TAAL AGM FY23 updates from Sept 26th 11am. This was compiled by a fellow shareholder (Yash), posting on their behalf. Thank him for sharing the notes in such a detailed manner.

Chairman speech:

Engineering design capabilities: company is on a robust growth path.

Merger of the subsidiary: there will be no dilution since it’s a wholly owned subsidiary. The rationale is to simplify the structure. The merger should be completed by Q3FY24.

Registered office has shifted to Bangalore.

Q&A speakers – Rohit Balakrishnan, Ashwin Dsouza, Rupesh Tatiya, Swechha Jain, Keshav Garg, Aayush Agarwal

Questions answered by MD:

3 areas: product design, construction, and infrastructure (architectural) and plant design (work for EPC companies).

60+ customers today. Number of customers have grown and business with each customer has grown.

Largely exports business. 70% US & Canada, 21% EU. Trying to make entry in Japan and Middle East.

No work for the defence sector in TTIPL.

Expect to retain the growth rates of the past.

Margins: built the business in that way. Have been very selective with customers. Margins are fluctuating because on site business has grown faster than offshore business. Over the longer-term margins will smoothen out.

Invested in sales and marketing team. Will pay dividends in future.

See good growth in all segments going forward.

Unlike KPIT are not automotive focussed.

Hired senior management particularly in the sales side.

Both the office are operating at full capacity.

Roughly 690 employees.

Have master service agreements and then get PO which are short term. Don’t have LT order book.

Top 1-5-10 customers: 13%-43%-60%.

Half to 1 million dollar is average ticket size.

In the EPC space don’t work for end customers. For other segments work with end customers.

Don’t have any aircraft. Entire business rests within the subsidiary and hence the merger.

Competetiors: many in Germany and France. Cyient, Axiscades, KPIT to some extents are competitors.

Recruit people based on orders don’t keep a bench of people.

106crs of financials assets: FDs, Investments, Bank Balances are major.

Any opinion about the current MD (Salil Taneja)? He led ISMT Ltd. as CEO in the period 2010 to 2015 (exited mid way to lead TAAL). During that phase, business’s operating performance was under immense gravitational pull.

Post GC years have been difficult for most business. No opinions on the ISMT CEO performance at that time.

Difficult to compare, since they are two different sector companies, ISMT was more commodotized compared to Taal business which is somewhat niche in IT Services.

Taal Enterprises was demerged around 2015 from Taneja Aero, when Salil took over. Taal Tech the main subsidiary (now 100% owned) was run by another person/co-owner, who left 3-4 years back, and since then Salil has been managing it also.

From AGM, my experience is, he does not over commit, never gives futuristic guidance, does listen to suggestions politely without committing. He sounds very boring in a good way. He understands that talking too much might be revealing certain things to competition, so refrains. I think he is doing well at Taal, and some directions taken by company have been inline with suggestions given in AGM. Thanks.

I sense an opposite personality in the letters to the shareholders during the ISMT stint. .Agreed that sector and industry dynamics are better in case of TAAL.

Can you share your findings about the ISMT promoters? I did a brief reading, and see below:

Kirloskar Ferrous Industries Limited (KFIL) acquired majority stake in the Share Capital of ISMT, making ISMT a subsidiary of KFIL w.e.f March 10, 2022.

ISMT Board at its meeting held on November 4, 2022 which was adjourned to November 5, 2022 has approved a draft Scheme of Arrangement and Merger between the Company (Transferor Company) and Kirloskar Ferrous Industries Limited (KFIL/ Transferee Company). Pursuant to the said Scheme and upon receipt of all the requisite approvals, 17 fully paid up equity shares of face value of Rs. 5/- each of KFIL will be allotted for every 100 fully paid up equity shares of face value of Rs. 5/- each of the Company. Not yet completed.

Anything else on the erstwhile promoter of ISMT can you weigh on would be helpful?

A lot of positives have been captured already in this thread, so I do not want to repeat them here.

But I am skeptical of the promoter quality. Performance of both Taneja Aerospace and ISMT has been poor. There was this aircraft accident in 2020 after which they shut down the business, and there was a bird hit earlier in FY17. This reflects poorly on the management. Accounting quality also needs to be scrutinized closely. When the aircraft accident took place in FY20, the losses were shown as Exceptional Item in the P & L, but when insurance claim was received, it was accounted as Other Income:

This inflates the PBT for FY21. More importantly this amount has not been deducted from PBT while calculating the CFO and so the CFO also stands inflated to that extent. Meanwhile, the aircraft continues to appear in the Gross Block under Right of Use Asset even today. I am not fully sure how this accounting works; but something doesn’t seem right here.

Salil Taneja has maxed out his remuneration at 10 % of PAT already which seems too high too early. I am also curious why a software company (Taal Tech) with a Gross Block of Rs.8 crores has Rs.1.42 crore of vehicles in it.

Have been holding Taneja Aero for the past 10 years. What I don’t understand is that when TAAL was their subsidiary, Taneja Aero was not reporting much revenues and profits from them - when it demerged suddenly the TAAL market cap is substantial relative to its origins

In detail, Taal Ent had two business, air flight charter (not so good due to multiple factors, and having only 1 Cessna plane), and a Technology Engg Service subsidiary. The Air flight charter business was closed after accident to the plane, and now the Engg Service subsidiary is being merged with Taal Ent. This Engg Service Tech business has grown quite well, and is the main reason. Earlier this was very small (hardly 12 Cr/qtr) and now over the years it had grown to nearly 45Cr/qtr. Employee strength has grown from 100 odd to 690 in FY’23.

The Company has had a presence in the Air Charter segment of the Aviation Industry.

The company was operating one leased Cessna Citation CJ2+ type of aircraft with a seating capacity of seven passengers. The aircraft was based at Pune airport and the Company had a loyal set of Charter customers centered around Maharashtra. The aircraft was maintained at the MRO facility of TAAL at Hosur in Tamil Nadu.

During the FY2019-20, the CJ2+ aircraft operated by the company veered off the runway during a landing, resulting in extensive damage to the aircraft rendering it inoperable and beyond repair. The insurance company has also accepted the aircraft as a total loss and accordingly paid the full insurance claim.

Now, the subsidiary, Taal Tech is the only revenue generating company, Taal Enterprise has zero business, that’s why both of these will be merged and made single entity.

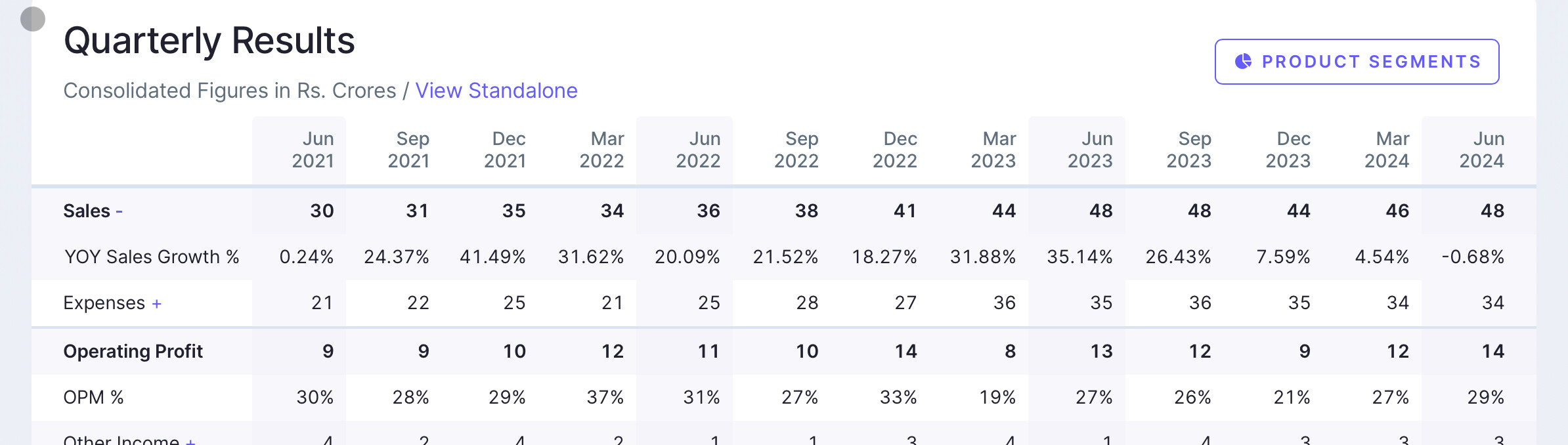

Decent growth in FY24 for the company. Consolidated FY24 EPS is now at Rs.119 vs Rs.100 in FY23. 19% growth in a tough year for other IT services company, is pretty commendable, although this is in niche Engg Design segment.

122Cr - Investments/Cash & Bank Balance,

Rev from ED Service is Rs.194 vs 159 ~22% growth,

PE at Rs,2600 is ~21. MCAP is 800Cr.

Did anyone attend the FY24 AGM? If Yes, request your views. It Would be great if you could touch upon: Why skipped the dividend? Any reasons for the OPM fall? Any plans for 100+Cr. cash or almost cash on the balance sheet? Overall impression. TIA.

Growth has come from existing customers as well as new customer addition. Will continue to strike a balance. Intent has been to prioritise the growth of our capabilties and share with existing customers.

Slowdown in growth rates attributable to sluggishness in the plant engineering business. See this turning around now.

Business split currently at 50% Product Development & Engineering, 35% Plant Engineering, Rest from Construction Engineering. Split more or less same as last year.

Customer count ~60+.

Margin fluctuations: due to hiring in advance of employees being placed in projects, variations in onsite/offsite employees ratio. Confident of maintaining EBITDA margins in a band of 25-30%. More likely to be closer to 30%.

Current employee count ~600. Manage this very carefully basis the demand that we see from our customers.

No revenue guidance, setting internal targets and track them.

This year, the softness in the growth has been because we’ve lost a couple of customers as they have been acquired. Identify this as a problem as TAAL primarily works with the middle tier of companies which are usually promoter driven and when the companies change hands, not in their control on continuity of the business.

Not keen on defence space - prefer predictable revenue streams and businesses without payable concerns.

Cash on books - deliberating utilizing of cash, yet to decide on it. Understand importance of improving return metrics and will take a call on this.

Capabilities - new areas added - auto embedded.

Capacities - looking to add more customers in existing domains or more capacities with existing customers.

While there has been no revenue guidance, do continue to see the employee count as a proxy to establish revenue growth and margins.

The slowdown/degrowth in employee addition trends are in line with the revenue trends and margin profile trends as the lower employee costs are getting absorbed over the same revenue base recently.

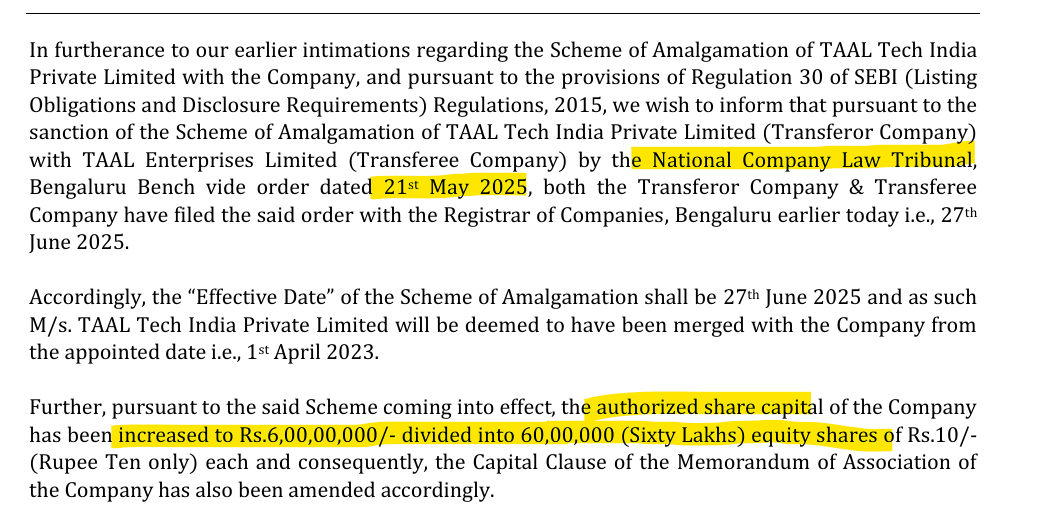

Finally after eternity, there is an Update on the Scheme of Amalgamation of TAAL Tech India Private Limited with TAAL Enterprises, NCLT sanctioned this on 21st May 2025, after 2+ years of wait. Bigger companies can get this completed in less than a year, but smaller companies it has been seen it usually takes1+ year, and for TAAL Ent it was very very long.

Interesting to note the increase in Authorized Share Capital are the merger of the subsidiary to 60L shares, currently 31Lakh shares are issued. So will there be a bonus possibility?