- Have a good presence in Middle East/African region.

- Vietnam is running at peak capacity, and the order books are looking extremely good and encouraging.

- Planning for more capacity in Instant Coffee side. Instant coffee continues to be strong, and the demand is about 2-2.5% growth. The company has good traction in Russia. Instant coffee order book is full.

- Arabica Coffee prices have softened due to better supply. Robusta coffee prices will increase due to lower supply.

- Green coffee sales have done very well.

2 Likes

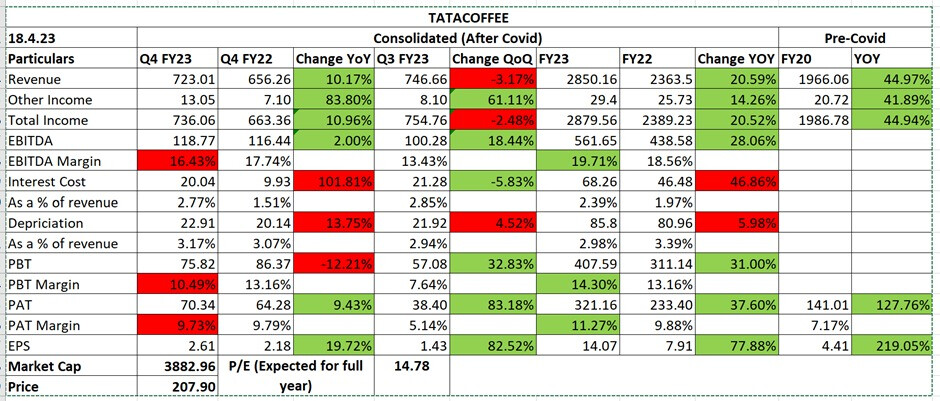

TATA Coffee Q1 FY24 Result Update:

- Merger of Tata Coffee and Tata Consumer is in the advanced stage and expected to be completed during the quarter.

- Company confident in improving the performance of Eight O’Clock Coffee and sees opportunities in the following quarter.

- Considering all options to support growth in Vietnam operations, including capacity expansion.

- Higher revenue generated from coffee plantations, higher realizations from instant coffee operations and better tea operations.

- The company’s operation in Vietnam was at peak capacity utilization. It witnessed higher sales for premium products and healthy order pipeline during the quarter.

- In coffee plantation business, the rainfall was deficient during the quarter which picked up in late July 2023.

- The tea plantations saw higher crops and better realizations during the quarter as compared to Q1 FY23.

- It envisages better demand for coffee from Africa in the coming periods. Instant coffee consumption continues to be on a secular path of growth despite the fact that there are several challenges in Europe where especially recessionary trends can be seen, but the instant coffee as a whole portfolio continues to grow.

- Revenue Mix: Plantation (Cultivation, Manufacture, and Sale of Coffee and Other Plantation Crops) - INR 143 Cr (20% of revenue). Value Added Products (Production and Sale of Roasted & Ground and Instant Coffee Products)- INR 5,80.1 Cr. (80% of revenue).

1 Like