Supreme Industries trying to emulate the model from Astral. Connecting with the plumber community and conducting workshops to make them ambassadors of the product. To watch this space if this can increase the retail share of Supreme Industries.

Excerpts from 2020-21 annual report (page# 46)

With the help of specialists the Company has embarked upon a new activity with nomenclature as “Plumbing Workshop” which is a full day session with Plumbers. Here the sharing is of latest Plumbing techniques along with applications of new products introduced by the Company in the recent past in the range. The markets have well appreciated it and there is

pressure on Company to increase the Plumbing Workshop numbers substantially. The Company could organize only 61 Plumbing workshops in the year 2020-21 owing to corona

pandemic. Company plans to continue organizing the Plumbing Workshops based on situation during the year 2021-22. There are now more than 90,000 Plumbers connected with the Company.

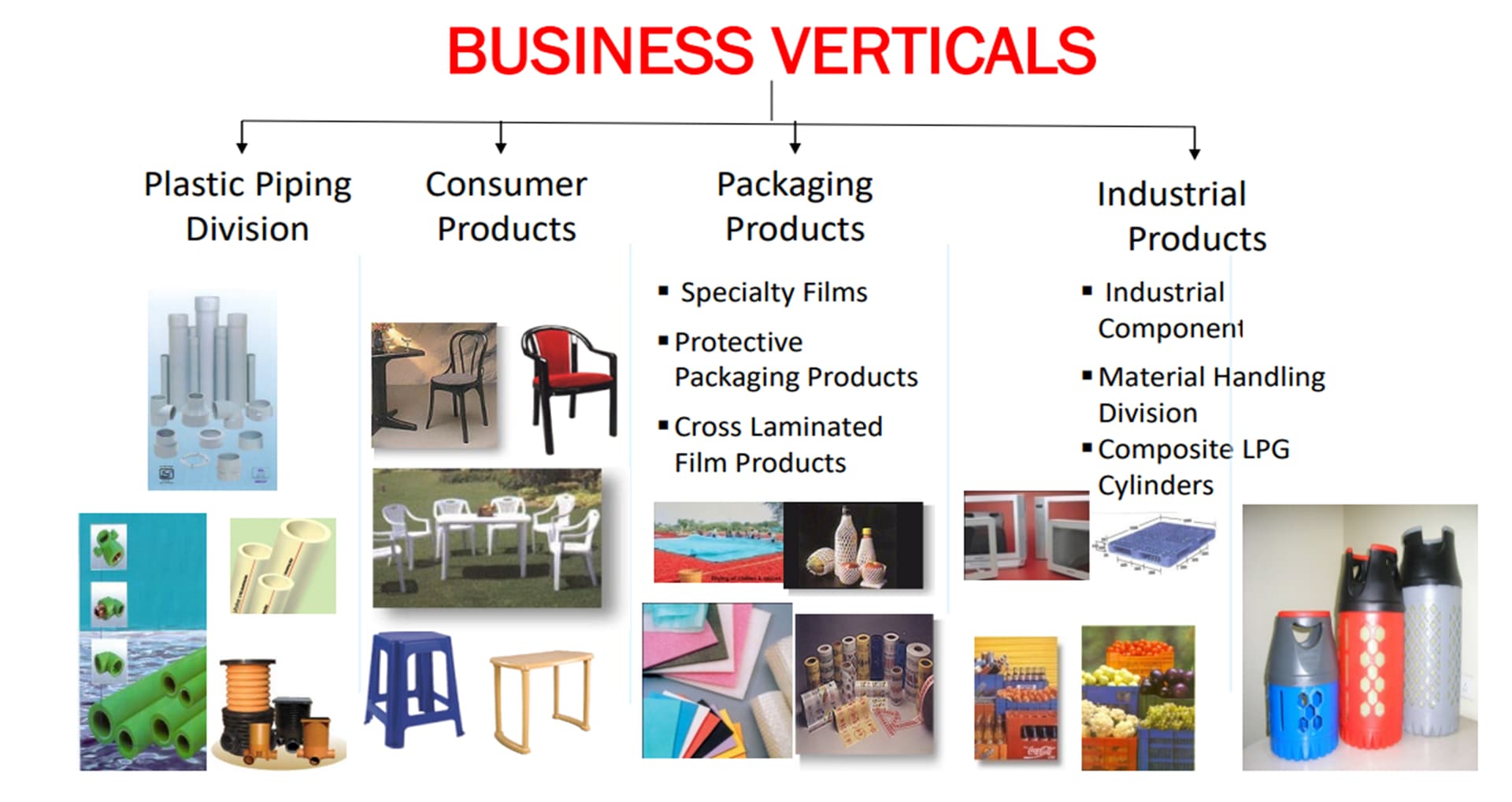

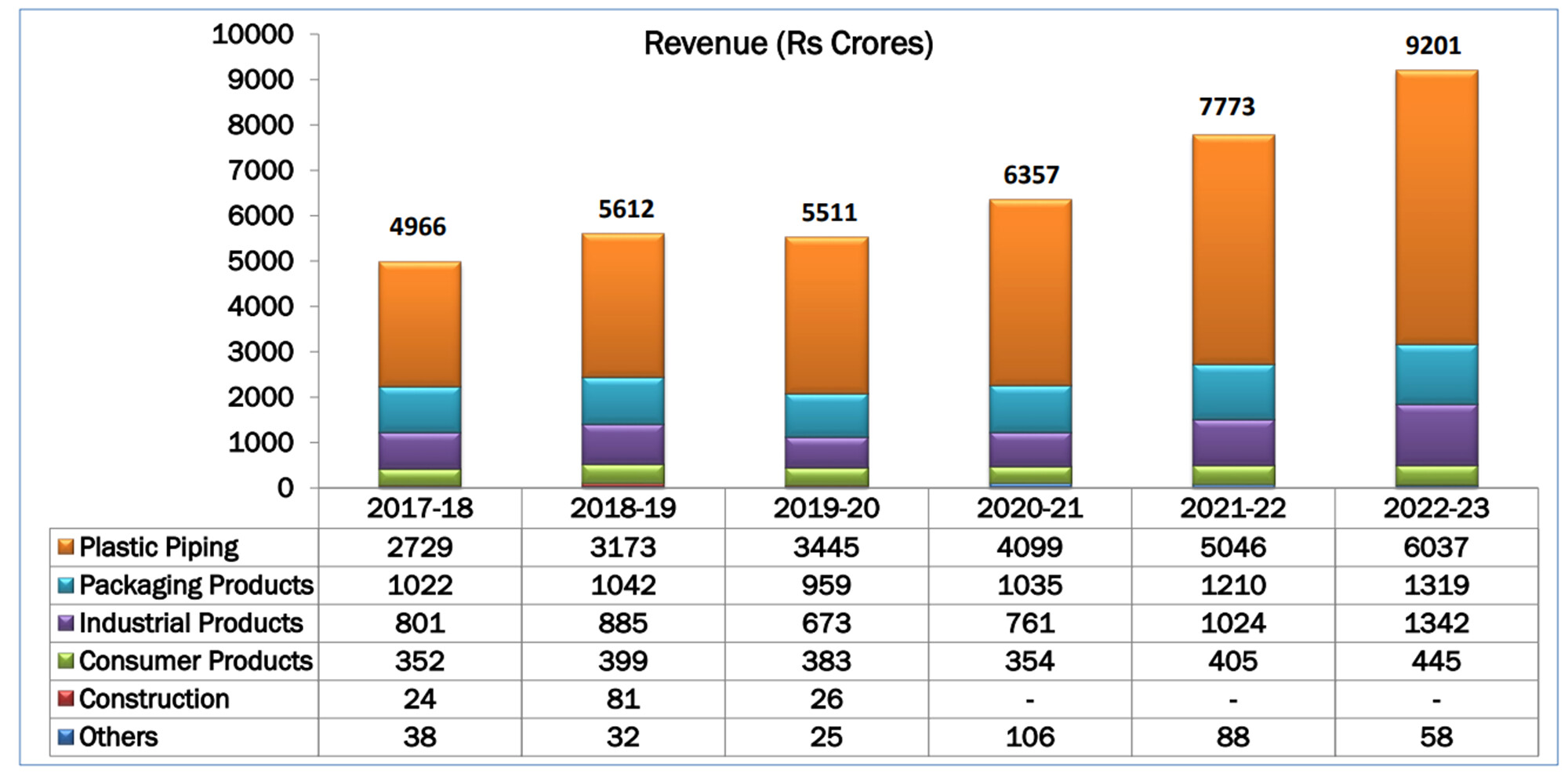

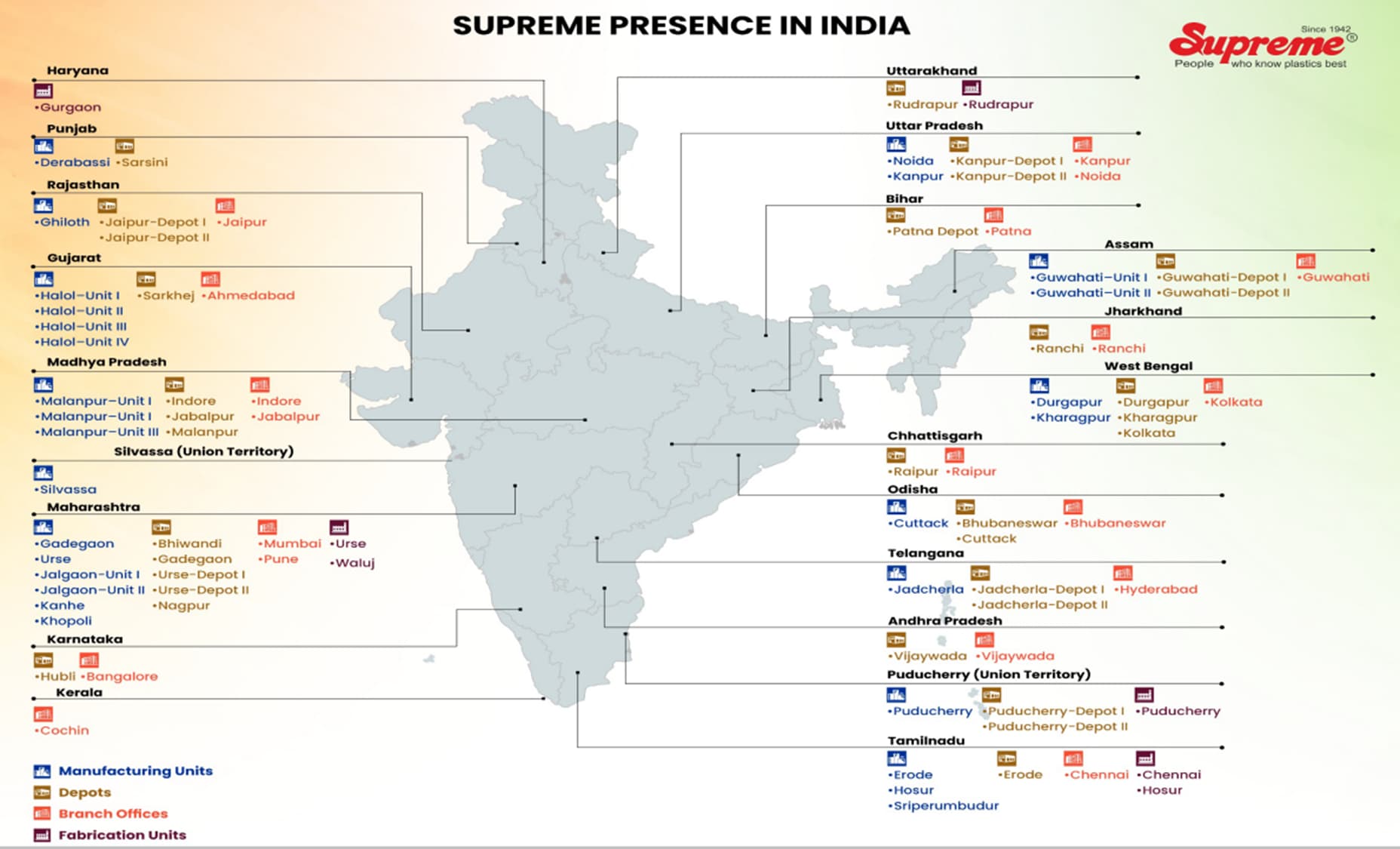

This is a peaceful company to own. With well diversified manufacturing facilities, distributors & products. The company has a leadership position in all the segments it operates & running more than 20 manufacturing facilities across Country.

Below are the segments its operates & revenue contribution -

Plastic Piping (66%)

Consumer Products (5%)

Packaging Products (14%)

Industrial Products (15%)

Others (1%)

This company is a typical example of how great companies remain great. (81 years in business).

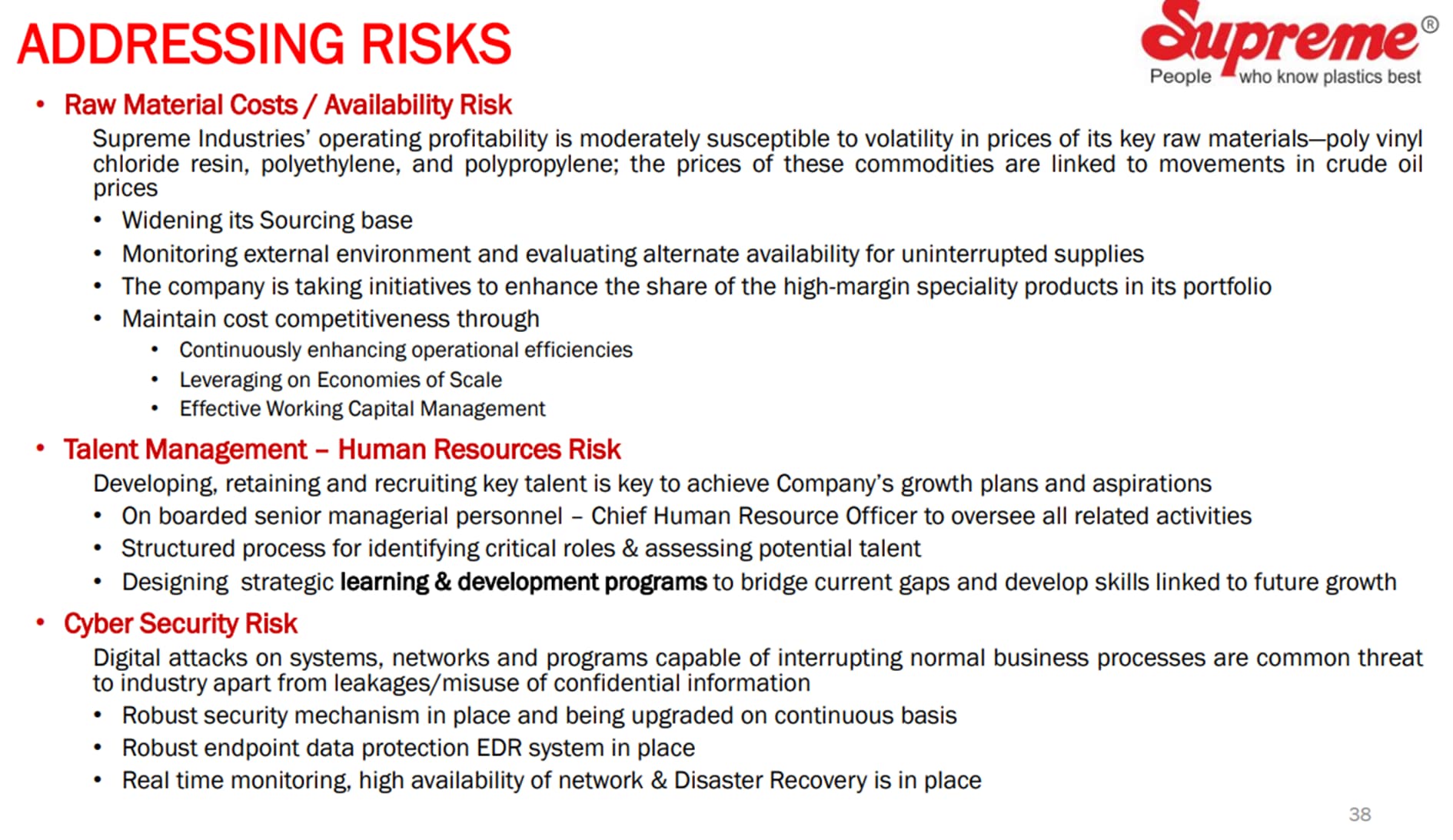

However, the most concerning things abouts this company are 1) no clarity on Management Succession plan 2) volatility of raw materials.

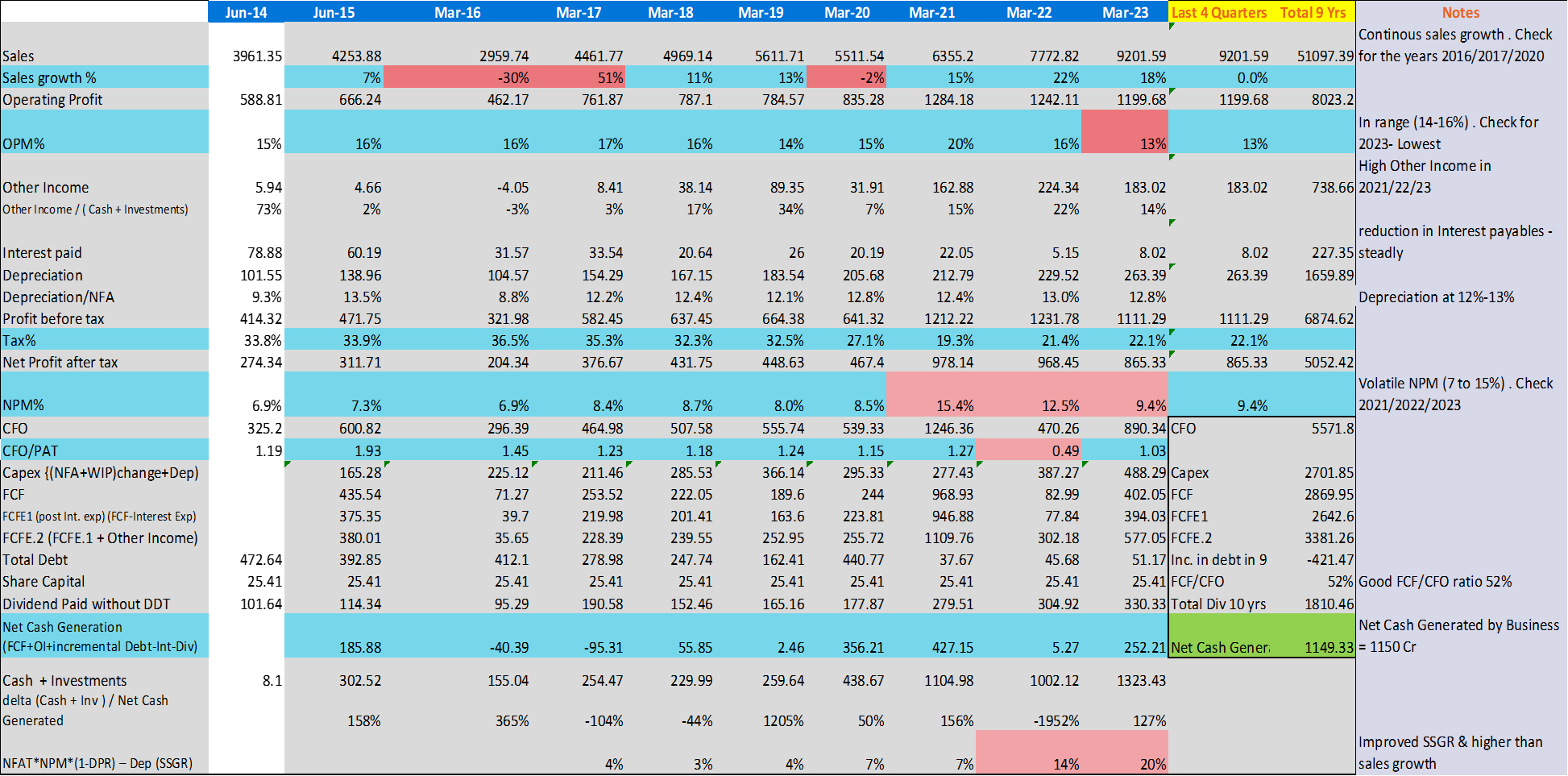

Financial Analysis Summary -

Balance Sheet looks good at high level - Funds are generated using profits & used for Net Block, debt reduction, Cash balance, Investments.

Outflow to Inventory and Receivables is in-line with the sales growth

Other liabilities increased due to increase in trades receivables

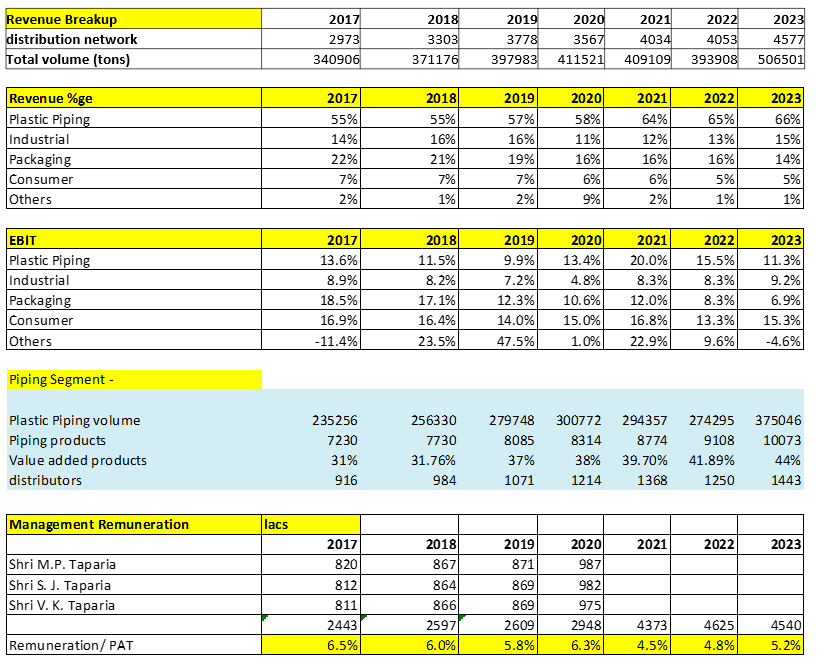

Dividend issued is always ~35% of PAT

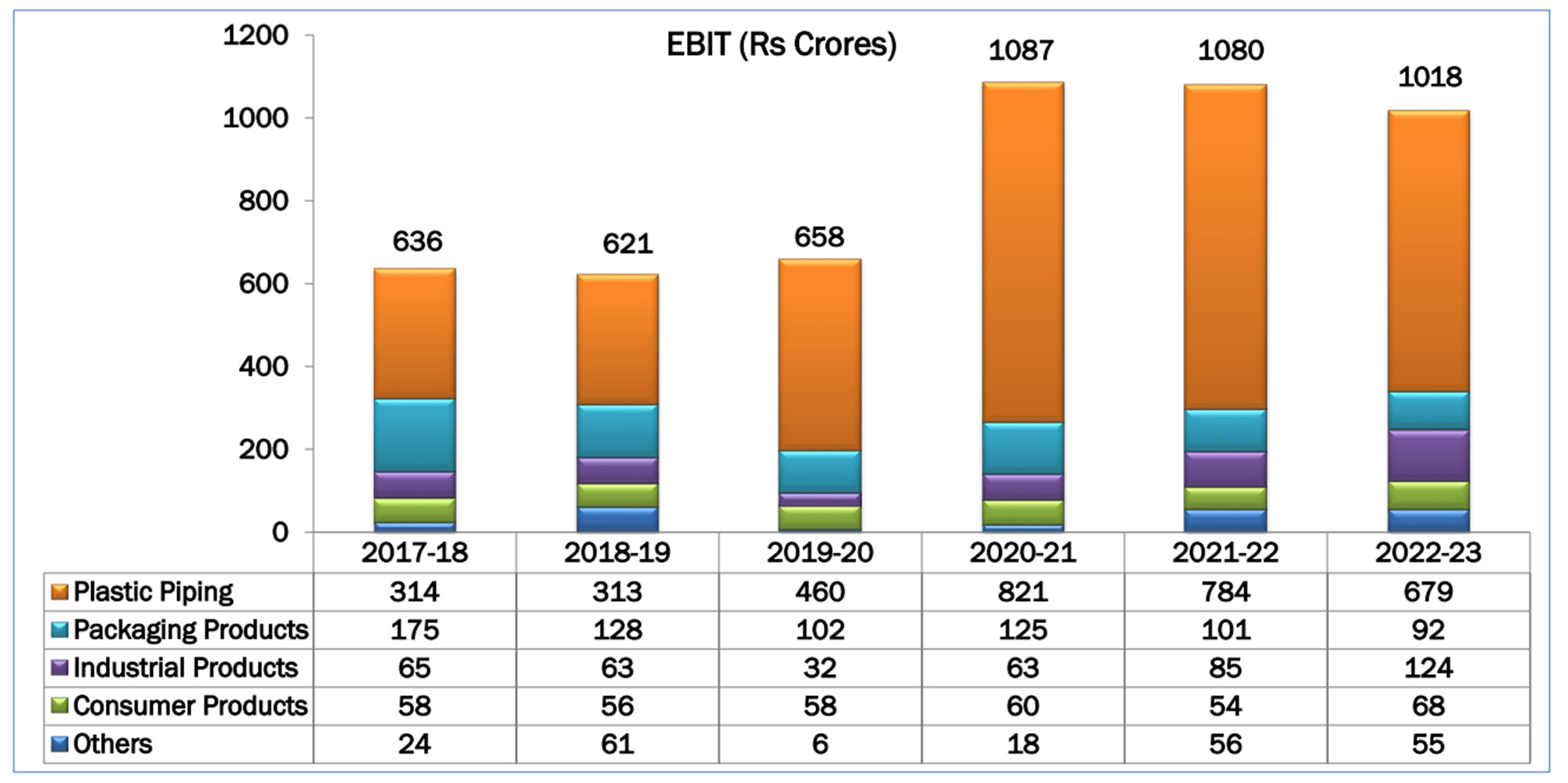

Continuous sales growth with range bounded OPM% (14-16) (check 2016/17/20)

High Other income in the recent years

Volatile NPM% (7 to 15%), check 2021/22/23

Good FCF/CFO ratio

Improved SSGR & higher than sales growth

Net Cash Generated / CFO is 20%

Depreciation 12-13 (in range)

Stable operations ratios

Controlled/Low debt

High return ratios (check for 2016)

Costs under control - Fluctuation raw material costs

In addition, an investor notices that until FY2015, the company used to follow a financial year from July to June. In FY2016, the company changed its financial year to end in March. As a result, in FY2016, the company covered only 9 months i.e. from July 2015 to March 2016. Therefore, all the financial data for FY2016 comprises the performance of only 9 months. In the years before FY2016 and FY2017 onwards, the reported performance is for 12 months.

Prices have bottomed out.

Volume growth is expected 20% in FY24

Demand for Agri and Residentials is favorable.

Growth in plastic pipes is around 20-25%

Rev guidance 11,000 cr with 14% OPM…seems like the street has already priced it in for FY24. In past its given very less no. of chances to enter, looking at prices closely to enter.

I recently watched a podcast of a senior analyst from Nuvama where she mentioned about the value chain of Pipes and fitting industries.

Insights I got:

Pipes and fittings is a bulk industry where the bigger player is getting and the smaller player is getting smaller. So the question comes in mind, why is this happening? The major raw material for pvc pipe is PVC resins and the major suppliers of resins are likes of reliance industries, Chemplast; and when big companies such as supreme or astral goes to procure resins from reliance, they have a bargaining power, incremently they can procure it at 2-3% discount. This reminds me of the moat of APL Apollo where they purchase raw material at a marginal discount rate from the Iron n Steel players. And on the other hand, small players lack this bargaining power, at first they can’t directly go to Reliance or Chemplast to procure resins, they have to procure via distributers and in this chain distributer wll have a cut of 3-4%.

Additionally being a bulk material, that needs to be transported from plants to the retailers incurs significant logistics cost. And only big player, Supreme has plants in various parts of the country, they can save on logistics supplying it to the retailers, on the other hand small players lack this scale. This reminds me of Ultratech where the company have various plants all across the country. PVC pipings industry is a commoditised economies of scale business, where the lowest cost and the most efficient manufacturer is poised to well.

Supreme and Astral are clear leaders. This industry has witnessed the significant value migration from unorganised to organised. Supreme is guiding to increase its revenue at 25% CAGR where all other players are downsizing their estimates. The next leg of growth in this sector can come from introduction of OPVC pipes as government wants to replace DI Pipes by OPVC. Additionally, in western countries usage of plastic doors and window panels are common (made up of UPVC) this segment may gather momentum. Additing to this, the pipes used in Fire control systems is also poised to do well.

hii basu sir very good morning sir you put a detailed report on supreme can you explain sir the supreme industris can replace the DI pipes by producing opvc pipes ? actually sir in water infra there will be huge demand of DI pipes in coming years so my concern is that opvc pipe can replace the di pipes ( i read somewhere that govt wants to replace di pipe by opvc ) am i right sir if that will happen then what will be impact on electrosteel casting types of company ? thank you sir

There is limited use of CPVC pipes in large scale water solutions especially underground water transportation. Use of pipes is there in long distance transportation and also within local areas or buildings. Long distance is mostly done by DI pipes and local and building based by CPVC.

DI pipes will eventually be replaced by OPVC pipes. This was explicitly mentioned by Astral management in one of the concall Q&A. There’s no immediate threat though but it’s a very mid to long term story

Please refer to the response from Sandeep Engineer in the document link attached below: page9