FAANG are extremely dependent on Indian IT. I had written off Indian IT for same reasons and stand wrong few years down the line. FAANG have DNA of new products and innovation. They need Indian IT to partner with them and grow their business as partners - otherwise they will not have bandwidth and capability to bring in the next innovation and their competitor who has partnered with Indian IT better would grow better. It is a symbiotic relationship and Indian IT are ready for that because of hard work they did last 5 years to focus on digital offerings and being partnership ready.

Some IT services globally which failed to do that like DXC are now getting sold as they are unable to grow and revive from tradition business stagnancy. Infact, if you see today, the most undervalued IT firms in India are on the contrary which hold IP and Products like OFSS. This maybe an anomaly today or Market knows something I do not - I do not know.

FAANG and Indian IT DNA is different - When I compared, I lost on huge Indian IT growth story.

I dont think PE expansion is 3X …my small quick analysis on this is:

Tata elxsi last 5 years PE was 25 ,now quoting at trailing PE of 44 ,last 3 quarters average profit is 84 cr per qtr ,compared to last year (3 qtr average )of 58 crores hence 45% increase …the share price before market collapsed in Mar 20 was around 1000 now around 2500 ,increase of 150% ,hence as per me 1/3rd because of earnings growth and 2/3 rd because of PE expansion

Just some quick thoughts on Tata Elxsi past performance .They were impacted by transportation vertical where Jaguar was not doing well , which is why they wanted to de risk ,hence their focus vertical to drive growth in recent past was media/broadcast and healthcare (they plan an acquition in this vertical ).Now looks like Jaguar coming back on track and both media /broadcast and healthcare doing well (here there is structural change because of covid )for which they are and will get benefit …hence their growth rate on top line will improve from 12% range ,operating leverage also in play which is why operating margin moved from 18-20% to 27% (trailing ),last quarter was 30% ,I think we expect it to be around 25% ,anyway this is a company /stock one wont be scared to hold because of the Tata group and performance .In between can the stock correct 30-50% ,offcourse it can but if holding period is longer (over 5 years ),how does it matter on a growth compounder like Tata Elxsi

Sell report on Tata Elxsi with TP of 1650/- .I am unable to understand why the analyst is lowering the PE multiple going forward 22 (against last 5 years of 25)when the company is in a “fly wheel” mode .Also surprised why factoring only 13% earnings growth when in difficult environment Tata elxsi have delivered 18% and 20% earnings growth in last 10 & 5 years respectively . MAY BE I am biased because of my holdings ,hence dont want to sell …anyone getting scared of the price rise ,i think should sell their shares and book 100% profit !

By the way the research company came with a sell report on Indiamart on 30th sep 20 ,after that the stock is up 60%+ and currently trading at 4 x of their target price (I dont hold Indiamart) .

Quite seperately I normally like their research report ,gives good insights on both sides .

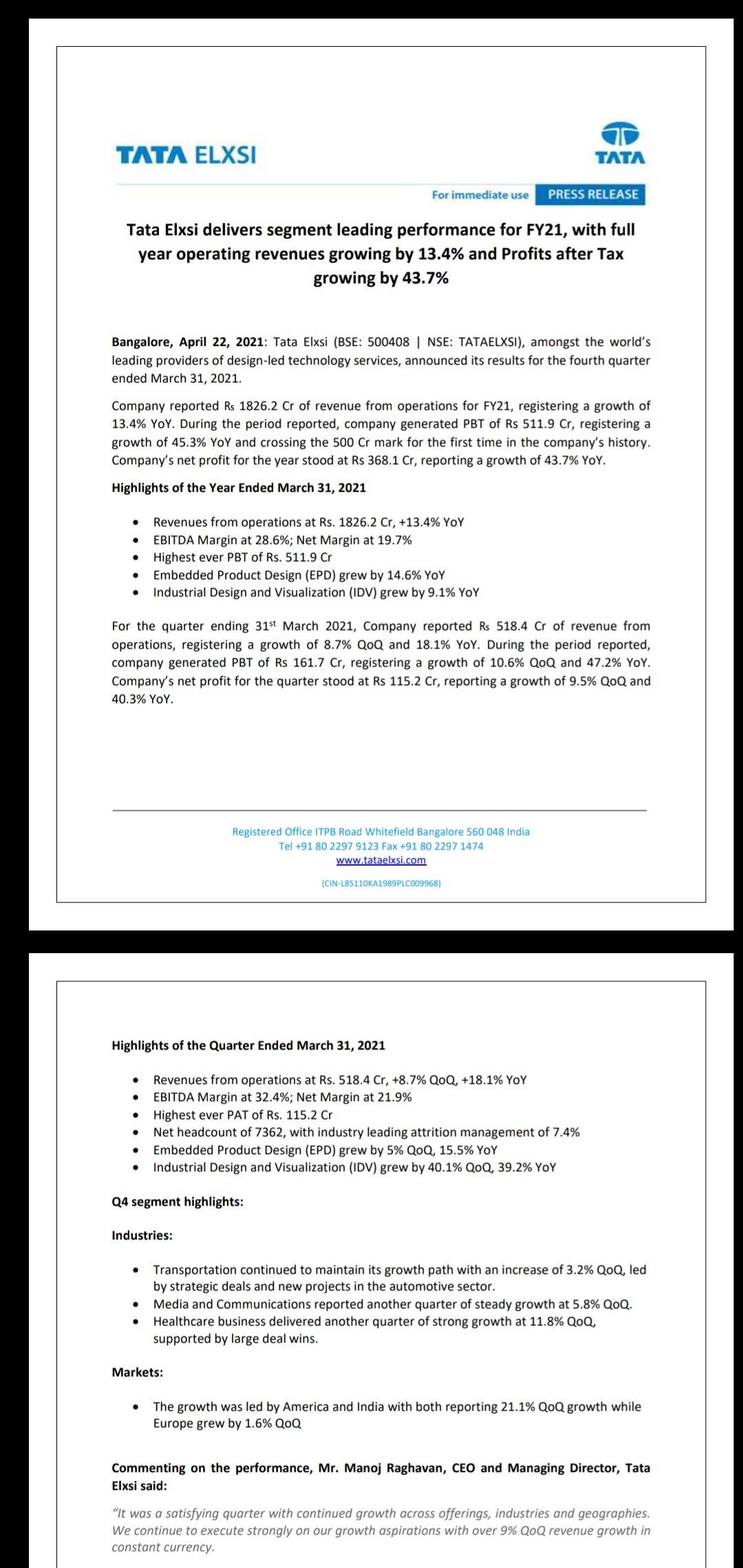

Tata Elxsi On Blockbuster Q3 :

-

Witnessing all round growth across geographies and verticals.

-

Operating margins are at 30% due to exceptional circumstances(less travel,visa expenses).

-

Utilization improved to 76% from 70%

-

Offshore leverage has improved.

-

Margin is highest in Healthcare followed by Media Communication followed by Transportation

so the growth in these segments and the product mix also helped improve margins.

Transportation Vertical:

- Revenue growth of 7.9% QoQ.

- strengthened team in both US and Europe.

- Looked at adjacencies like Rail,off road and commercial to reduce dependence on passenger cars.

- Business growing qoq and just a matter of time before we reach last years performance.

Broadcast and Communication Vertical:

- Growth of 24% YoY and 8% QoQ.

- Work from home,OTT,Broadband driving growth.

- While market was focusing on Automotive business company has been working diligently

- on executing on Healthcare and Media Communication verticals.

Industrial Design Vertical:

- Growth of 27.5% QoQ and 7.1% YoY.

- Business had been under performing,have made some major changes to improve performance.

- Segment contributed to both top and bottom line in Q3.

- Key segment that sets company apart from the competition.

Embedded Product Design grew by 9.3% QoQ.

Healthcare business had a growth of 24% QoQ.

95% Employees still working from Home.

One of the lowest attrition rate of only 6.1%.

Not shut down any offices,expect a balance in the future between Working from Home as well as office.

Company is well positioned and fully prepared to leverage the coming EV Wave.

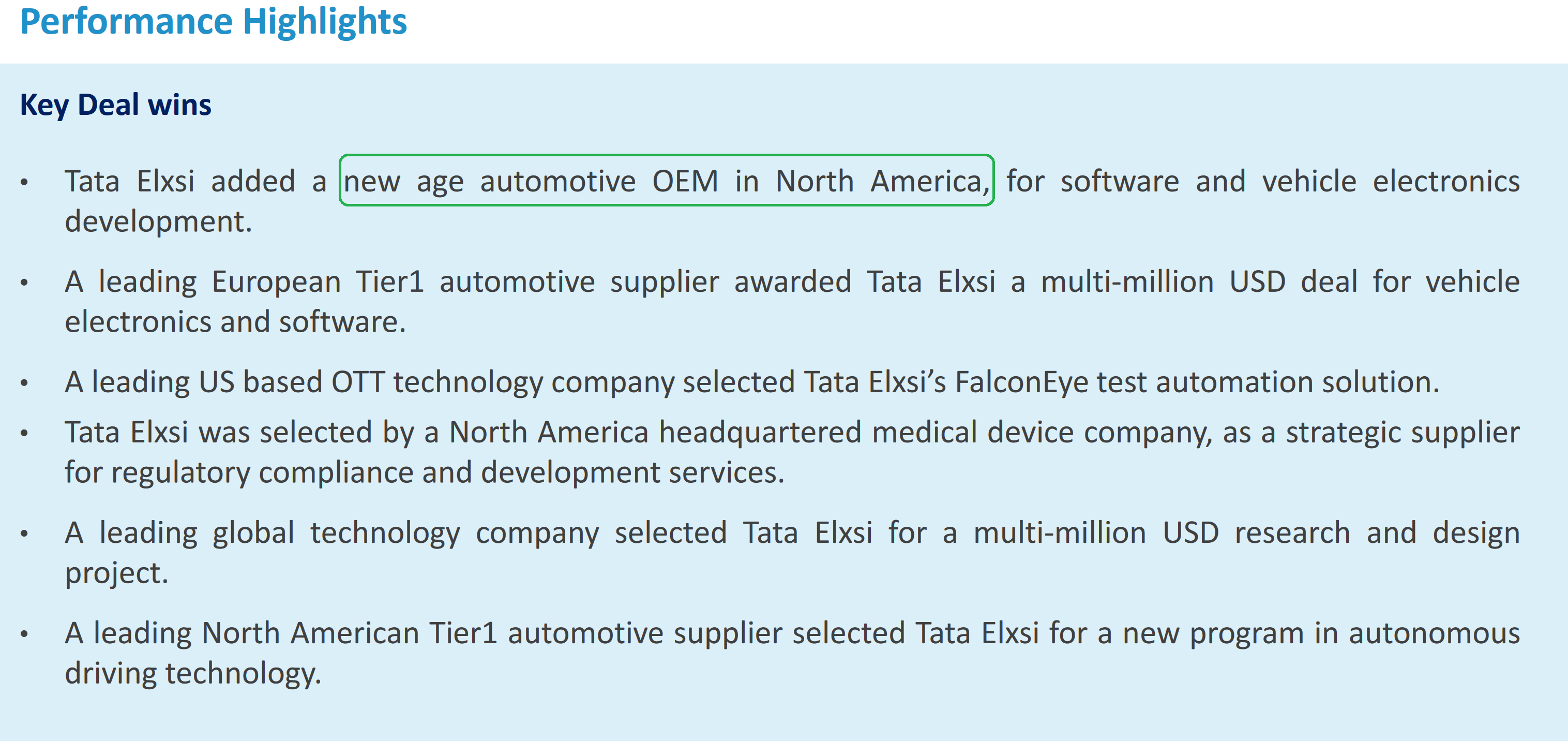

Any guesses who this ‘new age North American auto OEM’ is?

![]()

Source:https://tataelxsi.com/investors/Fact-Sheet/FY21-Q3-Fact-Sheet.pdf

Are you implying Tesla? If it is, then why won’t they take the company’s name directly in the fact sheet?

But I am a bit surprised. What was the concall for otherwise? or Why don’t they have a common concall with all? So many meetings will take significant management bandwidth

This would be GM, as TATA’s have worked with them before aswell

HDFC Securities initiates coverage on Tata Elxsi

Many structural changes in the Tata Elxsi story.

Revenues from the U.S. are now ahead of revenues from Europe, with most of the new growth now coming from the U.S.

| Revenue (Rs. Crores) | FY21 | FY20 | FY19 | FY18 | Change FY18 to 21 |

|---|---|---|---|---|---|

| India | 242 | 192 | 193 | 176 | 66 |

| U.S. | 667 | 558 | 490 | 410 | 257 |

| Europe | 644 | 659 | 706 | 607 | 37 |

| Others | 273 | 201 | 209 | 193 | 79 |

| Total | 1,826 | 1,610 | 1,597 | 1,386 | 440 |

Also, there are two customers with more than 10% contribution to the revenues, with the second customer almost equal to JLR in terms of contribution. Name of the second customer however is not known.

Lastly, Media, Broadcast and Communications is now ahead of Transportation vertical, contributing 45% of the EPD revenues as against 41% for Transportation.

Tata Elxsi - AR Summary 2021 - https://drive.google.com/file/d/19_1Hh0-IBPTFRpdxgFPt3pw_IAYUHpnB/view?usp=sharing

Please find the last 10 year’s analysis simplified in this video.

Almost like a thought leader award in the category - 3 awards for Tata Elxsi -great going on innovation Tata Elxsi - award press release 280621.pdf (465.4 KB)

Discl : Investment with high allocation in PF and hence may be biased

Annual report Synopsis and earning concall transcript for the complete year.

#TATA_ELXSI

Annual Report

Earning concalls

Impressive Q1 '22 numbers.

Edit : Investor Presentation

PBT affected due to additional Rs 33 Cr. of employee

expenses on account of the special one-time bonus for all our employees.

Geographical growth : America 17.5% QoQ and 69.3% YoY

Europe 5.4% QoQ and 30.1% YoY

India 2.8% QoQ and 47.6% YoY.

Business growth : Embedded Product Design (EPD) 7.5% QoQ and 31.4% YoY

Industrial Design & Visualization (IDV) 13.9% QoQ and 132.1% YoY

Vertical growth : Healthcare 19.3% QoQ and 80.2% YoY.

Media & Communications 8% QoQ and 31.6% YoY .

Transportation 3.4% QoQ and 20.1% YoY.

Company won large and strategic deals with both OEMs and suppliers in EV and autonomous technologies,

also won strategic deals in digital health, OTT and video platform development.

Commenting on the performance, Mr. Manoj Raghavan, CEO and Managing Director, Tata Elxsi said: We are entering the second quarter with a strong order book and a healthy deal pipeline across key

markets and industries.