with increase in ethanol price likely to be announced as crude has reached USD and exchange rate crossed 86 ethanol can go up by Rs. 5 per litre. ethanol will also save forex.

also increase in MSP for sugar expected shortly. sugar sector should bounce back from here.

1 Like

UP may increase SAP and the yields are expected to be less. It is going to be volatile for some ore time. Disclosre: invested in sgar stocks. Views Biased

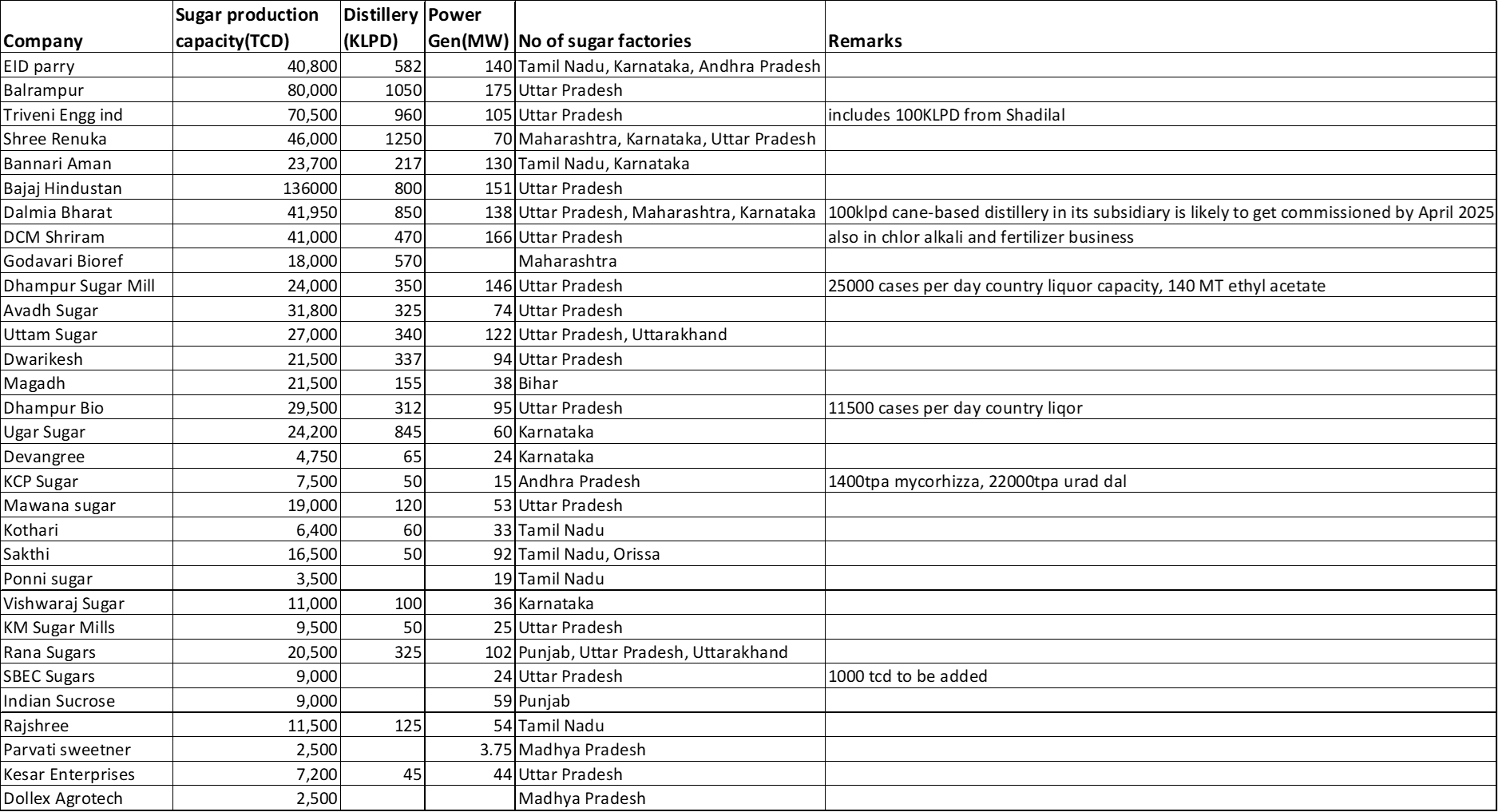

Just some raw data, which could be of some use.

Read “number of sugar factories” column as “place of operation”

10 Likes

sugar companies should stop supplying ethanol… at these prices it is better to make sugar…

in fact sugar prices will go up 5 to 10%.

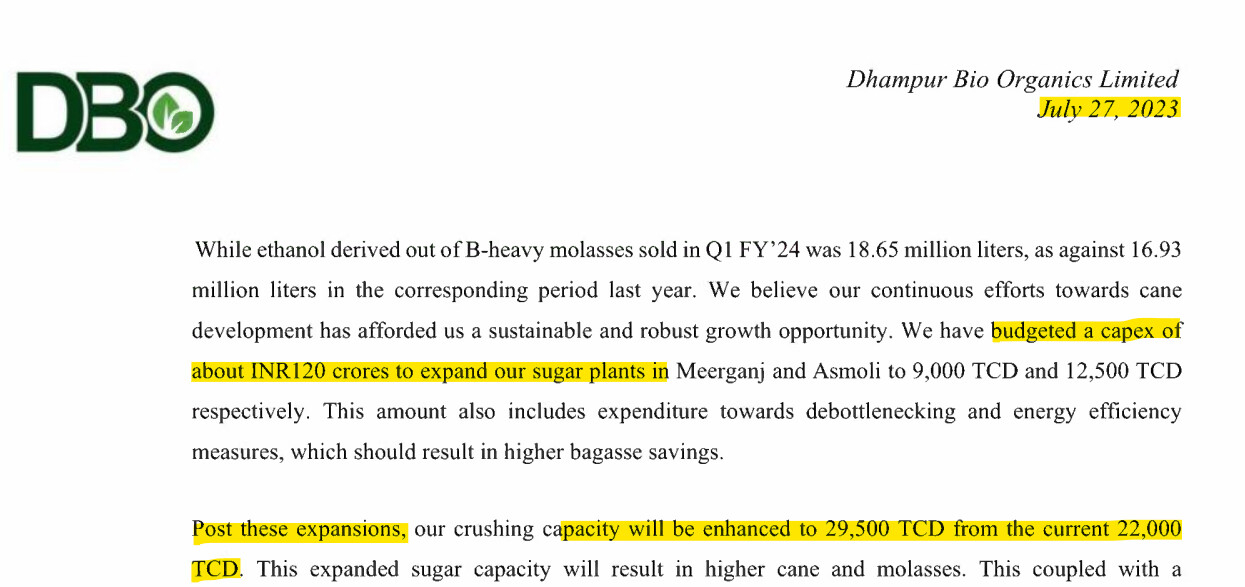

Did you conclude on this? Below suggests ~16Cr. per 1000 TCD when Land is already in place:

~20 Cr. per 1000TCD. Refer Page-36:

https://environmentclearance.nic.in/DownloadPfdFile.aspx?FileName=i8v/vaxDffNRSoYzTiHIvH+4TrHJKqCHErh/DZas2jtovz8xVY9ynHqdvsiDtXk2fVL0k1+1/Wy3vDLzRnY6FQ==&FilePath=93ZZBm8LWEXfg+HAlQix2fE2t8z/pgnoBhDlYdZCxzWF1OLE6RXe5MiAhSH8vdQ1

~21 Cr. per 1000TCD. Refer Page-19:

https://environmentclearance.nic.in/DownloadPfdFile.aspx?FileName=GmgdVCs2yw/3MPMslEO0YoJBCtQbaiM1BjWzpDiYoRg5wJau877vghyaESZsMF0I3HMo48fJhh4FgZXeA2LH08QrqwCK51cUGDwf56h8Vhs=&FilePath=93ZZBm8LWEXfg+HAlQix2fE2t8z/pgnoBhDlYdZCxzUlDadBGu7t8v4JoQvNU6UBlSmL0YQ7WQYaxkvlQvexKQ==

1 Like

When the ethanol procurement price is more than 1.6 times the price of sugar, it makes economic sense for sugar mills to maximize ethanol production. This was nicely explained by Mr. Narendra Murkumbi, Ex-Co founder of Shri Renuka Sugars in one of the Youtube channels. The current ethanol procurement price is Rs.65.61 and hence till the sugar price reach Rs. 41 it is more beneficial to rpoduce ethanol. The link to the channel is https://www.youtube.com/watch?v=UMjHWi5uaUY. Disclosure: Invested in sugar stocks. Views Biased

3 Likes

Mill prices in UP have reached 40/kg. so it is almost reaching parity. but will they be allowed to supply less than quantity contracted? first govt cuts the ethanol allotment of private sugar mills - now they could be forced to increase beyond contracted quantity.

it is always lose-lose for private mills… thats why i have always been saying that any mill expanding any capacity you should exit.

only those mills focuing on sugar recovery and mill efficiency are worth investing… and those getting into new products ENA/ IMFL/ CL / Chemicals/ Bio plastics.

4 Likes

Correct recovery and Production are concern

1 Like

Expectations of investors in sugar industry a. lifting ban on diversion of sugar cane juice and b heavy to Ethanol b. Lifting of ban on exports c. Revision of MSP for sugar d. Revision of Ethanol prices. Now ban on diversion is lifted. Export ban partly lifted, but who will get what quota to export is not clear. Other two expectaions may be the trigger for rerating. But when it will happen is anybodys guess. Disclosure: invested in sugar stocks. Views biased.

1 Like

at current international prices exports doesnt make sense… marginally above domestic prices.

1 Like

Any idea about eligibility for export subsidy?

@Aarti

Hi Mam,

Your views please about the future of the Indian sugar industry.

Disc: holding Dbol and Eid parry.

10 percent of my portfolio.

sugar industry has great potential for sugar, ethanol and bio-chemicals but the Govt. will not let it develop. Indian sugar industry will never become like that of Brazil…

As sugar recovery has come down in UP, sugar price has gone up - but still not enough to make up for increase in costs… it is going to be bad year for sugar stocks… without excess capacity shutting and some M&A happening this sector will not revive.

5 Likes

Hello, I’m looking to understand the sugar industry from scratch. I would highly appreciate it if someone could share some resources or reports that I can go through to understand it in depth.

Thank you!

Any views on valuation parameters to focus upon while valuing names in the Sugar industry?

is bajaj hindustan sugar stock undervalued currently at 18rs.

what is future looking like for this company, ethanol is not changing many things for this industry.

1 Like

I have been reading sugar cycle since last few weeks and would agree that there are so many variables that even an expert investor can commit mistake in execution. Having said that, I don’t think that this industry should be untouchable if you understand sugar dynamics. In fact what is hated/ignored in investment community becomes extremely attractive, provided you understand it well.

With this background, I am writing down positives and negatives of this industry and basis that , we can plan to invest when we think that risk reward is in our favor:

Positives:

- Govt policy shift is clearly visible based on its actions during last 7 years:

a) Govt fixed MSP (Rs 31) for Sugar which was never done in the past. Its another matter that price was never revised since inception.

b) Govt policy to divert cane to ethanol is continued with remunerative prices , and this also helped sugar industry in firming up sugar prices. This policy may mean that MSP on sugar may never be required, if diversion to ethanol keeps sugar demand and supply in balance. - Irrespective of Govt extreme control on sugar industry, Govt cannot allow the industry to die. That’s because 4 Cr vote bank (Cane farmers) matters the most to Govt, and they can be paid only when Sugar companies break even. Govt can decide exorbitant FRP/SAP, but also knows that sugar companies have to pay it and thus, govt need to create avenues for sugar companies to be profitable.

- Strong balance sheet - Govt policy direction (Ethanol etc.) has helped sugar players well and there balance sheets are much stronger today than where it was a decade back.

- Huge Operating leverage - Every single rupee increase in price of sugar above breakeven, adds directly to the bottom line. You dont know when this may play out, but when it does, it will have disproportionate impact on the bottom line. I single year of profitability can wipe out losses of last 10 years. As a investor, you may like to get exposure to such favorable outcome, when risk reward is in your favor.

- UP Story -

a) With development of C0238 seed, UP cane yield as well as sugar output both have increased substantially. For UP sugar mills this has been extremely positive, as there existing assets are now producing double the output without any additional cost.

b) UP farms are irrigated with abundant river water supply, where as Maharashtra cane farming is rain water based based and hence prone to weather uncertainties. - Cane based ethanol vs Grain based ethanol - Sugarcane based ethanol companies have competitive advantage than standalone grain based ethanol players entering the industry smelling money. Why?

a) The input (cane) is exclusive to sugar companies, that cannot be diverted to new standalone players.

b) The power costs are extremely low for sugar companies due to availability of byproduct (Bagasse) used for power generation.

c) Cane based ethanol players can transform their distillery to operate on both cane and grains, based on the availability and hence, can sweat there assets better. - Incentive to farmer - Farmer will almost always sow Cane, because it’s the most remunerative crop for him. Its another matter that if cane arrears are not paid by sugar industry due to stress in the system, he may not grow cane next year.

- Sugar Industry dynamics - Above points indicate that sugar industry is not as cyclical as it used to be in the past. The demand is stable, and problem of excess supply has been tried to addressed by various measures by the Govt.

Negatives

- Irrespective of its support to sugar industry, Govt keeps playing its taper tantrum in one form or other and will continue to do so in the future. It will be rather pertinent to say that Government has complete control over the industry. Some examples:

a) In Dec 2023, Govt ordered sugar companies to not divert cane for ethanol production as it feared insufficient sugar inventory in coming season. Sugar companies were driving all the profitability from ethanol sales, which suddenly vanished.

b) In Dec 2024, Govt reverted back and allowed diversion of cane to ethanol, but did not increased ethanol prices from sugar syrup.

c) Recently Govt started remunerating grain based ethanol much higher than cane based ethanol - Cane crop can get infected with disease in any season. Recently Red Rot disease in UP caused decrease in crop yield and reduced sugar extraction as well.

- The price at which sugar will sell is not in your control.

Now after discussing the positives and Negatives, the question is how a naive investor can play the game? Its not easy, as at end of the day sugar cycles is what drive the return and trying to predict it is not possible, at least for me.

My thoughts are that we can invest in sugar companies with track record of execution and efficiently running the mills, when they are available at fraction of the book value, and wait for things to get get better. Its easier to say but extremely hard to do.

Assuming you have done the buying part right, its still half battle won, as the game does not end there. If cycle plays in your favor, you now need to decide when is the right time to exit.

So, its not a easy game, and that’s why it can be very rewarding as most of the investors leave it altogether. If you track it, and if you spot risk reward strongly in your favor, you may bet/invest.

Apologies for long post and unstructured write up.

4 Likes

Great post i also feel ,one needs to bet on the promoter as well beacuse cost of production due to efficiency can make or break the company even 1 or 2 rs margin can make a company profitable and non profitable is different for different companies and even there can be difference .

What do you think the best price to book is for a sugar company?

• The main issue seems to be that a significant portion of the profit is being used for debt reduction, while interest payments continue to weigh on the company. So far, they have reduced debt by more than 50%, but it has taken several years to reach this point. Going forward, the pace of reduction might accelerate—perhaps within two years, or at most three.

• However, they are profitable. The impact on reported earnings is primarily due to depreciation, which is more of an accounting adjustment.

• They own the highest number of sugar mills/plants in the industry. Even selling one plant they can clear this debt completely (Just saying ![]() )

)

• Now, it’s a waiting game for the ethanol story to unfold.

I welcome further insights on the previous query as well as this one.

Note: Holding this and Mawana in the family portfolio, so my views may be biased.