Pipavav shipyard, India’s biggest shipbuilder by capacity, will spring back to …

Read more at:

Pipavav shipyard, India’s biggest shipbuilder by capacity, will spring back to …

Read more at:

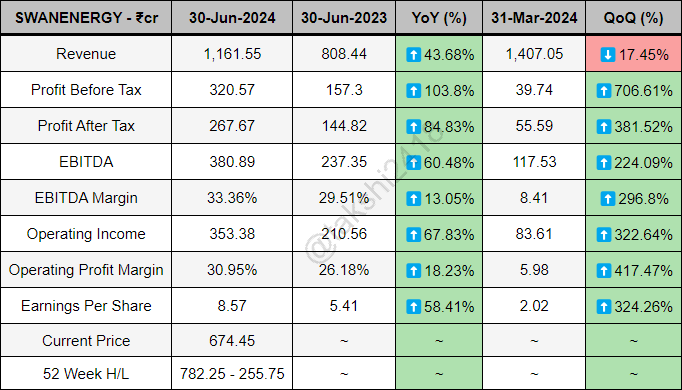

Q1 Consolidated Results:

Thanks to Takshi

Sheersh KapoorAugust 15, 2024, 3:42:34 PM IST (Published)

Swan Energy Ltd., an Indian multinational conglomerate with diverse interests, is set to sell its stake in a floating liquefied natural gas (LNG) terminal to Turkey’s state-run Botas for $399 million.

The Mumbai-based company disclosed the transaction in a stock exchange filing, noting that the deal is expected to be finalized within the next six months, pending approval from both shareholders and regulatory authorities.

The floating storage and regasification unit (FSRU), known as Vasant 1, has a capacity of 180,000 cubic meters. Swan Energy, through its subsidiary Triumph Offshore Pvt., owns a 51% stake in the unit, while the remaining 49% is controlled by Indian fertilizer giant IFFCO.

It is currently unclear whether IFFCO plans to sell its portion of the unit as well, as spokespeople from both companies have not yet provided comments on this matter.

The terminal was initially intended to commence operations at Jafrabad port on India’s west coast during the 2019-2020 period. However, its commissioning faced setbacks due to delays in port facility construction, exacerbated by the COVID-19 pandemic and a cyclone that struck in 2022, as detailed in Swan Energy’s annual reports.

Despite these delays, the FSRU was delivered by Hyundai Heavy Industries Shipyard in September 2020 and has been chartered to Botas since January 2023.

India currently operates seven land-based LNG terminals, but five of these facilities are running at less than 50% capacity. This underperformance is attributed to weaker demand and a shortage of pipelines connecting these terminals to the national gas grid, further complicating the country’s energy infrastructure.

The sale of Swan Energy’s stake in the floating LNG terminal reflects ongoing shifts in the global energy landscape and highlights the challenges facing LNG infrastructure in India.

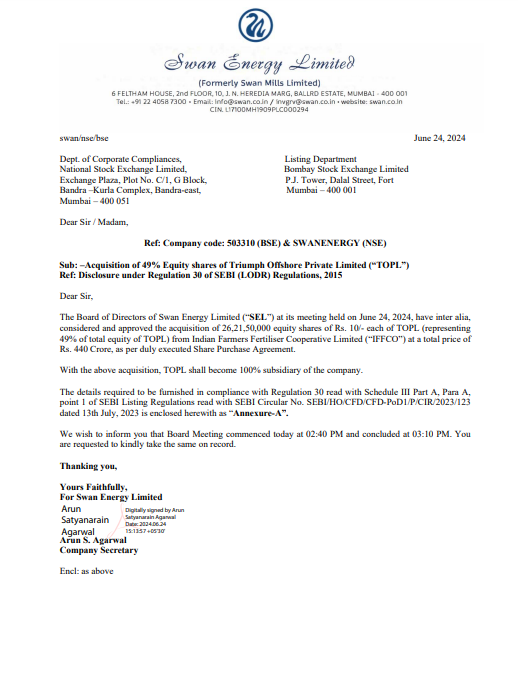

The remaining stake in Triumph offshore pvt ltd(remaining 49%), was acquired from IFFCO by swan energy in june 2024 for 440 cr.

now TOPL is 100% subsidary.

@kdjolly The reply was w.r.t CNBC tv article you shared.

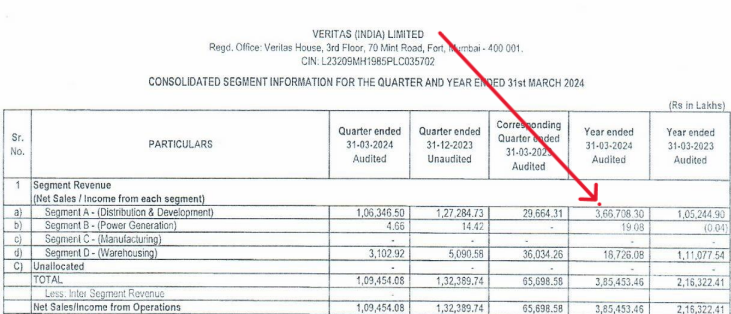

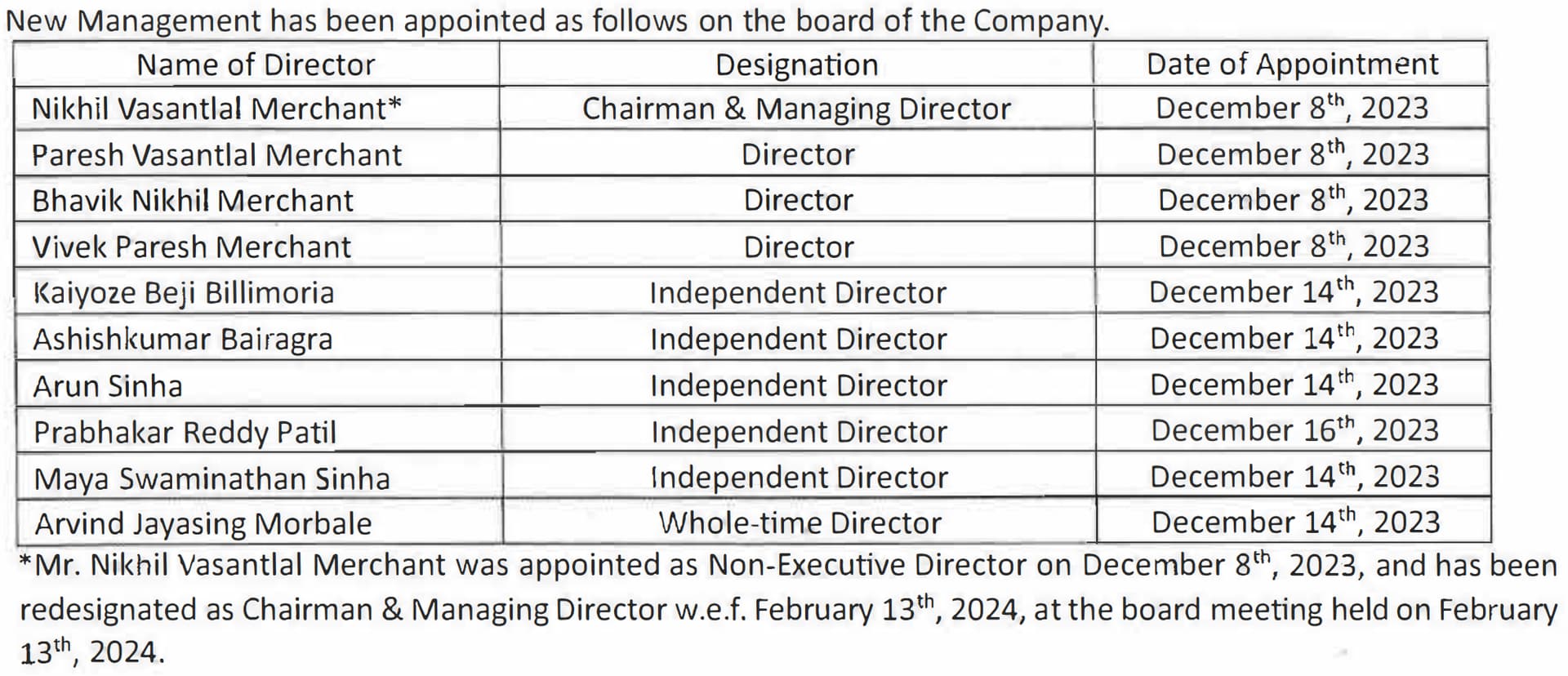

Operational Review for each business vertical of Swan Energy Limited based on the annual report for the fiscal year 2023-24:

The oil and gas segment was a major contributor to the company’s revenue, reflecting Swan Energy’s strategic positioning in this sector. The global energy market’s volatility was effectively leveraged to enhance both output and revenue.

The acquisition of Reliance Naval and Engineering Limited (RNEL) in January 2024 marks Swan Energy’s foray into the defense and shipbuilding sectors. This acquisition is a critical move toward diversifying its operations.

Swan Energy’s real estate division continues to focus on premium real estate developments in key Indian cities, with strong sales and potential future growth.

The Veritas division focuses on the petroleum products segment, which delivered solid performance driven by market disruptions and increased demand for petroleum products in India and Southeast Asia.

The textile division remains a critical part of Swan Energy’s diversified portfolio. Despite sector-specific challenges, the division showed resilience by maintaining operational efficiency.

How does FSRU sale impact their business?

The sale of the Floating Storage and Regasification Unit (FSRU) by Triumph Offshore Private Limited (TOPL) has significant financial and operational impacts. As per the board meeting on July 31, 2024, the company approved the sale of the FSRU to BOTAS for $399 million. This transaction is pending various approvals including from shareholders and regulatory bodies.

One of the key impacts of this sale is that it enabled TOPL to make a pre-payment of ₹82,481 lakhs to its consortium of lenders, marking full repayment of its outstanding debt on August 1, 2024(Swan). This move substantially reduces the company’s debt burden, strengthening its financial position. Additionally, this sale is part of the company’s broader restructuring and financial strategy to enhance profitability and operational efficiency.

The FSRU was earlier generating revenue through various charter hire agreements with international clients, including interim utilization as an LNG carrier for companies like CNTIC V Power Energy and Tema LNG. The sale of this asset marks a shift in focus from interim utilization to a more sustainable long-term strategy involving debt management and operational improvements.

As per Annual report 2023-24

Just one confusion. Has the 5 MMTPA terminal already been completed? Sources keep say it will be completed. In that case what explains the outperformance of the energy sector? Thanks

Swan Energy Limited (SEL) is developing an LNG port with an initial capacity of 5 MMTPA, extendable to 10 MMTPA, using a Floating Storage Regasification Unit (FSRU). The project operates on a tolling model and is 63% owned by SEL, with the Government of Gujarat holding 26% and Mitsui OSK Lines (MOL), the technical partner, owning 11%.

Key agreements include 4.5 MMTPA of regasification capacity reserved for GSPC, BPCL, IOCL, and ONGC for 20 years.

Construction progress has reached 83.95% as of March 2024, with major infrastructure like jetties and breakwaters nearing completion. The project has secured agreements for 90% capacity over a 30-year period, extendable by 20 years, ensuring a strong future.

Hi @DANGAR777

Swan is planning to sale Floating Storage Regasification Unit (FSRU). Any idea on the impact of this sale on the upcoming LNG port?

thanks

If Triumph Offshore, a subsidiary of Swan Energy, sells its Floating Storage and Regasification Unit (FSRU), it could impact Swan LNG’s operations and future revenue streams. The FSRU plays a key role in Swan LNG’s operations, as it is used for importing and regasifying liquefied natural gas (LNG) at the Jafrabad terminal in Gujarat.

Here are some potential impacts:

Operational Challenges for Swan LNG: Swan LNG depends on Triumph’s FSRU for LNG import operations. Selling the FSRU would require Swan to either lease or purchase a replacement, which could delay or disrupt the terminal’s operations. The Jafrabad terminal, scheduled to operate with a tolling model, would need this infrastructure to continue functioning.

Revenue Loss: Triumph Offshore has already generated substantial revenue by chartering out the FSRU before the full commissioning of Swan LNG. If the FSRU is sold, Swan could lose a significant revenue stream unless a new agreement is formed to continue using the asset on a lease basis.

Increased Costs: Selling the FSRU could result in increased operational costs for Swan LNG. They might need to lease a similar unit at a higher cost or invest in new infrastructure, impacting profitability in the short term.

However, if the FSRU sale is accompanied by plans for a new or more advanced unit, or if Swan Energy enters into a favorable lease agreement, the impact could be mitigated.

Swan Energy honestly has a lot of variables currently and its not a business we can predict based on the numbers as we do not know to what extent the numbers are cooked . It is more to do with political connections and how your connections help you to grow.

Just one insight which no one has brought into picture till now is the leverage of proximity of Swan LNG Terminal and the Reliance Naval & Engineering ( Pipavav Port )

This could bring in synergies in the long run with sharing of the resources .

The reason for sale of FSRU sale would be surely get the funds ready for Reliance Naval which is the biggest trigger from Swan Energy .

Nikhil Vasantlal Merchant daughter Vinita is married to Naman M Patel, who is the nephew of Mr. Anil Ambani who was previous promoter of Reliance Naval. The bid by Swan Energy for RNEL , clearly signifies the value the asset holds and is timed to perfection with the impetus currently shown by our government towards Warships and private participation

Also , once the LNG terminal is up and ready , either Swan could give Reliance Naval the contract of building an FSRU provided it has the capability and capacity to build one or else take one on lease .

Some more interesting points.

The articles of the company were amended recently which included 2 new business areas

The recent QIPs with Quant MF participation & BlackRock ( Jio connections again ) buying stake from the open market do give a validation to an extent that there are variables which may turn favorable for Swan in the coming years .

In addition , Mr. Nikhil Merchant in his personal capacity had invested in the preferential allotment of Balu Forge. What are the intentions of the investment are really unclear to me but if any board members can find more details it would be really helpful.

Their political connections cannot be doubted as IFFCO was holding 49% in the FSRU . IFFCO moved to NCLT against Swan Energy in March due to Swan wanting to prepay the loan by issuing shares to the lenders which would dilute IFFCOs stake. IFFCO did an out of court settlement with Swan in June and Swan bought IFFCOs 49% stake and then decided to sell off the FSRU at a profit . Swan made a mockery of IFFCO partnership and profited IFFCOs share in just a span of 6 months

To me the triggers are in the below priority

Disc : Invested & biased

These reports would more often than not be motivated to increase and pump up the price . I would take these reports with little to no confidence .

If u are investing in Swan or Veritas you are not investing in fundamentals but taking a bet on the promoters . As I mentioned previously , there are alot of variables in play and none of the forums members can predict the outcome of the variables .

The outcome can be both extremes so invest only the amount of money you are fine to lose . Connections can lead you to favours which cannot be apprehended from a logical point of view .

When I had invested , I was thinking of FSRU vessel as an advantage , now they have sold it off so overnight things have changed .

Just a thought : Some on the street compare Swan to Adani . Well Swan is going the same route but now Adani has become a giant who I do not think can be runover even when the political parties get switched over .

Seeing Adani acquisitions for quality companies like ITD Cementation is only making their business stronger which cannot right now be said for Swan . What future hold for Swan is unknown

These scripts we cannot be evaluate on fundamentals or we cannot even rely on their books as there would be a can of worms waiting to be uncovered .

It can only be valued , how do you see their connections playing to their advantage. Invest with caution and if u are ready for both extremes

Arihant Report on Veritas

Veritas_India_Ltd.pdf (320.4 KB)

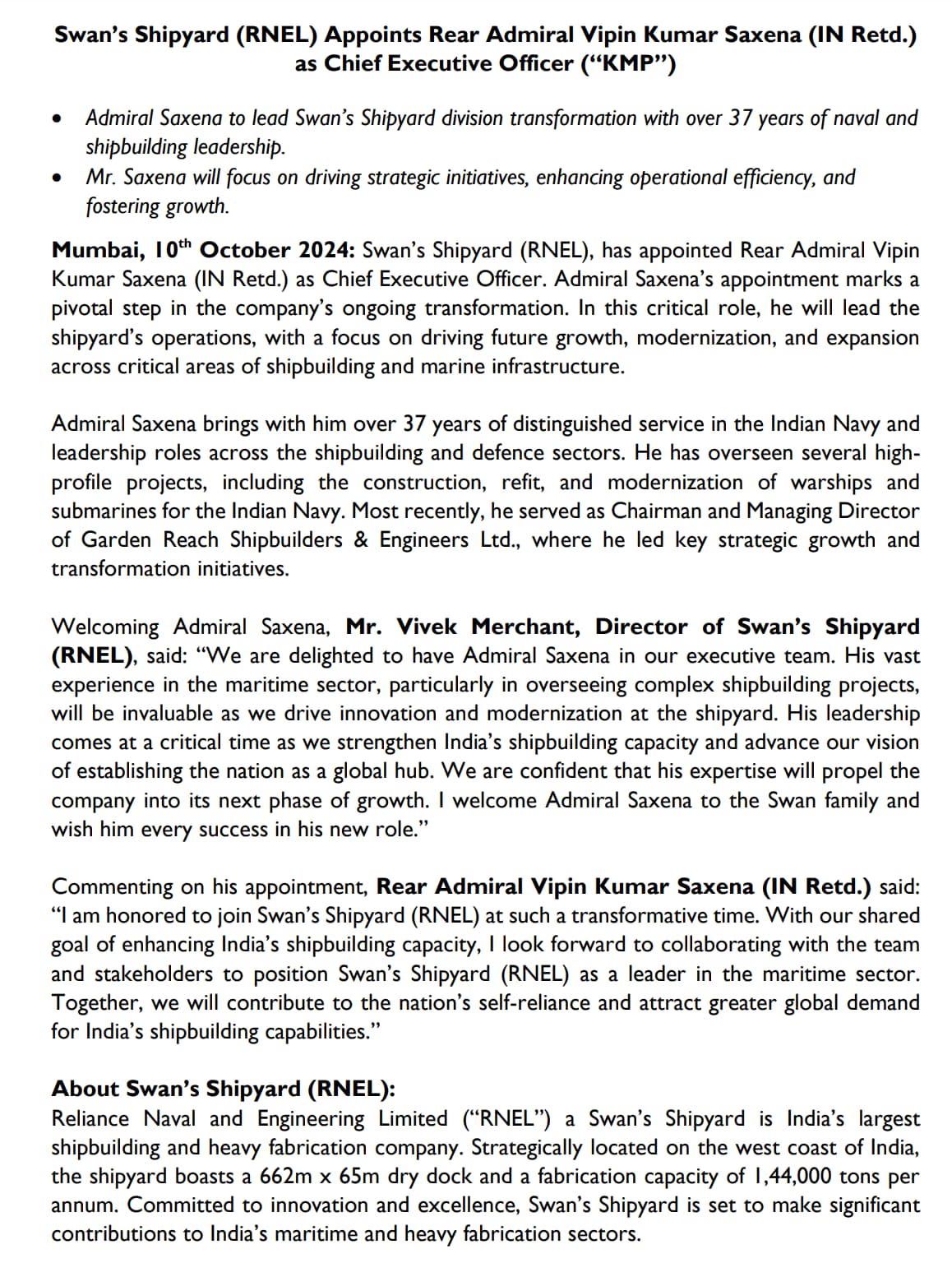

Press Release from Swan’s Shipyard:

Also Check out the integration of the shipyard division in the Swan’s website:

Reliance Naval Business Revival and Continuity Plan

The new management of the company is revitalizing the business through a comprehensive approach that strategically targets key market segments and establishes a clear roadmap to secure a competitive edge by focusing on 5 key levers:

a. Liquidation of WIP vessels and inventory: The company acquired 8 work-in-progress vessels presently at the yard and has received offers for liquidation of the OSVs.

b. Focused business strategy and sustainable revenue generation: The company is focused on building and converting a robust commercial pipeline by global and domestic reach outs for shipbuilding, repair and offshore fabrication opportunities. The company has received their first repair order starting in August 2024 and will be operational for new build from December 2024.

c. Yard Readiness: The company is currently reinstating and operationalizing the 600+ acres shipyard. As of date, the shipyard is ready to dock vessels and provide general repair services and is in the process of fully restoring their fabrication facility.

d. Organization building: The company is also focusing on talent identification and recruitment.to build a capable workforce.

e. Capacity augmentation: The company is also actively engaged in planning for additional capacity to integrate a maritime vendor ecosystem and meet the global demand by increasing docking and berthing space. They are in the process of building a comprehensive yard design and layout strategy.