I think they would have taken it and its after CenVAT credit adjustment. Sorry, have limited knowledge on this, I may be wrong. Lets hear from others.

can you share concall ???

Hi,

You can access the audio file using researchbytes.com. Click here to visit the site.

Regrads,

Yogansh Jeswani

4 Likes

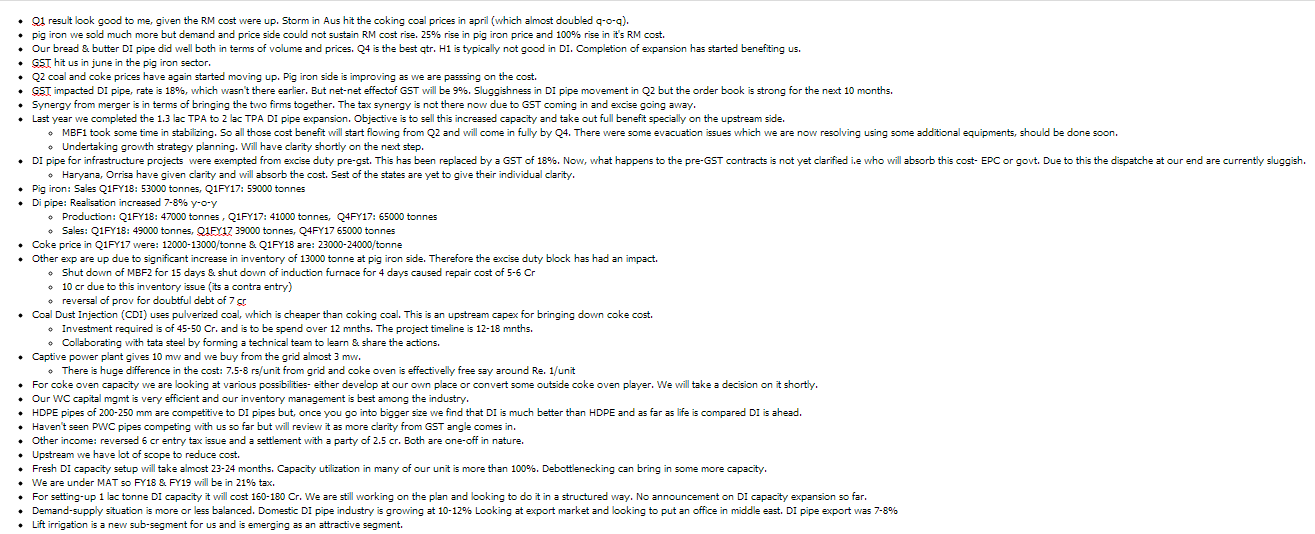

This is first effort from me there can be some mistake, sharing note from Q2 con-call:

- Q2 has been good because both the volumes and prices have gone up for PIG Iron, exact number 81896 pig iron and 45629 ductile iron pipe as against 52731 of pig iron in Q1 and 49036 of ductile iron pipes in Q1. There has been a slight drop in the sales of DI pipe, but that was expected due to GST impact and festival.

- What is important in pig iron is the spread. Last eight to nine year history of pig iron and coke spread average is 4500 per ton. Q1 2017 spread was 8000 from it come to 700 Rs. In Q1 FY 2018, now it is move to Rs. 2600 to Rs. 2700. Moving average could be Rs. 4000 to Rs. 4500.

- PCI project is in full swing, placed order for vital one, we are on track and want to complete before 18 months. one ton of coke will replace with one tone PCI. Price of coke today is about $350 and PCI would be $120, can clearly see the difference. 80 kg target is sure for replacement, TATA STEEL does more than 200kg, we are trying to learn from them.

- Full year volume can expect 5 lakh for hot metal and 2 lakh for DI pipe, DI pipe production more or less depend on size mix.

- Pig iron is purely sell in the spot market , ductile iron pipe is not a spot order, but it is a long-term order, order is book and that order is normally executed over six months or eight months.

- Therefore the finished goods price is fixed. Therefore what need to do is to focus on the raw material prices. so that we can fix that or reduce that. Spread the margin So in the case of pig iron the finished goods prices also change, but in the case of ductile iron pipe that remains constant for an order.

- The raw material is iron ore, coal, and coke, iron ore we have typically a long-term contract

and we buy mostly from Tata Steel, but it is at arm’s length and it is linked to the market price, but market price also there is a spot price and there is a long-term price so it is linked more to the long term, so to that extent the volatility is somewhat limited there. - Coal and Coke: 40% of coke consumption is captive, which means we produce the coke ourselves through a BOOT arrangement that we have in our plant and the coal is imported mostly from Australia. The balance 60% is open and that is what we buy in the spot market coke, but what we are trying to do is to link up that also on long-term about another 30% to 40%, so that at least 70% to 80% of that of our coke consumption is on long term, it is basically buying from Tata Steel on long-term basis and there also the price would be linked to coal and not coke. So that way what happens, we are able to limit our exposure to only coal prices and not both coal and coke

so what happens is that if the coking coal prices come down, our costs come down while our prices are fixed obviously the spread increase as well. - Current order book eight months for DI pipes, certainly 1 lakh tonne.

- Q2 was bad quarter for DI industry, inventories of some of the other players, suspicion is they are at a much higher level. we are much more reasonably placed in terms of both inventory and sales. we have refused to take lot of orders because of lower prices rather live with the old orders than book new orders at lower prices. some people may have sold, but we have not. We continue to hold the price.

- Ductile pipes volume growth will be anything between 10% and 15%.

- Capacity expansion for DI will probably take around 18 to 24 months.Current DI Industry capacity utilisation is not very high now. It is about 70%, 75%.

- The debtors have increased because of two reasons, one is that volume has gone up, second is the GST has increased the rate of 15% and the inventory also to the large extent for the coking coal and coke prices.

- Short-term borrowing has gone up 98 crore, but other financial liability that has come down substantially from 276 Crores to 199 Crores, but the other financial liabilities includes the current maturity of long-term debt so that has come down.

- Our internal target is long-term target is 1:1, but we will try to bring it down initially by 1.5 times.

Gross debt Rs.517 Crores. This includes Rs.100 Crores of preference shares.

5 Likes

I read that long term rating for this company has been degraded from A+ to AA-. I checked for the report in icra website and unable to find. Please help me in understanding this impact for the company and its future prospects.

Rating degraded announcement:-

http://www.bseindia.com/xml-data/corpfiling/AttachHis/9c5fa34e-b783-4574-9cbb-d56164f49830.pdf

The below information is available for the Tata metalliks in the ICRA Ratings report

Credit strengths

Improvement in cost structure on a sustainable basis – The company has commissioned coke-oven plants (under BOOT basis) and a 10-MW power plant in FY2017. The power plant is based on flue gas generated during the coke-manufacturing process. The recently commissioned coke oven and power plants along with the sinter plant, in operations from FY2013, has resulted in sustainable cost savings to the company.

High capacity utilisation and improvement in operating efficiency of the DIP division – The DIP division has been operating at full capacity levels in the last couple of years. Besides, a number of process-improvement initiatives were undertaken in the DIP division, which resulted in significant cost savings in the past few years.

Favourable demand outlook for DIP in India; healthy order book position for the company – The demand outlook for DIP is likely to remain favourable at least over the medium term, given the government’s thrust on infrastructure development. Moreover, TML has a healthy order book, which is expected to keep the capacity-utilisation levels at an elevated level, going forward.

Improvement in capital structure and interest-coverage indicator - Healthy accretion to reserves led to further improvement in gearing levels to ~2.1 times as on September 30, 2017 compared to ~2.6 times as on March 31, 2017. Interest coverage indicator remained healthy at ~6.2 times in H1 FY2018. With healthy accruals, the debt metrics is expected to further improve. ICRA expects gearing to improve to ~1.2x as at end of FY2018.

Established presence in the pig iron and DIP business; status of the company as a part of the Tata Group – The company is one of the largest producers of foundry-grade pig iron in the country with an installed capacity of 500,000 metric tonnes per annum (MTPA). A significant portion (~45%) of the hot metal produced is used in the DIP business, and the rest of the pig iron, primarily of the foundry grade, is used by the foundry industry to manufacture castings. TML is a 50.09% subsidiary of Tata Steel, with proven track record of financial support received from the parent in the past. The company also has established relationships with banks, which provides some degree of financial flexibility.

Credit weaknesses

Exposure of profit and cash flows to the cyclical nature of the pig-iron business - Raw material costs account for a major portion of the cost of operations for pig iron players, including TML, and are thus important determinants of profitability. The pig-iron sector, being a cyclical industry, is exposed to margin risks arising from temporary mismatch in prices of raw materials and pig iron, causing volatility in profitability and cash flows. The backward as well as forward-integration facilities available with the company, however, mitigate such risks to an extent.

L-1 based bidding system for orders results in range-bound profitability in the DIP division - Most of DIP’s sales take place through tenders where the lowest bidder is awarded the contract. This results in significant price-based competition, which tends to keep profitability under check.

Moderate capital structure - Notwithstanding improvement in capital structure, it still remains moderate. This is primarily on account of large losses reported by the company in the past which had severely impaired the net worth of the company.

2 Likes

Q3 results are outstanding. Revenue growth of 54% YoY and PAT growth of 110% YoY.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/7f902bba-ae32-4de8-b11f-487b6d1c1b86.pdf

1 Like

1 Like

Hi All,

Sharing my notes from Q3FY18 Concall, held on 8th Feb 2018.

* Cost push was significant.

* Coke prices went up by 3000/tonne.

* We were able to pass on the cost to a certain extent like: Pig iron by 2000/tonne & DI pipe a marginal increase.

* We have been able to increase volume and at the same time squeeze cost.

* Coke plant and captive power plant are running at full capacity, providing full benefit.

* Volumes should be similar to PY volumes.

* Iron ore prices have shot up in last 1 month.

* Due to 50% production cut in Orrisa mines due to SC orders (we depend on Orrisa mines)

* SC cancelled license in Goa mines, this dampens the sentiment. However, we are not impacted directly as these mines are for low grade ores which aren't used domestically.

* Our Biggest cost element is Coke (60-65%)

* 40% of it comes from captive source (BOOT)

* 40% we have tied-up a LT contract with Tata Steel. So, overall lower volatility from this front.

* 20% is from open market.

* DI pipe biz.

* Q4 is best for We should be able to do similar or better than Q3.

* DI pipe is competitve. It has 7 players.

* Most orders are long-term (6-8m) in nature. While, RM prices move daily.

* Oct was a festive month and impacted volumes. Else, could have done more.

* GST impacted us in the past as Pre-GST pipes were excise exempt. Matter now stands resolved in 90% of cases.

* Industry is at 70% capacity utilization.

* We are at 100% capacity utilization.

* We expect the industry to grow by 10-12%

* Actively evaluating growth/capex options. Planning stage is completed and are now making few bets. Will announce soon.

* Almost 60% of our total biz is from DI pipe.

* On receivable front we have some exposure to govt bodies but larger part (70-80%) is with big EPC like L&T. Where we secure the receivable with some instrument.

* DI pipe is a complex engineered product compared to ordinary pipe.

* involves several stages of processing.

* No major work on R&D front is happening in the industry. In past we took the technology from countries like Japan. We are gradually moving towards improving know-how efforts.

* Like to maintain EBITDA of 15-18%

* We were bleeding 3-4 years back. But, with rigorous efforts have halved our costs.

* So, operational know-how is critical. Won't comment on other industry players on this front.

* Pig iron market also looks good at the moment. We should be able to pass on the cost.

* Other Expenses b/w Q2 & Q3 are not comparable.

* Q2 includes 5 Cr prov for doubtful debt reversal & 8 Cr of excise duty adjustment.

* Order book is typically 6 to 9 months.

* Currently, it is near 6 months due to RM volatility.

* Increase in DI pipe price has not happened in line with our expectation.

* We are hopeful to achieve 100%+ capacity utilization in DI pipes.

* Geographic concentration is in East followed by central states.

* We are seeing orders from Orissa, Rajasthan, MP, WB. We have good orders from TN too.

* Volume Details:

* Pig Iron: Q3FY18 85000 tonnes (Q2FY18 82000 tonnes) (Q3FY17 42500 tonnes)

* DI Pipes: Q3FY18 50000 tonnes (Q2FY18 45000 tonnes) (Q3FY17 39000 tonnes)

* Net Debt is 500 Cr

* Inclusive of 100 Cr pref shares to Tata Steel

* LT Contract with Tata Steel:

* Iron ore for pre-defined Qty, Price is open.

* Coke 40%

* We look at contribution and make decision to take up the order in DI segment accordingly.

* We have best yield and rejection yields in the industry and try to maintain it by planning our contributions/product mix.

Regards,

Yogansh Jeswani

Disclosure: Invested

Note: These are my rough notes and it is possible that I may have heard/typed incorrectly. Please do your own due diligence.

5 Likes

Merger with tata group? the problem earlier was that TML was in deep red hence the merger was proposed. At the moment not discussing merger.

In Q1FY17, the spread were as high as 8000 per tonne which came down to 1000 per tonne in Q1FY18. at about 2500/tonne is at Q2 & Q3FY18. in Q4FY18 its a bit better.

Iron ore price has increased by 50-80% in short time in Orissa due to SC order. Coke prices have come down over last 1 month or so. Coal was about 240 or so at end of Dec and have moved upto 260 or 270.

Coke prices were $340 and now $370

10 MW power plant is helping us and will benefit 35-40 Cr on EBIDTA basis pa.

This year we are reaching 100% of DI capacity. We are in advance stage for growth planning. Looking at both organic and inorganic growth

9 Likes

https://twitter.com/ToshniwalEquity/status/1000227476390334466 ? negative for Tata metalliks

Went through the FY 2018 annual report of the company - http://www.tatametaliks.com/investors/annual-reports.aspx

Lots of cosmetic changes to the annual report. Improved transparency and focus on the several cost reduction and improvement measures undertaken over last few years, resulting into substantial improvement in results of the company.

Not much discussion about the future growth drivers. Company is already operating at high capacity utilization.

The DI pipe sector outlook is expected to be strong. The growth was lower for the industry in 2018 due to GST issues. During the year there was lot of volatility in raw material costs also which had impact on margins.

4-5 Mutual Funds hold about 7-8% stake in the company. Dolly Khanna holds 1.2%

7 Likes

Good insights in the interview: https://economictimes.indiatimes.com/markets/expert-view/q4-should-be-good-for-tata-metaliks-but-poll-uncertainty-remains-sandeep-kumar-tata-metaliks/articleshow/67539033.cms

Notes from Concall: Q3FY19:

Company is working on getting EC approval for a brownfield expansion. There is no concrete plan as of now to either go for greenfield, brownfield or acquisition. But, company doesn’t want to waste time if it plans to go for brownfield DI pipe expansion in getting approval. So, keeping things ready in back end.

Kharagpur we can grow DI pipe capacity

Economical expansion capacity will be 2 Lac TPA

Hot metal production was down 20% due to MBF shut down.

We are working on higher than full capacity utilization for DI pipe segment.

Coking coal has fallen in past 1-1.5 months from 225 to 200 od levels.

Coke price has also fallen by 2000-2500/tonne in past 1-2 months.

Current debt is 430 Cr

Will use both debt and internal accrual for capex plan. Final mix is not yet decided.

Current DI Pipe order book is for 9 months. At a similar realization as we have seen in FY19 so far.

We should see some bit of improvement in margin as the DI pipe orders are fixed price and RM has corrected in past few days.

Andhra Pradesh govt is coming out with a huge scheme for water grid. Roughly 6.5-7 Lac tonnes of pipe requirement.

We don’t have any pressure in terms of debtors at the moment.

Current industry capacity is 18 Lac tonne.

Majority of players are in East (11 Lac Tonne): Rashmi, Shri Balaji, Electrosteel, Vedanta and TML. (Rashmi & balaji are operating at lesser capacity but are aggressive with pricing sometimes.)

Other players are Srikalahasthi, Sathavana (non-operational), Jindal & … missed the name.

DI pipe realization for the Qtr was 41700/tonne.

Pig iron Realization have fallen to 30000-32000/tonne

4 Likes

Andhra Pradesh govt is coming out with a huge scheme for water grid. Roughly 6.5-7 Lac tonnes of pipe requirement.

This development can also be tracked through Indian Hume Pipe (IHP). Company has received orders worth Rs.900 cr in last 1 month from AP Govt besides orders mentioned in their 2018 AR. I had attended the AGM and management of IHP had confirmed that they also source DI pipes from other vendors considering the transport factor. They had received huge orders from Telengana govt in 2016 which is evident in their 2017 nos.

https://www.bseindia.com/xml-data/corpfiling/AttachHis/86d9528f-c916-4c2b-bee5-d1c95f465c8f.pdf

https://www.bseindia.com/xml-data/corpfiling/AttachHis/842cd978-62da-4c2e-a78d-ba870ffe5afa.pdf

IHP has also recently received orders from Madhya Pradesh Jal Nigam.

(Note: Above amounts are for projects on turnkey basis and may have requirements of HDPE / PCC / PCCP / DI / PVC pipes)

3 Likes

Summary of the Concall (source: capital market)

-

Tata Metaliks recorded a turnover of Rs. 546 crore and profit before tax of Rs. 50.91 crore for the quarter ended December 31, 2018. For the period of nine months ended December 2018 the company recorded a turnover of Rs.1561 crore and profit before tax of Rs.155.39 crore.

-

The company recorded highest quarterly sale of DI pipe at 66536 tonne in Q3 FY’19, which was 31% higher than Q2 FY’19 and 27% higher compared to Q3 FY’18 on account of robust order pipeline & good pull from projects.

-

Pig Iron volume however was lower at 61503 tonne in the quarter compared to 83984 tonne in Q2FY19 and 85045 tonne in Q3FY18 as a result of higher offtake of hot metal for DI pipe manufacturing and lower production by blast furnaces due to unscheduled shutdowns.

-

Price realization of both Pig Iron and DI pipe was marginally higher in Q3 FY’19 compared to Q2 FY’19 by around 2%. However, there was a cost push by way of increase in prices of iron ore, coal and coke.

-

The company has been able to keep its operating margin at around 14% despite furnace problems being faced in Pig Iron division during the quarter. The furnaces are now performing well and with Pulverized Coal Injection in these furnaces. The company is looking forward to improved performance of the Pig Iron division from Q4 FY’19.

-

Q4 of any year is usually the best quarter for DI pipe business when most of water and sanitation projects have necessary funds that need to be utilized within the financial year. However, there is some softening of raw material prices which may impact the net realization of finished goods.

-

Current order book stands at 8-10 months of orders in DI pipe business.

-

Tata Metaliks PCI (Pulverized Coal Injection) project has been commissioned, which is expected to improve the cost structure has been commissioned and is ramping up now. The company expects it to stabilize in January and the benefits should accrue in February and March 2019.

-

The company oxygen plant is coming up well and expects it to commission in Q1FY20.

-

Environmental clearance of the brownfield project is cleared by the appraisal committee of the Ministry of environment. However, signing of final EC is awaited. The company expects it to get in January. After this it will need clearance from state pollution board. All other statutory clearances are ready.

-

Total Debt is around Rs 430 crore which it expects to bring it down to Rs 400 by end of FY2019

7 Likes

As its just at planning stage, would take a long time (atleast 3 years) to commercialize. At the same time it upholds the hypothesis of limited players and strong demand

3 Likes

EC approval to increase capacity from 3 lac tonne to 5 lac tonne - https://www.bseindia.com/xml-data/corpfiling/AttachLive/ea239e27-4d00-4010-9724-142fdc6613d5.pdf

6 Likes

Pretty interesting development - https://www.bseindia.com/xml-data/corpfiling/AttachLive/e9465077-8611-4663-b8ba-6710b9523b4e.pdf

Co doubling the capacity of DI pipe from 2 lac tonne to 4 lac tonne! The project cost will be 555 Cr.

Interestingly, Tata steel (the promoters) are taking a preferential allotment and will infuse about 390 Cr (assuming approx price of 600 per share) into the company and perhaps their holding will increase from current 50% to maybe 75%!

As a material portion of project cost will come by way of equity debt shouldn’t increase much

10 Likes