Anyone with any detailed insight into this business? What can we expect the business to evolve into from here? What are the key opportunities and key risks?

1 Like

Hi, I was hoping to reach out to the management for a meeting. Does anyone know who is the right person to reach out to and could possibly share the contact details? Thanks

Hi Prakash, I was hoping to reach out to the management for a meeting, do you mind sharing the contact details? Also, who were the most helpful people you met? Thank you and please let me know.

Did anyone attemd AGM for Sukhjit? If there are any updates please post

The OPM is @7 % - the lowest in 12 years. Maybe could this be the bottom and the start of a new maize cycle? Also the food park should help in storage to maintain prices I guess.

Can anyone help in identifying the maize cycle?

Disc : Not invested. Invested in Guj Ambuja

I’ve done some research on corn cycle and below are my inputs:

On an average the corn cycle lasts for 28-30 years.

1. It starts with a build-up in prices due to growing demand and stagnant supplies

2. This is followed by a spike

3. Which triggers higher production

4. And then due to oversupply the prices crash and reach to a new base level

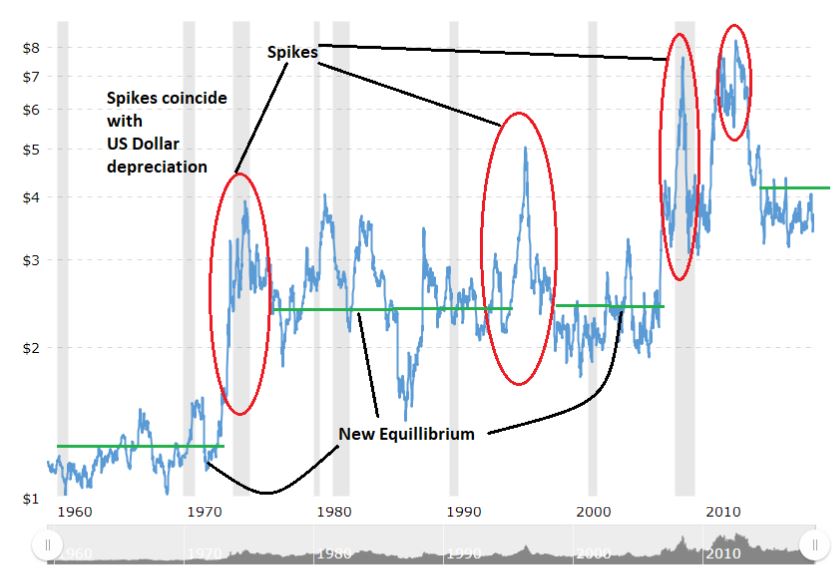

Below is the corn price chart.

1970

If we look at the last 50 years of corn cycle, one of the first spikes recorded occurred in 1970s.

There is no single reason for this spike.

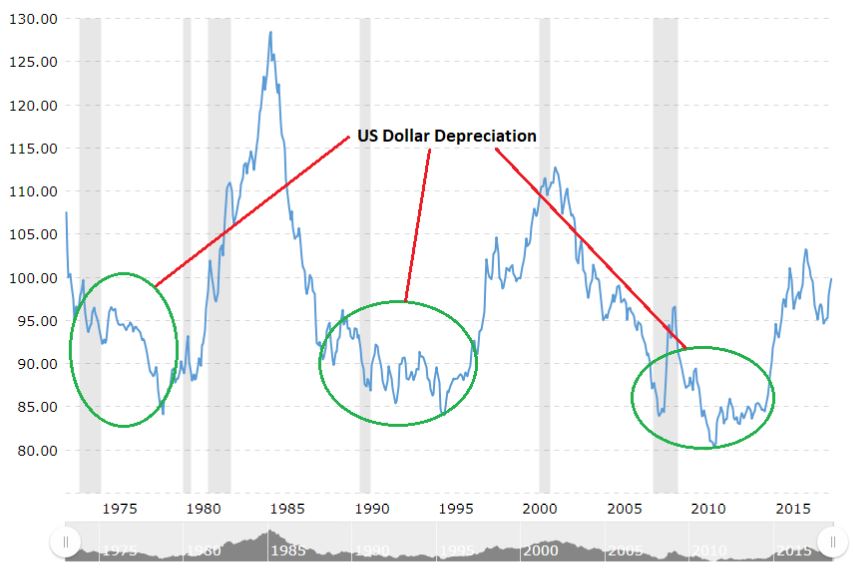

In 1971, the US, removed the dollar from the gold standard and moved to a floating exchange rate. This resulted in approx. 30% depreciation of USD against other currencies. The depreciation of dollar made U.S. products more competitive in overseas markets, so exports and prices rose.

Soviet Union unexpectedly purchased large amounts of grain from global markets fueling the increase in grain prices including corn to a 125 years high. The reason behind such a big purchase was a shortage of grains in Soviet Union. Because of this event other countries started buying grains too.

US Dollar Index

1990’s

The demand in mid-1990’s was due to the rapid development in Asian economies and declining production. This was again coincided with US Dollar depreciation.

2000’s

Once again the spikes in 2006-07 were due to the production shortfall and US dollar depreciation. Another reason was the production of ethanol which accounted 23% of total corn use in 2007-08.

So, as per my research we can’t predict when the corn price can spike but there are few characteristics using which we can find out that when do we have a high probability of increase in corn prices.

- Currency Depreciation of major corn exporting countries especially US.

- Shortfall in the stocks of major corn consuming countries.

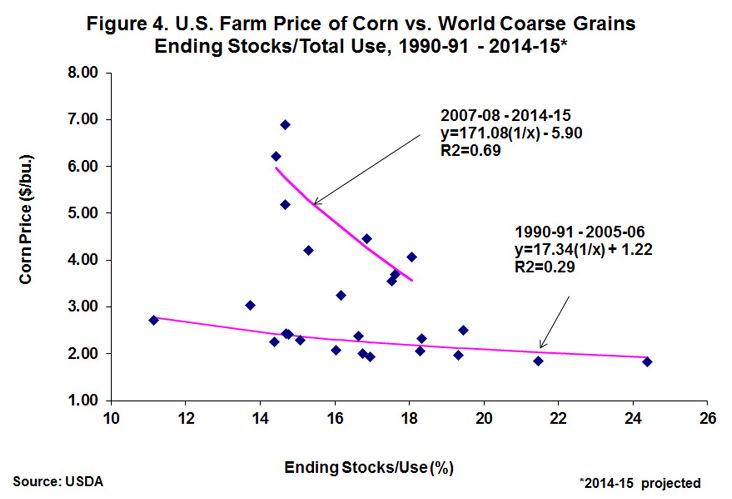

- Tracking stock-to-use ratio, this ratio is on an average inversely proportional to Corn Prices

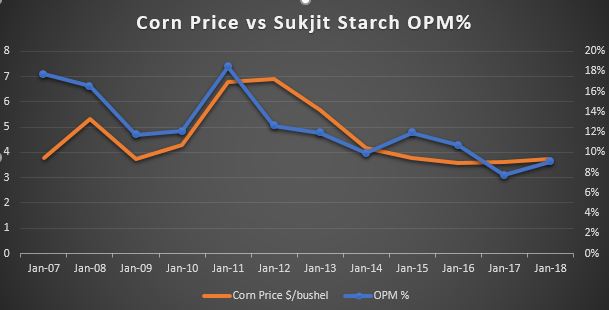

I can also see that Sukhjit Starch’s OPMs% are directly proportional to corn prices, though there is some lag. So probably the best time to play this stock would be when there is negative sentiment due to oversupply and stock-to-use ratio starts moving down, and USD depreciates.

Disclosure : Not Invested

7 Likes

Is it

- In latest annual report they are trying to explain more about covid 19 than the usual business of the company

Hi Team,

I have written a detailed blog about this company. Pleas feel free to read from the below link,

https://www.bsaravanan.co.in/blog/post/588205/why-sukhjit-starch-chemicals-ltd-is-undervalued

Thanks,

Saravanan

Twitter: 3peducator

1 Like

Very well written post @saravananb1994 , I became interested with this company after it popped up in my 52week high screen .What are your views on the performance of the company with respect to other listed companies in the starch industry like Anil Ltd, Gujarat Ambuja Exports, Tirupati Starch & Chemicals .etc

Hi Nitin,

First of all, kudos to your amazing research on corn prices and its effect on the stock prices.

Considering the current scenario of Russia Ukraine war, the prices of Corn have shot up in global markets, and the sanctions which will be imposed on Russia should also keep the prices high in the near future as per my understanding. Can you please provide some guidance on this about the near future improvements we can see in the topline because of this and if you like any other stock in the similar space? I am also thinking of adding GAEL which is also in the same space.

I started tracking this company 4 months back an invested at ~350 levels. I also managed to have an interaction with the management and someof the key points from my reseacrh and management are as follows:

- Growth going ahead: Sales are expected to continue showing upward trend in the coming years in 10-20% range (expecting on the higher side of the range)

- Full capacity utilization of the Mega Food Park may take 2 to 3 years but substantial part of bank’s finances have been paid off

- Total Capex on Mega Food Park is around 140 cr. The revenue of Mega Food Park will come from the leasing of its facilities and partly from sale of electricity & steam produced by its Co-Gen facility.

- The recent increase in margins has partly come by the increased scale due to operationalization of the largest maize processing facility Phagwara and partly from higher share of high value products

- Company will endeavor to maintain EBITA margin at around 14-15%

- End user industry- percentage of revenue has increased from Pharma, Healthcare and FMCG sector

- Spike in maize prices: company has sufficient experience of successfully handling such situations in the past

- Revenue from top five customers comprises about 15% of the total revenue.

- The capacity utilization varies from 80 to 90% except the new maize processing unit which is currently operating at around 75%

- Competitors: Sayaji Industries ltd., Universal Starch-Chem Allied ltd., Tirupati Starch Chemicals ltd., Gujarat Ambuja Exports Ltd., Gulshan Polyols Ltd.

- Exports: India enjoys good cost and quality advantage over other Nations for starch & Liquid Glucose etc.

- Imports: There is no Import of starch from China or US due to higher cost of production / transportation.

Disc: Invested.

7 Likes

Thanks for sharing this, Harsh. Did they say anything about their new Capex plans or getting into grain-based ethanol like their competitors?

They are clear about not getting into grain-based ethanol, I had asked them about it. They have enough capacity to grow at 12-15% (volume) in FY23, and will need capex post that.

4 Likes

Thank you for the details. My main concern currently is about their margins. The last time maize prices increased this way; their margins were significantly impacted.

1 Like

Agreed. We rely on management’s experience of decades. Next 2 qtrs will be litmus test of their capabilities.

The recent fund raise, first time ever it seems by the company, hints at another major expansion plan. Although, they issued share at steeep discount to market price.

Can someone please guide on the below points -

-

There was a post about the correlation of USD prices and Corn Prices and it’s impact on the Co.'s OPM. Can someone please take the liberty here and explain the same in a bit more detail so that this can be understood better

-

While stock has corrected ~30% from the ATH, its competitors - Universal Startch, Tirupati Starch are showing some strong support/uptrend. Does this mean Sukhjit is a bit overvalued as compared to its competitors.

Discl. On Watchlist. Not Invested yet.

1 Like

Commissions a hydrogen plant from biogas at Phagwara

Seems to be first in India!

Sukhjit Starch FY22 Annual Report Takeaways:

• Management comments:

o The Co. has shown resilience during tough times and have emerged as ‘Partner of Choice’ for many clients, especially in the value added product range.

o As a part of this Transformation Agenda, we have transformed our manufacturing process and logistics in last 2 years to achieve and to enter next phase of growth.

o We consistently use our expertise to migrate customers in our Tier 2 and 3 cities from unorganized sector to organise where people offer international quality at Indian Prices.

o Overall global environment is quite positive for exports from the starch industry as higher cost have helped starch producing countries to increase exports.

o The global geo-political situation is challenging and supply side constraints have caused unprecedented inflation. This remains a key risk as it would impact demand, and the response of Central banks to squeeze out liquidity could in turn further impact the demand.

• Operational performance:

o Actively managed the terms of our customer contracts, which enabled us to address higher corn and input cost, and deliver profitable growth.

o The New Unit in Punjab is operating at 80% capacity for starch & 85% plus capacity for derivatives. Co. will achive 100% in FY23.

o Company is seriously looking to expand capacities of maize processing at two locations where we are still working with old / low capacities.

o We firmly believe that we will be able to increase the capacity to 2000 TPD from 1600 TPD in the next two years.

o We are hopeful to exceed the expectations of our dear shareholders who have put faith in us over the years.

o Capex for FY22 was Rs. 26 cr and have approved plans of Rs. 35 cr in FY23 (Gross Block of Rs. 685 cr)

• MD&A:

o Global growth is projected to slow from an estimated 6.1 percent in 2021 to 3.6% in CY22 and 3.3% in CY23.

o Sustainable fuels (bio-fuel):

Globally, 13 per cent of corn production and 20 per cent of global sugar cane production go into ethanol production.

Price of these commodities have up sharply.

Growing food and energy security concerns are raising questions about the use of food crops for biofuel

o India:

A growing middle class, the emergence of new cities and increasing internet penetration make India’s consumption story one of the world’s most compelling.

The COVID-19 pandemic led to increased acceptance for processed food (KPMG 2021) especially in Tier II and III cities.

o Starch Industry:

Starch is considered as one of the most promising natural polymers because of its inherent biodegradability.

As per our internal study and the last few year trends we have observed, the starch industry will definitely grow at the rate of 15% to 20 % for the next 5 to 10 year.

The per capita consumption of starch is still below 2 kg average in India against the world average being above 6 kg with China at 10 kg.

Starch is still finding its use in many products & particularly shift from plastic to bio degradable

Textile, Food industry and the packaging offers ample opportunities.

o Sukhjit Starch:

The company enjoys preferred supplier status with many MNCs owing to its standard business practices and high quality products

To take advantage of this, the next Generation of the promoters has great ambitions to go for high value products.

Besides ramping up old capacities, their product portfolio will also be revamped to add high value products.

The main strategy of the management is to grow the production of value added products by at least 25% over next 3 financial years.

Our ownership structure provides us with the stability to invest in businesses that we believe in and to support the growth of those businesses over the long term.

Director’s remuneration:

(Rs. cr) FY20 FY21 FY22

Remuneration to Executive Directors 1.13 0.87 1.99

PBT 33 28 102

% of PBT 3.4% 3.2% 1.9%

Remuneration ton non-ex directors 0.20 0.29 0.60

• Accounting:

o Co. has extended Rs. 51.9 cr to its subsidiary Sukhjit Mega Food Park without specifying any terms or period of repayment. The said will be recoverable from the balance amount of grant receivable from Ministry of Food Processing and leasing of the facility to the tune of Rs. 50 cr a year. (Invested Rs. 140 cr in the facility.)

o Sukhjit Mega Food Park & Infra Ltd generated revenue of Rs. 22 cr in FY22 and cash accruals of Rs. 5 cr. This is expected to improve significantly going ahead.

o Provision for bad debts was Rs. 2.8 cr (0.2% of revenue)

o Revenue Break up:

Revenue break up Rs. Cr % Mix

FY20 FY21 FY22 FY20 FY21 FY23

Starch 298.5 231.5 432.4 37% 33% 37%

Starch Derivatives 298.4 277.7 391.2 37% 40% 34%

By Products 202.3 189.6 335.4 25% 27% 29%

Total Revenue 799.2 698.8 1159.0 100% 100% 100%

o Highest increase in expense was in freight which jumped from Rs. 18.2 cr (2.6% of revenue ) to Rs. 30.4 cr (2.7% of sales)

2 Likes

Hello everyone, I know this is coming in a little late but I had attended the AGM 2022. Sharing some notes from my visit. I got a chance to interact with the promoters as well. Disc: Tracking Position (no transactions in the last 30 days).

Background of the company-

- The founders had realised early that sugar and carbs in a growing country will always be required. They saw that carbs were playing an important role in food, textile, and pharma sector in the West. India being a protein deficient country, they foresaw that carbs and starch would keep growing to make up for that deficit.

- They were situated in Punjab which is a maize growing belt. The founders pioneered the machines to go from 5 TPD to 30 TPD. Maize is the best route to produce starch as compared to Potato or Tapioca as both are unviable and expensive methods.

- They started adding more products to the portfolio starting 1960s. They claim that they were among the first ones to manufacture Sorbitol and Dextrose indigenously in India using indigenous technology

- Between 1987-2000, the company went through consolidation and did some de-bottlenecking. They also tried their hands at NBFC & Textile businesses but they did not work out. In 2000s, the company and promoters took a decision to focus and grow only in the Starch business. This is when they set up the Malda and Himachal Pradesh plant.

- In 2014, they realised that they needed to modernise the Phagwara unit and expand capacity. The old unit was right in the middle of the city and it was difficult to expand. That is when the Food Park happened (more on this later).

- Company was established by 2 brothers- Mr. K.K Sardana & Mr. I.K Sardana. Mr. I.K Sardana passed away in 2019 (his wife is the Chairman). Both the brothers have 2 sons each.

- All the 4 brothers in the second generation are completely involved in the listed entity and each look after respective units. Shareholding is also equally split among the 4 brothers. Mr. Bhavdeep Sardana looks after new projects and business development along with the new Phagwara unit. I got a chance to interact with him.

- Mr. Bhavdeep mentioned that because the company has been listed for a very long time, they have been transparent and this has kept the family and business together all this while.

- They have no other businesses outside of Sukhjit Starch.

Food Park-

- What happened in the form of approvals in 2017, should have happened in 2015. They mentioned that it was a very difficult period as the old plant was running at full capacity. The food park was developed and the new unit finally started in Oct’20. They were behind by 2-2.5 years

- The older Phagwara unit was 150 TPD. The new unit at the Food Park has an installed capacity of 600 TPD which can be expanded up to 700 TPD.

- Why food park and why did they spend 105cr?

- This is a 55 acres land. 26 acres is developed area. Remaining 29 acres is for greenbelt, roads, and utillities like Common ETP and Power Generation unit of 6.5 MW which is being utiised by Sukhjit’s new plant currently.

- Out of the 26 acres developed area, 14 acres is for Sukjhit’s new unit. The initial idea was to give the remaining land to their existing customers and supply them with starch and other value-added products directly through a pipeline but covid ruined their plans.

- So, out of the 105cr invested in Food Park and its infra like ETP, Power Plant, etc, it greatly benefits Sukhjit’s new unit and will benefit other manufacturers who put up the plant there. They have invested another 160cr to set up the new facility. So, the 600 TPD capacity was set up at the cost of 260cr even if we include the entire Food Park capex. For reference, Gujarat Ambuja had announced a capex of 450-500cr for a 1000 TPD capacity at Sitarganj in Jan’22.

- So, essentially only around 30-35cr has been spent on non-core operations but that also they feel will be recovered from the core operations itself by supplying starch and its derivates to the customers when they put up a facility at the Food Park.

- This was the first time they set up such a big plant along with power generation. They now know how to operate bigger plants and this will greatly benefit them in the future.

Overall Operations-

- They have land available at all the units. Current capacity is at 1600 TPD and they will gradually expand to 2000 TPD (as mentioned in the annual report). They have enough land to expand to 3000 TPD. They will start own power generation as well in other units.

- The major margin difference between GAEL and Sukhjit’s margins profile is because of much larger plants of GAEL (more efficient) and captive power generation. The company feels that once they expand at other locations and start generating own power, their margins should inch upwards.

- From 1 MT of maize, 0.65 MT of starch is procured. It is then on the company how they want to utilise this starch. They have dedicated plants at all the units for different products. When I inquired about the installed capacity of major products, Mr. Bhavdeep mentioned that this is not revealed by anyone in the industry and they would like to keep it that way.

- On Value-Added Products- His straightforward reply was that what is VAP in one year may not be VAP another year. VAP is defined by margins and not just by products. He ensured that Sukhjit has the right basket of products and will focus on products that have higher margins during a particular period.

- Main plants are Anhydrous, Dextrose, and Sorbitol. Products that go into pharma are automatically higher grade.

- The company has dealer distributors in place and also does direct supplies to large customers. There is not much of a margin difference.

- Company is working on new product development and that would their focus in FY23 & FY24. Growth should come from here and capacity going from 1600 MT to 2000 MT.

- They track plant wise profitability and take feedback on different units to make the overall operations more efficient.

Industry-

- The top 3 players are Roquette, GAEL, and Sukhjit. Roquette is the leader in terms of quality and GAEL in terms of capacity.

- Mr. Bhavdeep mentioned that after Roquette entered India, the industry has become highly organised and they have streamlined a lot of things which did not exist earlier like cash and carry sales, quality products, conducting business ethically, etc.

- The 3 large players are vendors with most of the large customers.

- On smaller listed players like Tirupati Starch & Universal Starch- they have been able to expand capacities and grow in India because the starch industry is growing at 1.5x of GDP in India. It has wide uses in paper, textile, and food industries among others. Growth of exports in these industries also help with rise in demand for Starch.

- He also mentioned that smaller players are inefficient (seen in their margins) and don’t have a high share from VAP segment.

- Chinese presence- China exports starch derivatives, but is a net importer. They export very few products to India. These are niche and small volume products

- They don’t want to enter small volume products and Chinese have the tendency to kill the competition. They want to go into larger volume products and be in the Top 3 in India.

- He was all praise for Manish Gupta (GAEL’s promoter) and did not shy away from saying that he has set very high standards and has taught the industry how to do business profitably.

Miscellaneous-

- NSE listing would be done soon

- They were looking for buyers of their old unit land. They have already announced about this publically. It is a 10 acre prime property right in the middle of Phagwara.

- Excise 29cr contingent liabilities- Confident that it will be in their favour

- Better investor communication- they will definitely consider an online AGM next time.

I feel that the company is conservative and has the right approach towards this industry. Overall, starch industry should grow and they have enough land to almost double their capacity. As capacity goes up and they become more efficient, margins can go up as well. A key monitorable will be how they utilise the sales proceeds from the sale of Phagwara land.

Disc: Tracking Position (no transactions in the last 30 days).

12 Likes