Are these 3 competitors - Tata Elxsi, KPIT & Tata Technologies?

Tata Elxsi and KPIT are competitors. However KPIT is focused on auto sector only.

2 Likes

5 Likes

1 Like

Very good and more important consistent result .

Revenues from operations at Rs. 817.7 Cr, + 28.7% YoY

- Overall quarterly revenue crosses US$ 100 million for the first time

- EBITDA Margin expands to 30.2%

- Profit after tax at Rs. 194.7 Cr (3 years back quarterly profit was around 70 cr -now its almost 3 X)

- EPS grows 29.0% YoY

Other positive :

- Attrition down

- Best Innovation award from CII

- Esop to attract and retain talent linked to market performance

In my view Tata Elxsi core competence is design which acts as a key differentiator coupled with their strategic approach of strengthening the CORE and then also GROW more thru getting into adjacency vertical has been smart move .

Tata Elxsi 250123 inv ppt.pdf (2.6 MB)

4 Likes

Key Deal Wins ![]()

Selected by a global OEM software organization for a Software Defined Vehicle (SDV) program. Thisrepresents a strategic entry for next generation SDV and EV platform development.

• Tata Elxsi selected to set up an offshore center of excellence for EV system development for a leading USEV system supplier. This represents a multi-million multi-year engagement.

• Tata Elxsi won a design-led New Product Development (NPD) deal from a Global medical devices companyfor development of a home renal care platform.

• A leading broadcaster in EMEA selected Tata Elxsi to develop, integrate and deploy a next generationAdTech platform for streaming video services.

6 Likes

These 2 companies result confirm that ER&D space companies are able to buck trend compared to pure IT services companies

5 Likes

1 Like

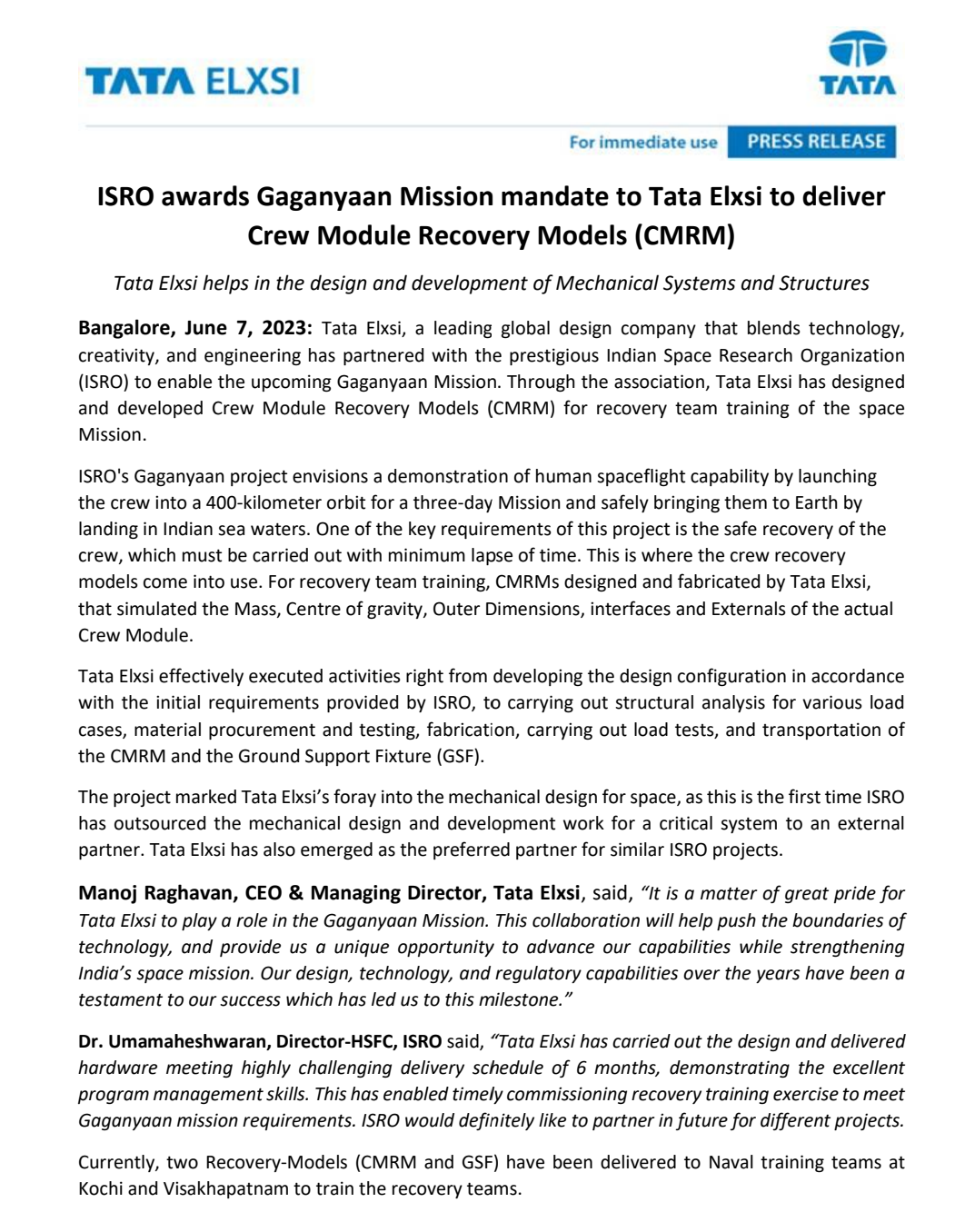

Association with ISRO. This is some development.

This is the first time ISRO

has outsourced the mechanical design and development work for a critical system to an external

partner. Tata Elxsi has also emerged as the preferred partner for similar ISRO projects.

10 Likes

one promoter having three IT companies - TCS , Tata technology ( filed document for IPO ) and Tata elxsi . Promoter may fix boundaries to three companies so that they may not compete with each other. so there will be limitation to growth for tata elxsi.

Dear friends, what is your opinion ?

1 Like

The projects Which TCS(IT Service) works and Tata Elxsi( ER&D)are different. The overlap will be minimal or very low. And Tata Technologies works in design and BMS , software to cars and other car related products.

So only whole three will not cross in a major way but minor overlaps might there

3 Likes

All Big IT companies like TCS, HCL, Wipro has presence in ER&D. % of E R&D may be low compared to overall revenue but some has >1 Billion USD revenue from this segment

Check below link on Automotive E R&D rankings.

https://zinnovzones.com/ratings/e-r-and-d-services/automotive/2022

you search TCS + BMS or other technology in google, you will find TCS is working there as well.

can say Tata Elxsi has more focus on certain domains and in current automotive cycle its growth will be higher.

3 Likes

Hi

Last paragraph would be more appropriate for KPIT.

TEL has good presence in Media, Medical devices etc.

Anyone would like to work with a specialist. Please bear in mind UT companies work with CTOs where as EnRD companies work with Design Teams there tend to have higher bargaining power.

Disc Invested in TEL and LTTS

1 Like

What are the advantages of adas of Tata elxi over like kpit etc

1 Like

KPIT is pure automotive ERD (engineering, research design) play while Tata Elxi is an ERD play across multiple industry verticals (e.g. automotive, healthcare, media, transportation etc).

KPIT has done really well in the last couple of years due to the EV tailwind in auto space while Tata Elxi financial performance in the same duration has suffered due to slow demand in some of the segments. So on a stock performance basis one may like KPIT a lot better although the valuations of the latter are now really stretched.

On a long term basis, however, I like Tata Elxi much better for the following reasons:

1- They have a highly capable management team and have come out stronger over several market cycles. Their transformation from generic IT service provider to specialized ERD player is quite remarkable.

2- They are diversified which gives them a natural hedge against downturn in a specific business sector.

3- Their operating metrics are much better than KPIT with better operating margins and cash flow generation.

4- Valuations have come down from 100 in 2022 to mid-50s today and I believe some of their underperforming verticals may have bottomed out.

5- Being a Tata company always helps in terms of reassuring to the investors from corporate governance and business longevity point of view.

14 Likes

Q3FY24 | Concall Notes

1. Growth:

Overall:

The commentary suggested by management indicates strong pipeline and good conversations going on.

EPD Division

- Transportation:

- Solid pipeline and prospects going forward, some deals expected to ramp up in Q4 and Q1 FY25. Business mainly coming in from Europe, Japan and rest of the world

- Focusing on business in Europe, Japan and ROW, both OEMs and Tier 1

- Being selective about OEM business in North America. Working only with those OEMs that offer good terms and commercials

- Some Tier 1 business going away as there in consolidation taking place in their business, some OEMs have started taking on the work that tier 1 companies did earlier and lastly because tier 1 companies are setting up captive centers in India

- Medical: Business has picked up since they’ve diversified from MDR business. Pipeline looks good for the next 2 quarters, beyond that they have limited visibility and aren’t sure if the growth witnessed recently is secular in nature, they are monitoring the same

- Media and communications: Prospects of this business remain highly uncertain. No green shoots visible now. This part of the business remains under stress. The management is working on retaining as much business as possible here. Recovery is no where in sight

2. Margins: Expect it to remain in the same range (27-29% types). No scope of further margin expansion

3. Hiring: Will go slow going forward. Have enough bench strength to cover existing and expected ramp up in business

4. General inference from the con-call: The next quarter or two the company is poised to do well due to the transportation and medical vertical.

Transportation vertical seems to be doing well overall. Medical vertical visibility needs to be tracked beyond 2 quarters. No visibility in sight for the media & comms vertical and the pressure is expected to persist heading into FY2025.

Disc: Invested

11 Likes

Overall some sectors , no visibility going forward and no major business pipeline from North America. Whats ur opinion, is this the right time to increase the weightage here?

1 Like

Personally, I’m not looking to add to my holdings here. I’ve added Tata Elxsi at various points between the years 2016 & 2020. The valuations today are too rich for me to add more for a company poised to grow its topline by ~15-20% in the medium term and with no margin expansion. Though, I’m very comfortable holding the stock as the company has great prospects.

7 Likes