Global sugar prices sharp rally” in talks with industry experts

By Shivaaneey Rai -Thursday, 14 January 2021

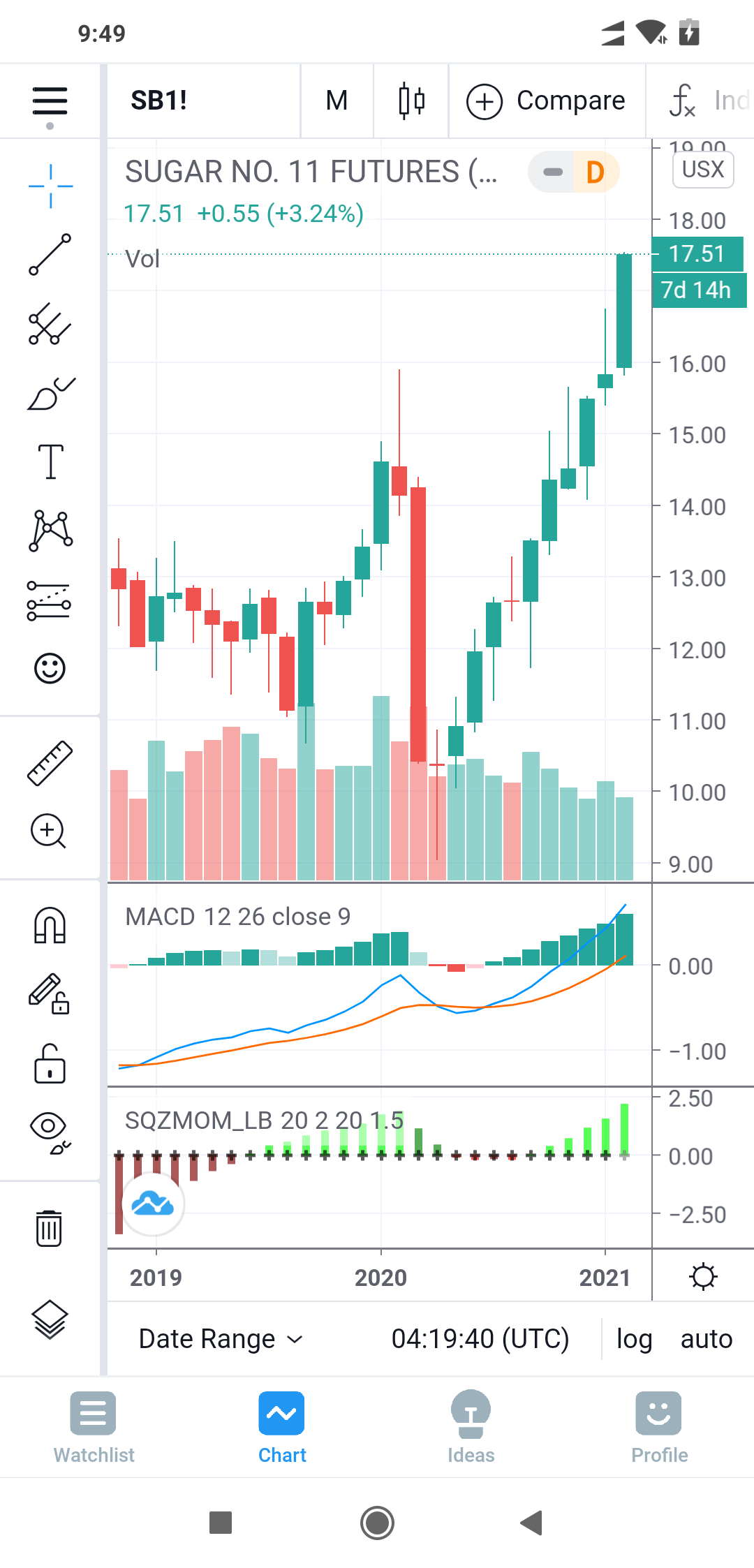

Global sugar prices have rallied sharply however the industry is in a nail-biting position to solve the puzzle of whether the current rally has solid fundamentals. March NY world sugar #11 (SBH21) at the time of writing this article is +0.64 up at 16.48 (+4.04%), and March London white sugar #5 (SWH21) is trading +10.20 up at 459.30 (+2.34%).

In conversation with ChiniMandi News, a few industry experts shared their views.

Mr. Michael McDougall – Managing Director at Paragon Global Markets, LLC, New York, USA said,

“We just jumped now as buy stops were activated above 16.22, the high from earlier today and then 16.33, the recent high. SO that is bringing in more technical buying. There is talk that Pakistan might import 300 K of sugar to try and calm down their internal market, though most likely it is more threat than reality. Additionally, there is also talk that Brazil is well priced already with anywhere between 69-80% of exports fixed in the futures markets. That is up significantly from the 29% last year. So the selling above is most likely much lighter than we would normally see at this point. I would say it is “Any excuse for more juice”. Commodities are attracting attention from funds and with all the money sloshing around, they just need any excuse to buy more”

Mr. Arnaldo Luiz Correa – Director at Archer Consulting said, “Well! I think the market is rallying for no fundamental reason. In my opinion it is more a technical and the knowing funds activity. March has basically no sugar from Brazil so the market can freely continue to go up and I think it’s a great opportunity for the Indian exporters to fix their sugar in the global market. And I still think for the 2021-2022 crop in the Central South of Brazil thats related to the months of May, July, Oct 2021 and March & May 2022 if you take the average something like almost 14 to 15cl/b because the market is inverted, May has a higher price and I keep saying that I don’t believe for these particular months we are going to see prices much higher than 15cl/b in average or if you are expecting 16c/lb we need to have a perfect storm to make that happen. One thing we cannot forget is the fact that the consumption of sugar worldwide has probably declined due to the pandemic. We don’t have the accurate figures yet, but there has been no doubt that a shrinkage on the global has taken place which is estimated to be 2-3 million tonnes. I don’t see any fundamental change witnessed in the market to support the upward movement. One must be very careful while taking advantage of it. When we look at the oil prices, they’re still hovering between $50-$55/barrel which is a good indication that the fuel consumption worldwide has decreased and that will surely have an impact on the ethanol price in Brazil making the mills to maximise the production of sugar.

Mr. Marcio Perin, Senior Market Research Analyst – ED&F Man said,

“The last few weeks have been quite positive for the commodities markets. Sugar has taken a ride in this more beneficial environment. The non-commercial funds returned to the purchases, adding a bullish tone to the markets. However, this rally does not seem to be supported by supply and demand fundamentals. In the short-term, the flow is sovereign. But in the medium term, this flow can be reversed, weakening even more fundamentals.”

The above article supports #Mehnazfatima view on the weakening of prices in the medium term. Let us await for the hardening of prices in International market to take a plunge in impending sugar rally.