Would there be any opportunity in semiconductor space for TATA ELXSI?

1 Like

Nope. They are two very different business. I dont think elxsi involved in this business

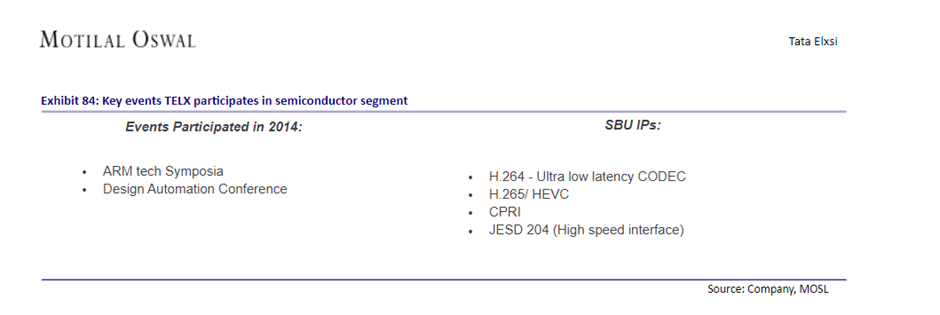

Media reports about the recent PLI scheme for semiconductors have mentioned Tata Elxsi as a potential beneficiary. The company reportedly has capabilities in chip design. A 2015 Motilal Oswal report mentions Tata Elxsi as a regular participant in semiconductor events.

The company website also mentions semiconductors as one of the industry segments served.

Click here for more details:

7 Likes

There is no confirmation about the company having semiconductor business.

Look at other companies who are already into semiconductor technology like Sasken Technologies

1 Like

6 Likes

Q3FY22 Results:

- Revenues from operations at Rs. 635.4 Cr, +6.7% QoQ, + 33.2 %YoY.

- EBITDA of ₹ 210.8 Cr; Growth of 14.8% QoQ and 46.8% YoY.

- PBT % increased from 28.6% in Q2 to 31.2% in Q3

- EBITDA Margin at 33.2%; Net Margin at 23.5%.

4 Likes

Awesome results all round. Good growth across all divisions. Only dent would be Client concentration and employee attrition both of which have gone up YoY and QoQ.

2 Likes

Launched new product to cover digital health capabilities.

2 Likes

Hi,

Following comments are generic in nature, and are not only related to Tata Elxsi, but for developing systems across India and could be applicable to IT services & products as well.

I believe that, there is huge opportunity in India to integrate all historical patient records, medical test results, treatments received, disease data, which can help doctors diagnose the current medical problem with 360 degree view of the patient.

There are hurdles at the moment in having this information at single place, due to fear of misuse of the information for selling medical treatments, products and insurance, but an attempt in this direction will make things more transparent.

In some of the developed nations where I have stayed long back, your General Physician have access to all data recorded in the centralized system in the past, and that avoids unnecessary medical tests which is common practice in India and also unrequired medication.

If such an integrated systems can be designed and developed here, probably that could be substantially good business opportunity for Tata Elxsi and other such companies, though involvement of Tata Elxsi could be limited.

There seems to be huge gap in the healthcare spend as percentage of GDP in India and Developed world, hence this can be harnessed if there is such vision.

2 Likes

Such a system would be in the nature of general business software, even though it maintains medical records. Tata Elxsi would not be interested in it. It would be in the domain of companies like TCS, Infosys etc. who write code and provide maintenance, customizations, enhancements etc. over its life cycle. It is the “normal” software development job, for want of a better word.

Tata Elxsi’s healthcare vertical is into very different type of work, such as create physical product design, write embedded software, help get regulatory clearances and so on. One look at this will make it clear:

12 Likes

I had heard the concall yesterday. I was positively surprised by management’s commentary - they mentioned for the next 8-12 quarters they can grow as fast as they grew in the last 8 to 12 quarters.

2 Likes

Even if you hear Q2 concall commentary, they said they have order visibility for 3x current topline for next 2-3 years. That is huge visible runway!!

3 Likes

How do we justify valuation for a company with 500 croresCr profit valued at 45000 crores which was a 8000 crore company some months back. 3 year sales growth has been 10% for last 3 years and Reverse DCF at this valuation shows it needs to grow earnings at 28% for next 10 years to justify this.

This is a quality company operating well in a niche that is growing but this feels beyond optimistic.

4 Likes

Very fair point and hence to me this is a compounding play. One might not expect too much alpha here unless it behaves like a TCS/ Asian Paints

1 Like

Confident of growing 6-7% QoQ; expect good margin performance going ahead: Tata Elxsi

4 Likes

I think with almost close to 9-10x growth since Covid lows everything is in the price…The rerating of the company is a big exaggerated as expected in the bull run, but still it can beat nifty and other big IT companies in the next decade…thats why entering early in a growth story is very important, as once the stock gets rerated there is not much left on the table for an investor arriving late due to FOMO

Yes agree. The story has played out. Same issue across a lot of names. IEX in 2020 seemed like a safe bet with secular growth story in a stable sector. Now it is being priced like the greatest thing since sliced bread.

I love these businesses but narrative seems to be following the price. This is expected of fund managers who will make all kinds of stores and names like “platformization”. But investors who fall in love with the stock also are guilty of this

4 Likes

4 Likes

This Article from Fortune India , Covered TATA Elxsi Extensively, worth looking at it  AI Powers Business at Tata Elxsi

AI Powers Business at Tata Elxsi

7 Likes