Thanks for initiating this very interesting thread. One data point that is missing (but was covered in @Donald notes) is the management capability to turnaround overseas acquisitions. That has clearly come across as a major threat to the investment thesis. Suprajit acquired CTP Gills Cables in UK in 2006 when it was loss making, profitability came in 2011 when it was renamed as Suprajit Europe on 01-06-2011 (data taken from past annual reports). So management can turnaround businesses, sometimes it takes longer.

Another point was made about family succession. This is a very progressive management as they were talking about succession planning back in 2015 (see this 3-video series by SAP India). Now both sons are part of the business, one of them was recently inducted in the board (if I am not wrong). We now need to see how hungry the next generation is, any management interview planned? @Donald If you plan this, I will be happy to collaborate on management questions.

For me the key monitorables going forward are:

- Turnaround in the margins of WESCON and Phoenix Lamps

- Relevance of halogen lamps in the longer term, can management switch to LED lamps in the future?

- Electric vehicles have less than half the cable requirement. Adoption of 2-wheeler electric vehicles can be a huge problem for the company.

Valuations

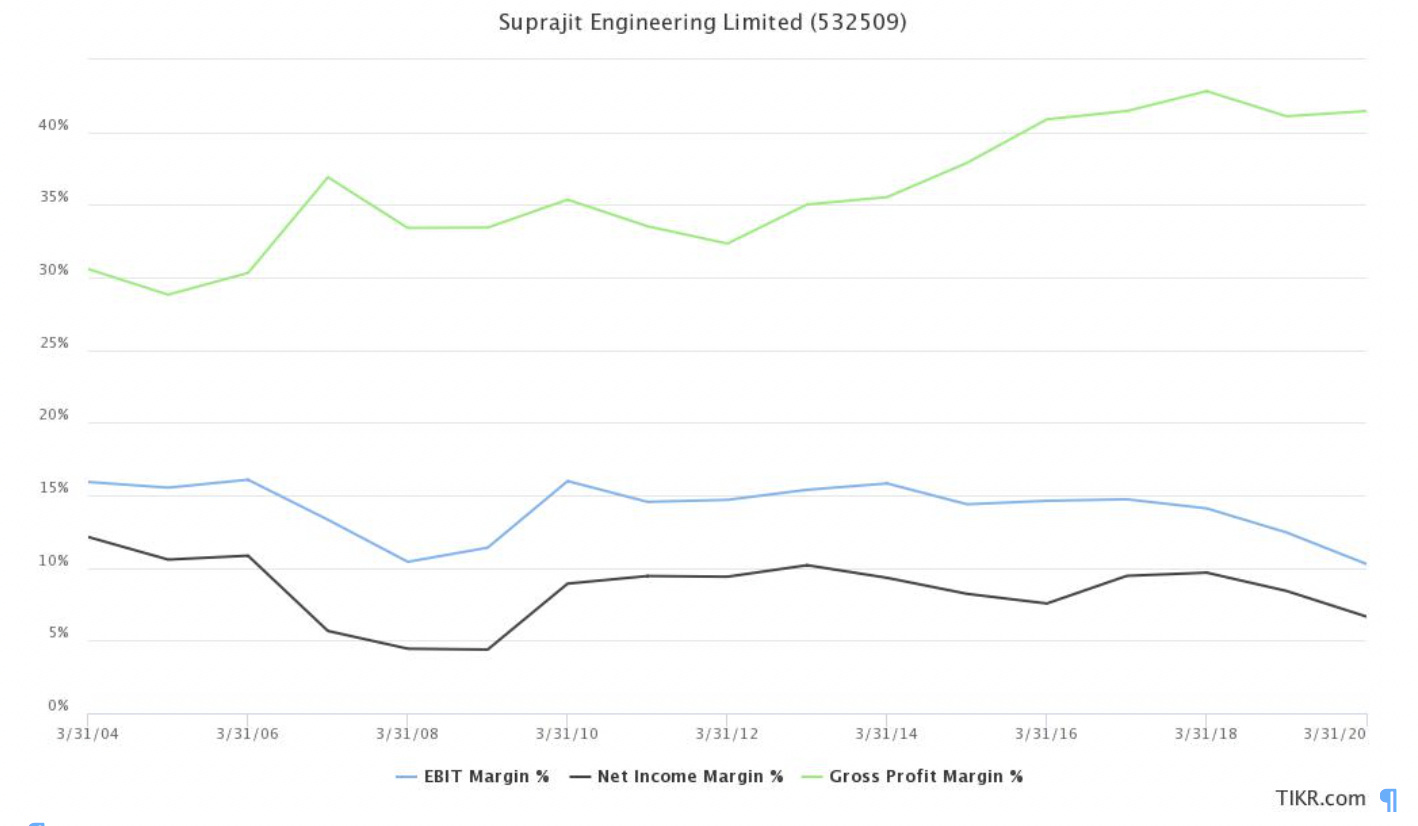

Valuations has not been covered and I will add that aspect. Over the long term, profit margins have varied from 5-10%, with 5% margins in very bad years (2008 industry downturn). The figure below (taken from tikr) shows their gross, operating and net margins from 2004. We can clearly cyclicality in margins.

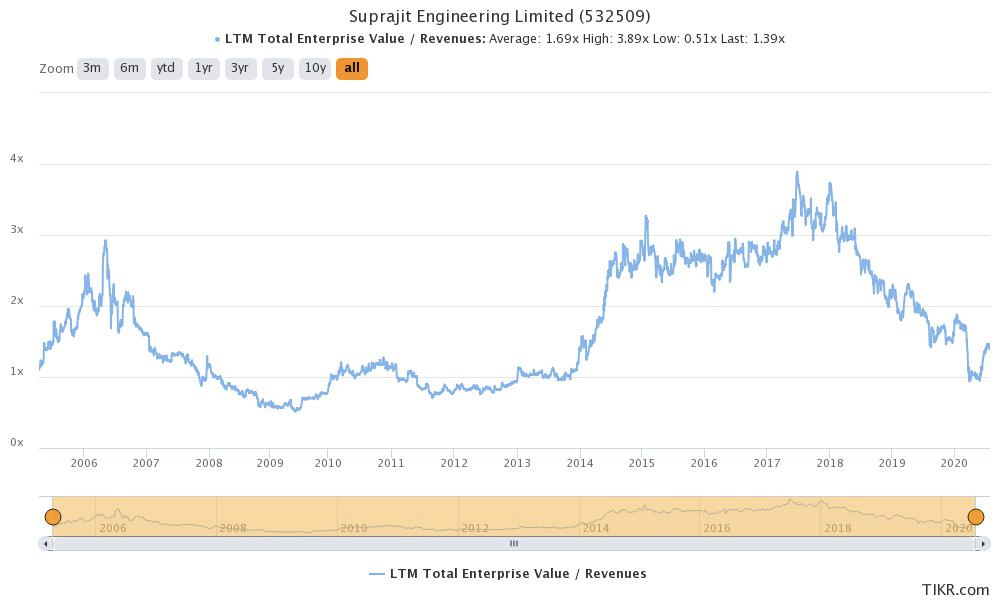

Cyclicality in margins mostly come from the embedded operating leverage in their business model, where in times of boom margins are high because of better capacity utilization and lower labor cost per unit of goods produced. Market generally values this kind of a business between 1-2.5 times EV/sales. A one time EV/sales implies a normalized P/E ~ 12 and a 3 times EV/sales is generally in times of boom where market extrapolates higher cyclical margins and trailing growth (when we should try to sell). Here is the proof (long term EV/sales for Suprajit taken from tikr)

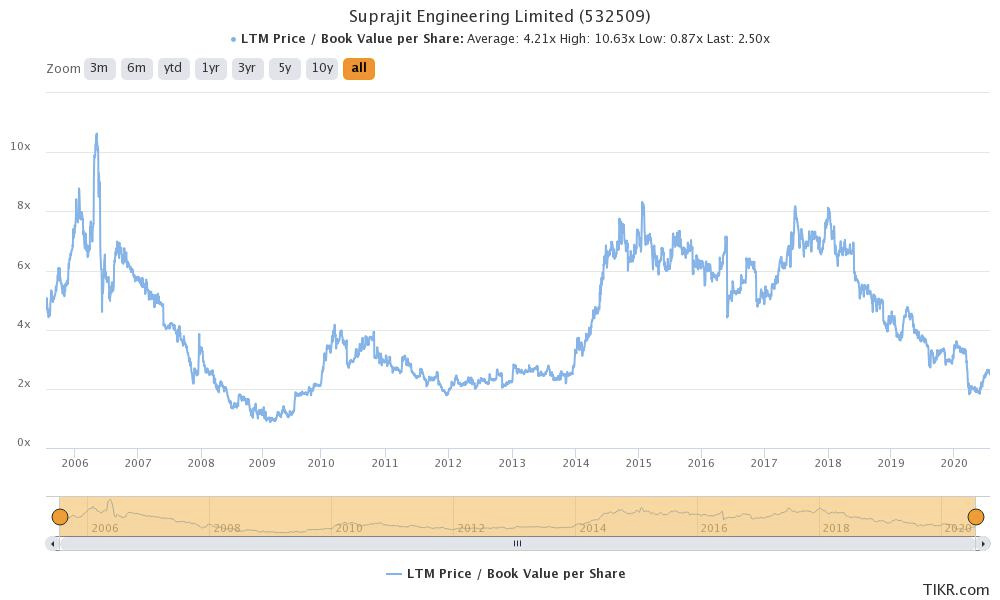

Other ratios (EV/EBIT, P/E and P/B is also shown below and taken from tikr)

Disclosure: No investments as on date (detailed portfolio here)