Superb Results by Sumit Woods Ltd in difficult environments. Improved sales, reduced Debt.

Two New Projects kick Started.

Co expected to perform much better going forward, two New Projects may start by March 2020 and may complete two Projects by March 2020 as well.

Expecting second half may be better than first half.

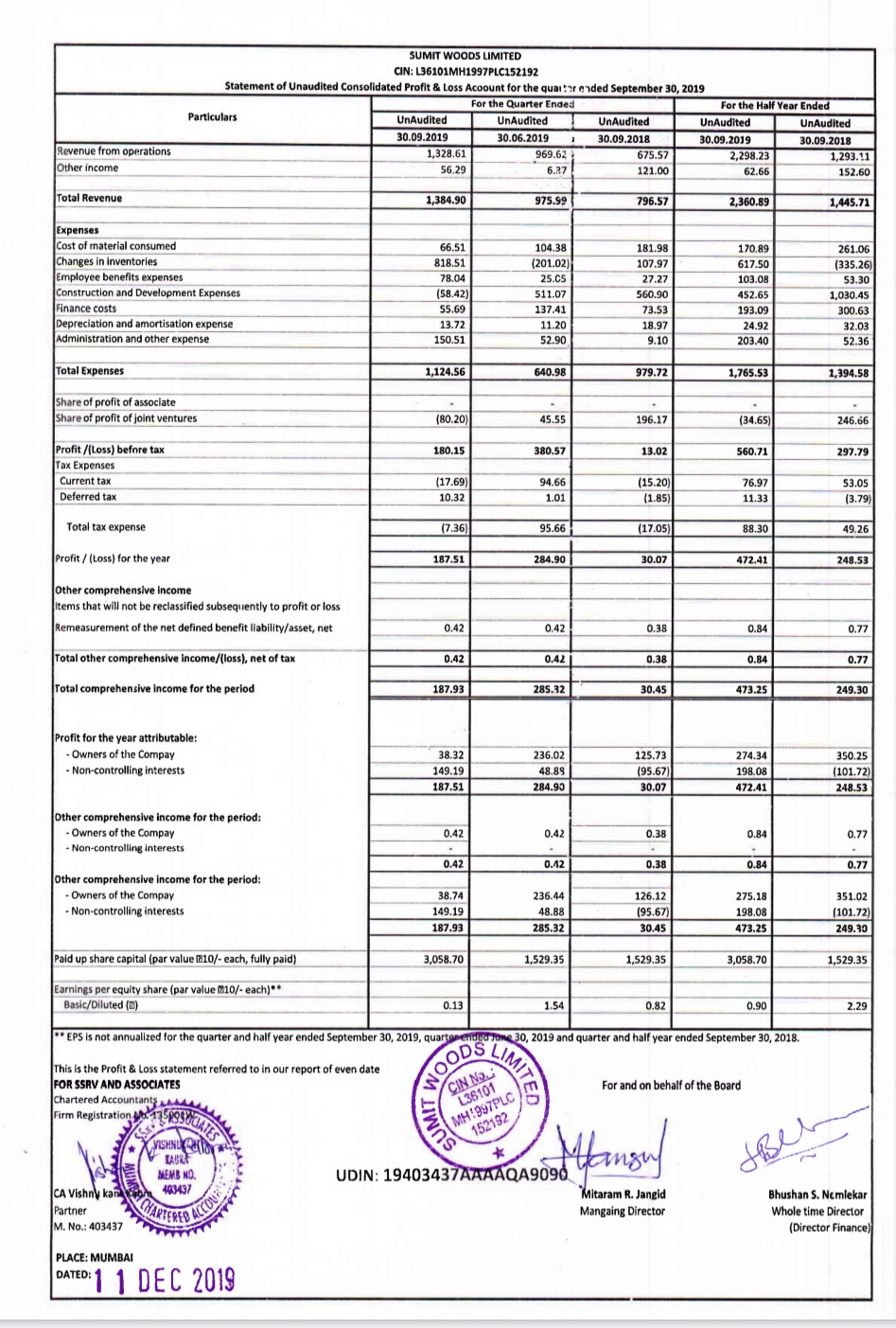

I wonder why you say it is superb. I find this is very bad result. PAT after minority interest is only 38 lac vs 1.26cr yoY. All the profits are going to non-controling interst (profit 1.49cr vs loss 96 lac yoy ). Net debt has gone up from 7cr (310319) to 32cr (300919) !! where did u see reduced debt? operating cashflows are negative at 3cr…

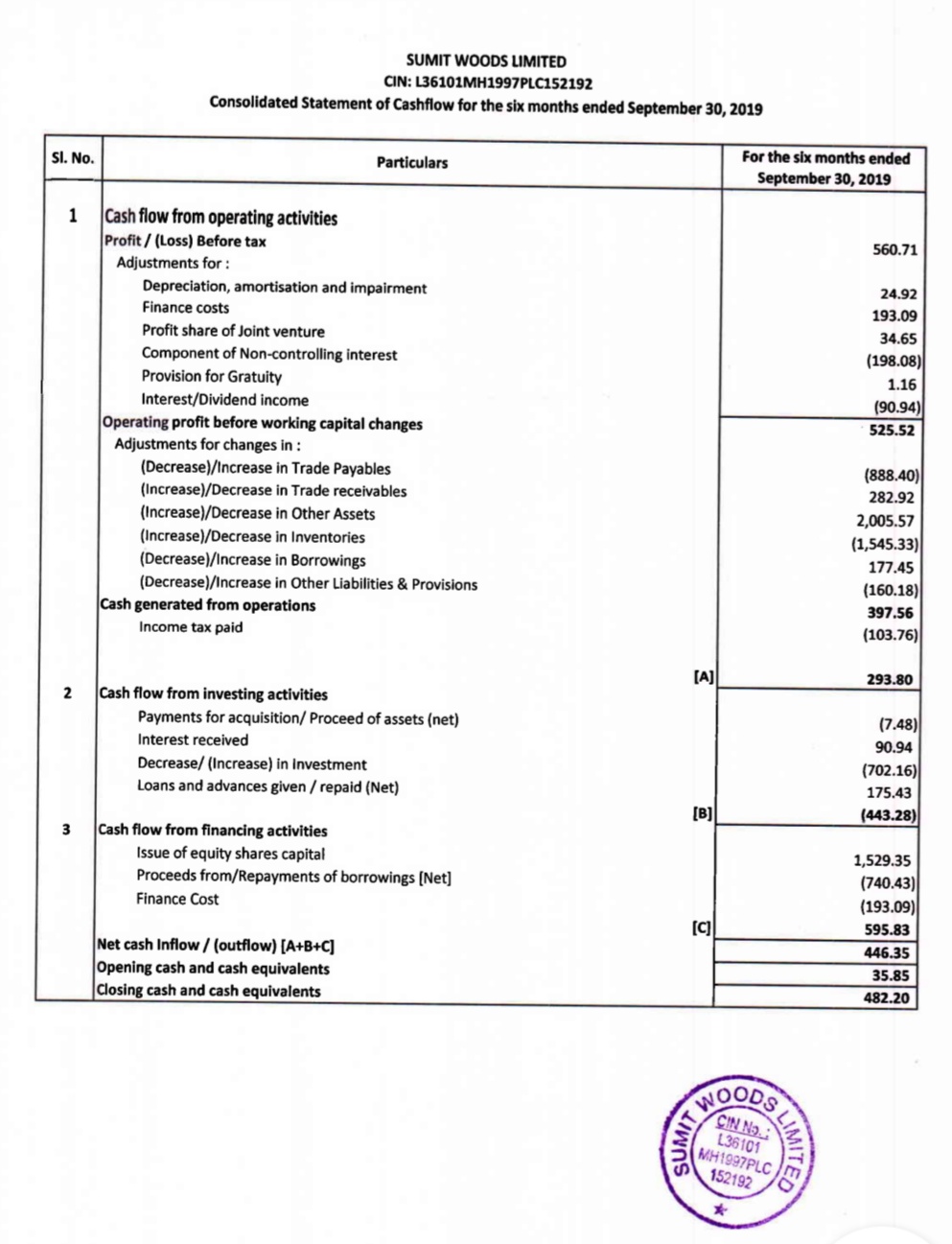

Operating Cash flow is 2.35 Crs, they included 530 lacs Loan repayment in Operating Cash Flow instead of Cash Flow from Financing Activities.

Co work in JV, Joint Development, Redevelopment and Development Management Model. For Most of past Projects Co had some JV Partners from last two Years Co taking up Projects in their controlling stake or fully, Currently just one or two Projects remaining in JV model that too completed & applied OC.

Even Co kick started their one of the biggest Project in Reported Qtr Net Debt Come down in both QoQ and YoY.

From here onwards size of Profit and Loss & Balance Sheet will improve significantly by March 2020 or June 2020, Being most of the running Projects and upcoming will have 50-100% Economic Interest.

After FY 2020, Sumit Woods Financials will become comparable to players like Ashiana Housing.

With current running and upcoming Projects I’m expecting around 150+ Crs sales in FY21 that can be 4X of current sales.

u posted consolidated b/s above but u r looking at standalone cashflow. In cons cashflow, there is increase in debt of 1.77cr. Hence, operating cashflow is actually negative 5cr.

If company has taken over JV projects fully in some projects, then its own profit should rise and not that of non-controlling interest. Herer it is reverse. And anyway, u have skipped this point in your reply.

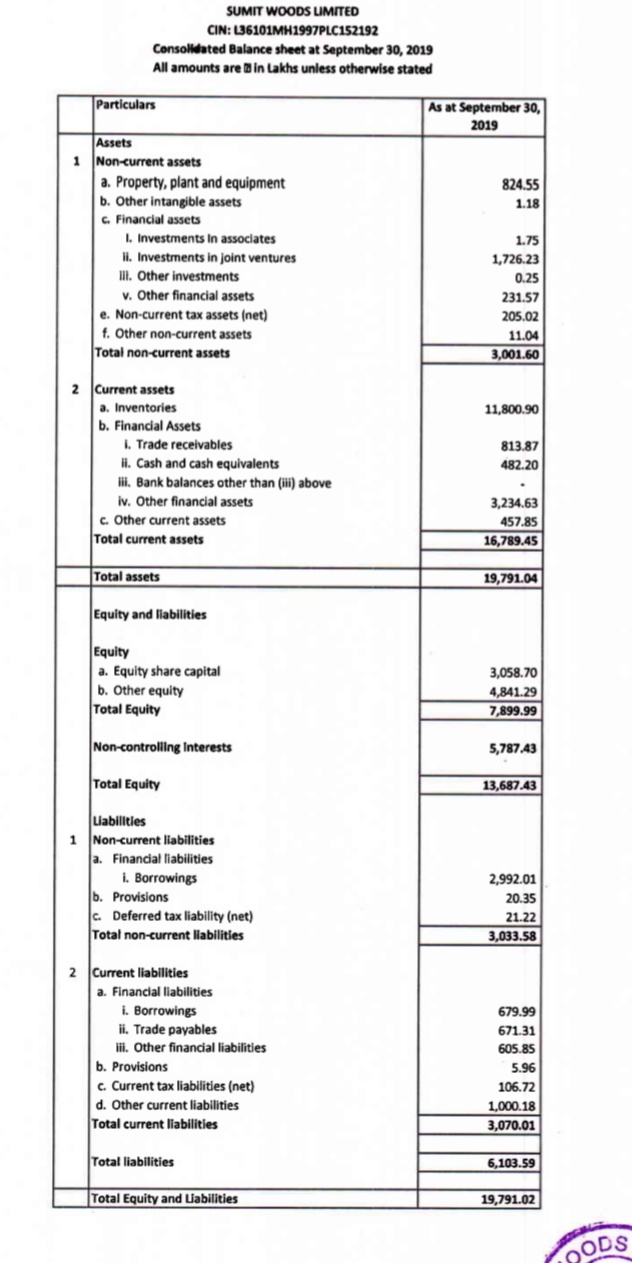

We have to see Consolidated figures only. Here putting you the Consolidated Cash flow

Operating Cash Flow is Positive by Rs. 294 Lacs

While in Cash Flow from Financing Activities also showing Repayment of Borrowings by 740 Lacs.

Co haven’t taken over any JV, I’m saying most of their JV Projects are Completed now, remaining two Projects will get OC by March 2020, one OC already applied.

Now all running or upcoming Projects are either fully owned, Majorly owned or DM (Fee Based) From March 2020 or June 2020 onwards Size of Operations and Balance Sheet will start looking Sizeable contrary to right now.

During the reported qtr it’s Credit Rating improved by two notch which is huge differential among Sector Players.

Co kick started a Project in reported qtr that have Revenue Potential of around 160-180 Crs in next 24-30 Months, Co aim to Complete the Project ahead of the Schedule.

Co’s debt Position is quite comfortable it’s Debt Equity Ratio is around 0.40 which is quite healthy.

What about this? – PAT after minority interest is only 38 lac vs 1.26cr yoY. All the profits are going to non-controling interst (profit 1.49cr vs loss 96 lac yoy ).

This Qtr they completed their Sion Project and applied OC, This Project is last big JV Project of the Co which they have minority Stakes and Major Nos came from this Project only and here Sumit hold just 30% equity Interest.

Got clarity from Management over phone

Some one time expenses

Around 30 lacs Migration Cost from NSE SME to Main Board.

Co switched lender from SBI to ICICI and reduced cost interest cost by 1.50% that took another cost of 30 odd lacs in the qtr.

In reported qtr Co launched two Projects, Co didn’t get any revenue in reported qtr but expenses booked as normal course of Business.

Hope these will help you to understand the results.

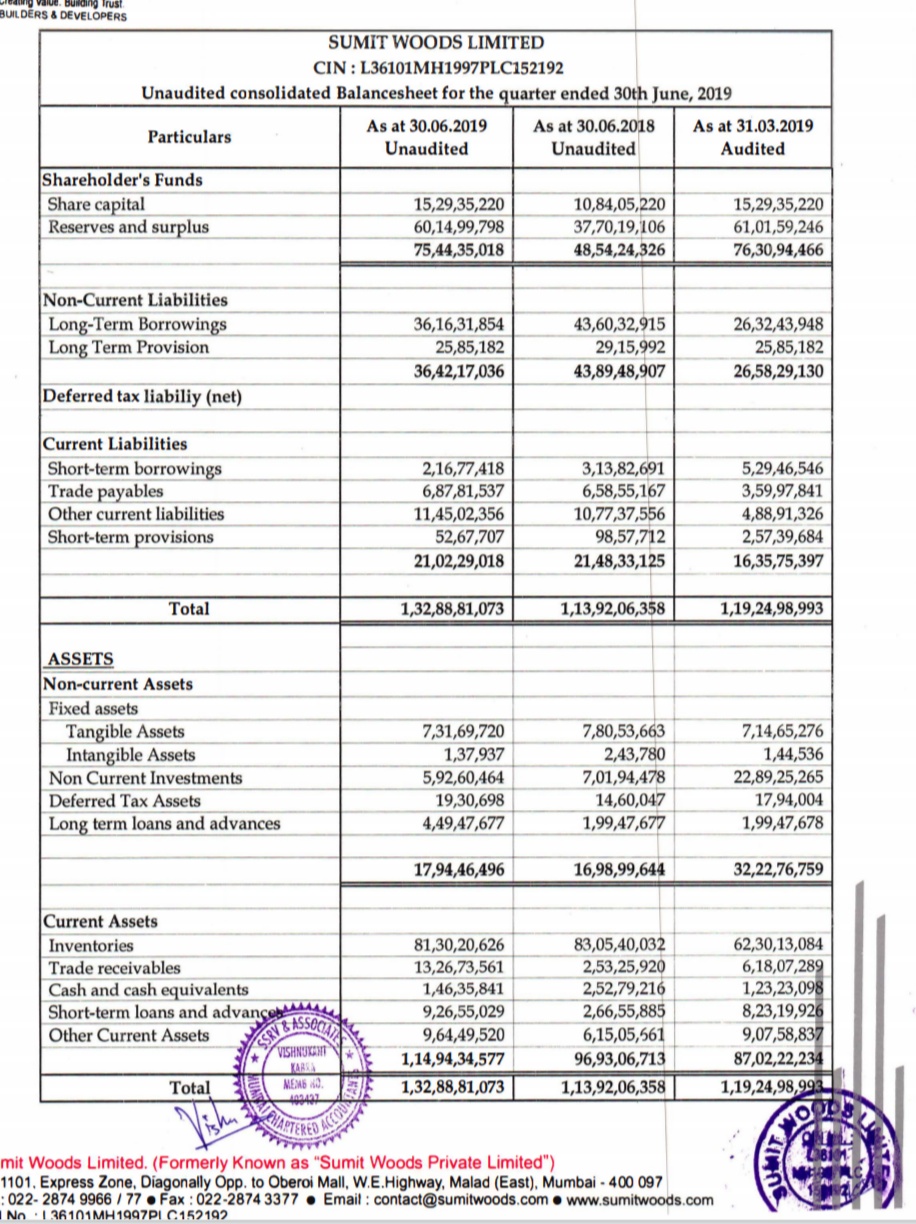

Share capital increased from Rs 10 Crs in Mar’18 to Rs 30 Crs in Sept’19. Almost 3x in 18 months.

Inventories increased from Rs 60 Crs in Mar’19 to Rs 113 Crs in Sept’19. Does it mean Project worth Rs 55 Crs got completed executed in last 6 months ?. Also the inventory number looks very huge for a company with a size of Rs 60 Crs market cap.

Dramatic increase in other assets of Rs 37 Crs in last 6 months

By September 2018 Co raised around 20 Crs through IPO & Pre IPO Placements that enhanced Capital to 15 Crs post that 1:1 Bonus in July 19 that took Issued equity to 30 Crs.

Co Launched two Projects during the qtr so some Increase may be due to that & some Incremental may be due to implementation of IND AS.

Other Assets may increased due to technical impact of IND AS.

Results improving gradually. Possibly it May start giving excellent Nos after March qtr as two Projects will start contributing to the Earnings.

From 2020-21 onwards things may change very significantly for the Co.

Sorry for the delay updates but it’s quite amazing that Co get OC for its Sion Project in Lockdown and also started construction activities for Goa Projects.

Hi Amit, hope you are holding the company, the company has received two orders recently worth 900 Crores and I think they will complete this order in the next 3-5 years with 16-17% EBITDA which will give them 140-150 Crores of EBITDA and PAT of almost 100 crores. Have you met the promoters? if yes whats their take?