Quant elss vs parag elss.

Quant is doing far better.

Good to compare but the style of investment varies for both fund houses.ppaf is all of value investing and on other hand quant is of like momentum backed by statistics of data. Need to decide what kind of investment suits you and align with fund house to generate wealth

Hi, kindly share which website you used for comparing and identifyingdifferent funds overlap

The link is in the posted image.

You can go to Coin (zerodha) or trendlyne.

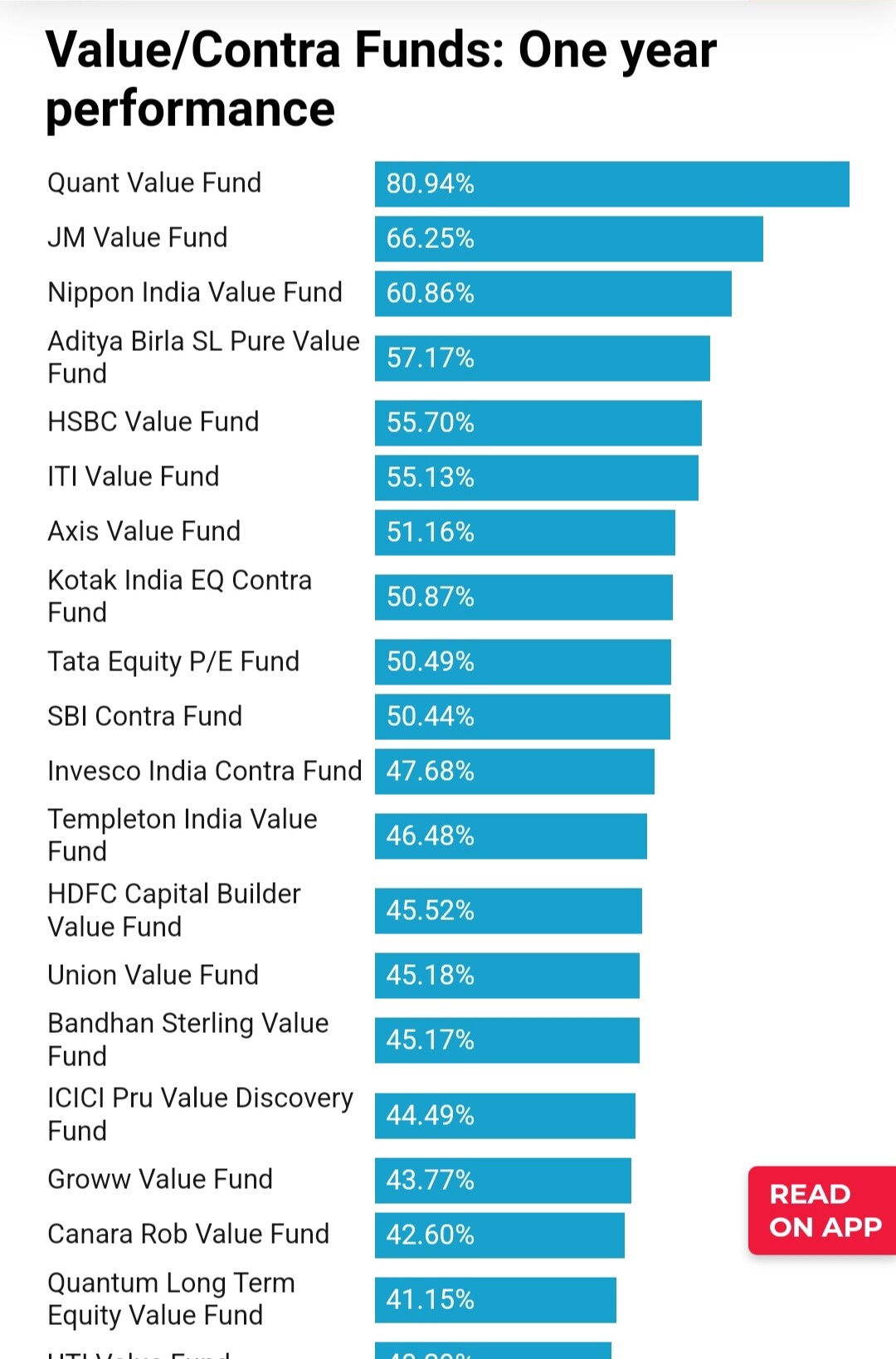

Quant Small Cap Fund, the topper in the category, gave 14.21% return on lumpsum investments in 2024 so far!

In my opinion, SBI Bluechip, UTI Nifty 50 Index Fund being large cap oriented will give stability to your portfolio.

Parag Parikh Flexicap will give exposure to Developed markets. It would take care of rupee depreciation and can give good returns as INR depreciation will continue for many years.

ICICI Nifty Next 50 Index Fund may test your patience as returns may not be encouraging and Volatility will be as close to Midcap Fund. You can read review by Pattu Sir on freefincal website.

Nippon India Nifty Smallcap 250 Ind : Here your risk appetite will be truely tested. There will be huge ups and downs, so only suitable for goals which are 15 years away.

Motilal S&P 500 Index Fund : This fund will also give US exposure. With Parag Parikh Flexicap, you already have reasonable exposure to US Tech stocks, so this fund can continue till you believe it is adding value to the portfolio.

I would say, based on my experience, all Funds have good times and bad times.

Mostly the underperforming funds often catchup after few years, and Top performing funds sometimes become laggard. This cycle keep repeating after every 4-5 years, so in the long run, you should focus more on funds with good management, low expense ratio, low standard deviation (low volatility) compared to peers instead of chasing returns. This is more than sufficient.

Also you should focus more on your goals and do regular Equity: Debt balancing as your goals approach nearer.

Rest all is noise and it is less important. Once good funds are selected, stay invested until you really believe that your fund selection was wrong. That’s the key.

3 Likes

Quant mid cap is also doing as good as it’s small cap.

It the top fund in mid cap catagory.

It s 3 months return is 15 percent while 2nd best mid cap return is 11 percent.

1 Like

1 Like

Hi everyone,

I’m 21 and have been investing in mutual funds and stocks for the past 4-5 years. Over time, I’ve built a reasonably concentrated MF portfolio, currently around 4 to 5 funds, in line with the general advice that over-diversification can dilute returns.

However, once in a while I come across a new mutual fund that I believe has strong potential (due to a differentiated strategy, a change in fund management, or unique positioning). My dilemma is:

How should one go about adding a new fund for SIP without bloating the portfolio with too many holdings?

Do you:

Exit or trim an existing fund to make space?

Or just decrease SIP amount in other funds and add that amount to the new one?

Would like to hear how fellow investors think about this. I was thinking of selling an old fund and buying this but that would mean a lumpsum investment which I’m not sure if it’s a good idea at current valuations.

Thanks in advance!

Every few years, the same pattern repeats: a new mutual fund starts outperforming the index, climbs the rankings, attracts a surge of investors, its AUM balloons, and by the time you invest, it begins to underperform. On top of that, each time you exit a fund, you pay taxes.

So, what’s the solution?

- Let go of FOMO. Over the long term, only about 20% (or maybe 10%) of mutual funds consistently beat the index. Don’t stress too much about chasing performance.

- Hybrid approach. If you’re an active investor, consider allocating 100% of your portfolio to index ETFs. Then, each year, identify just 1–2 high-potential stocks that could deliver 50% returns over 1-2 years. Sell 5% of your ETF holdings to invest in these companies. This way, you stay diversified, minimise taxes, and still have a realistic chance of outperforming 90% of mutual funds, without the stress.

2 Likes

Since you are 21 Years old, you have lot of time to invest for your long term goals.

I would suggest you to add New Fund through SIP, if it helps you in achieving your long term goals, only if it is not in same category of current MF.

If you already have, Say, Mid Cap Fund, there is not much value addition by adding another New Mid cap fund. After few years, that New Fund mostly can under perform index or your current fund.

You should add New Fund only if it is really essential for achieving your goals.

It is always better to align Equity MF to your future goals, so that, you know how much years you have to achieve that goals and then decide the most suitable MF for that goal.

From my experience, if the goals are not identified then just adding New Funds may not help you to achieve much. You will see your Equity portfolio rising but without knowing the End Goal.

I may be wrong in my approach, but it has helped me to align MF with well defined goal and then select the fund and stick to it for minimum 5-7 years and if possible much beyond that.

I am not much worried about chasing performance neither I have any Index Fund. Index / ETF does not protect the downside and it is important in the long term. Returns are always in the hindsight and Risk is in the journey. Off course, having one or two Index Funds/ETF(s) is also a good idea.

3 Likes

Thanks for your valuable advise @avneesh and @gsapte

I’ll look into goal based investing more and also the hybrid approach is something I’ll surely try and implement, it sounds interesting.

Nice strategy!

Need to ask here. You mean to sell all existing old MF and invest in ETF? In the meantime search for good stocks ?

Selling all your existing MF units can be a personal decision, considering your taxes.

In my case, I have stopped deploying fresh money in MF. I am only buying index ETFs. Meanwhile, I am also looking for good stocks with high chances of outperforming the market. Hopefully, this strategy should work.

1 Like

Your portfolio is very good if you prioritize lower costs, market efficiency, and guaranteed market returns over the long term, without relying on manager expertise.

Many stories are being floated now-a-days which suggest that, investing in Index ETF/Index MF is better than active funds. All such suggestions will come and disappear after few years!!

Investors keep looking for new themes and ideas after every 3-5 years and such new strategies will come and go!!

What actually works is select active or passive funds with Low Cost, Good governance and remain invested for very long term and the magic happens!! Rest all is noise.

In past few years, Index may not have given much CAGR but some Active Funds might have beaten Index and Over next few years it could be opposite. An investor should not read too much into this as long as he/she is achieving his/her Financial Goals.

2 Likes

Some times Active Funds if hold for longer periods can beat Passive Funds / Index Funds.

Changing funds after 2-3 years of down turn is the main reason why MF investors do not see the benefits of Active Funds. One benefit is it might protect the down side to a certain extent.

ICICI PRU Blue chip Fund / Large Cap Fund is one such fund which has given stable returns in tough market conditions in the past 4-5 years.

Disclosure : I am holding this fund since 2015 on wards. SIP & Lump sum investment for first 4-5 Years and Now holding/partially selling for few financial goals. This is one of the funds I happen to continue holding in spite of occasional under performance.

1 Like