 100bps every year for few years down the line )

As per Tci’s management Sme sector is driving the growth and Gati on other hand says large corporate and cash n carry segment are in a much better position than Sme as sme will take sometime to recover.

Mr.Chander’s guidance on revenue doubling and profit increasing 4x over 4-5 years seems to be too good to be true.

Some very basic red flags:

€ over guidance by management almost in all concalls

€ fumbling management during extempore questions

€ very low emp cost as %age of sales and no satisfactory revert by mgt, even fumbled

€ very lopsided contract with vendors as per management, it seems vendors are just ready to get exploited

€ some paid promotion to jack up share prices

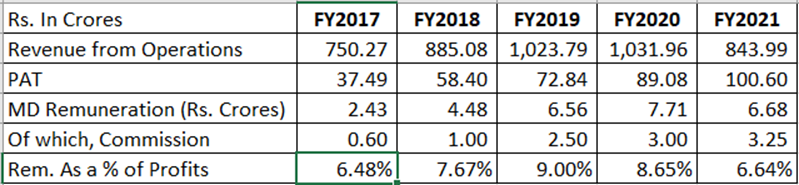

€ high mgt salary

Counter:

€ no debt

€ no equity dilution

€ moderate dividend payment

€ long history of operations

Analysis:

£ Overvalued, no doubt; so what, entire mkt is overheated

£ outright fraud, does not look like: some aggressive accounting, may be a possibility

£ whether capex is for real, if confirmed, then may be gr8 to get all answers crystal clear.

5 Likes

Tci express has a far superior business model compared to the other logistical players.

They are a asset light company that allows them to have a huge operating leverage when they scalenin size.

The only expenses would be employees and the fulfillment centres that they are building out.

They don’t own any vehicles and other assets that gobble cash. This is evident in the return ratios (roce, roe and roa) which is higher than any other logistics play.

4 Likes

Company reported it’s results today. Some important points in investor presentation worth noting:

-

During the quarter, we had received the required regulatory approvals for our 1.5 lakh sq. ft Pune sorting centre and it is now operational. It will also improve operational efficiency by ensuring faster and reliable service and support our branch expansion plans in the region.

-

Capex incurred during the year was primarily toward setting up owned Sorting Centre at Gurgaon and Pune; ~50 crores to be spent towards automation

-

In the next phase, TCI Express will focus on automation and technological upgradation

-

15 new branches were opened during Q1 FY2022 in the metro cities primarily in the North and West region to deepen TCI Express presence in key business geographies

-

TCI Express successfully launched Cold Chain Express Service, an asset light model and

use existing hub and spoke network to meet the growing demand for Cold Chain logistics

7 Likes

What do you guys feel about paying 5800cr (net worth) for something that can be replicated for ~250cr (assets)?

Doesnt it provide a commodity service in an expanding sector with very large investments being made by all players across the value chain?

Then question is - why their competition is not making money and creating same assets by spending 250 cr?

Why are their returns ratios > 20% and why OPM is high if it’s commodity?

It’s like saying I can create copy of Uber app for $1000 but why world is paying Uber so much valuation.

10 Likes

H1 FY22 vs H1 FY20 is good since H1 FY21 is an aberration due to covid

Company has entered into cold chain solutions which is one other value added service - margin accretive

2 Likes

My two cents -

Being pre-dominantly in B2B space helps the firm maintain its topline if not grow yoy. Efficiency in operations makes this company a repeatable and pure ROCE business

2 Likes

3 Likes

9M FY22 vs 9M FY20 (as per screener): -

Sales down by around 1%

EPS up by 32%

1 Like

My impression is that this is a good company in a bad sector. The main moat is their business model, which is an efficiently run tight ship with asset light business and good margins even in a commodity type business. Company is debt free and management seems okay.

Around 85% of revenue comes from road transportation of express cargo. The key end-user industries are auto components and pharmaceuticals. SMEs account for 45% of the business which is a risk. There is Intense competition from large organised players as well as unorganised players due to fragmented nature of the business. Ability to pass on increase in fuel prices remains critical to maintain profitability, though the company seems to have demonstrated that successfully in the past. There is also increase in competitive intensity over the years on account of the entry of P/E backed logistics players who may not be bothered about profitability and can ruin the market for everyone.

Some readers have commented on managerial remuneration and related party transactions. Surely, MD’s remuneration is on the higher side which is a negative but not a red flag:

Related Party Transactions are not serious. Amount are small and a large chunk of that goes as rent to TCI which could be due to legacy reasons. TCI itself is a listed company, so no issues on this count.

Overall, I feel this could be a good company to buy but at a more reasonable valuation / need better timing. Currently, in an environment of rising fuel prices, 50+ PE seems to be on the higher side.

(Disc: No positions)

10 Likes

Group, i have one question. If we check tci express in screener.in we dont see any other companies in peer comparision section which is little strange for me. We have other logistics co like vrl, bluedart, snowman etc also listed.

Is Tci exp unique of its kind in market? Is it a monopoly ?

1 Like

Peer data is not accurate in Screener.

The management had guided a shift in unorganised to organised players in this sector but that does not seem to have happened.

Is it that unorganised players are still strong or the competition is now PE backed startups?

I think the competition is still a mix of all three categories – traditional players like Blue Dart, Gati, VRL etc., unorganized players and new generation PE / VC backed players. Unorganized competition may reduce gradually but not overnight and some of them may graduate upwards. New gen players should also not be ignored though the management says they are not a threat.

1 Like

An update from MOS: -

Motilal_Oswal_TCI_Express_Company_Update.pdf (1.2 MB)

4 Likes

Good set of numbers by TCI express. Firm has opted for buyback @ 2050 per share

Key points: -

TCI XPS marketshare is just 7% with 95% of the industry being unorganized

Current capacity utilization @ 85%

Final capex of 80 Cr utilized (part of last cycle) for devlopment & automation of sorting centre

Another 500 Cr Capex planned in next 5 years

Good improvement on working capital

Plan to double revenue by 2025 (est sales growth approx 26% CAGR)

Increase in customer base by 40000 in the last 5 yrs

TCI XPS q4 FY22.pdf (2.1 MB)

6 Likes

A detailed report on express logistics industry from Indian Chamber of Commerce:-

Express-Logistics-Industry-Report-2022_compressed.pdf (3.2 MB)

5 Likes