buyback of balrampur chini

PAT up 3x of triveni engg q2

cons PAT from rs22.2 cr to 67.9cr

bcm results are also in line

dhampur sugar

in contrast few laggards yet to catch up the party

Is it time to worry about our Sugar stocks and start booking out our Profit/ Losses…

Or wait for another relief Q3 … Q4 results rally …

Another point I wanna ask is government is constantly saying about Ethanol use…

Even in the recent rally of PM ModiJi in UP last Sunday he spoked about Sugar and ethanol … so should we focus on Sugar Stocks who have better Ethanol capacity…

And spurt in crude now can benefit those ethanol producers…

Regards

2 Likes

Various issues internationally to keep pressure on sugar prices.

http://gulfnews.com/business/companies/mideast-sugar-refiners-face-intensifying-competition-1.1938132

Sugar futures crashing below support level. Looks like the top was made at 23 cents. HDFC securities guy called it correctly. Sick.

Everyone wants to hold it for 3 months and exit …to find a greater fool. Sometimes in this game we(I) happen to be that one

Brazil’s sugar industry sees no quick end to global shortage

http://www.brecorder.com/agriculture-a-allied/183/109380/

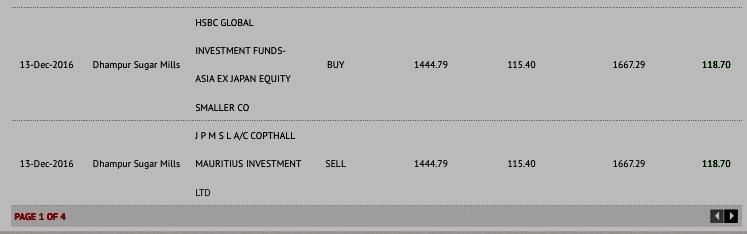

On 13 December there was a Bulk deal in Dhampur sugar where HSBC Global bought a good chunk at 115.4 … looks like institutional interest still there in this sector …

and now hope so we may soon see this consolidation getting over in sugar stocks as a whole… with Q3 and Q4 in focus now …

The worry part US Sugar 11 is now at 18.40 $

UP sugar mills recovery realisation has gone up by 500 basis points which augurs wellfor better profitability this season though post demonitisation, denting of sentiment has reduced retail sugar price by Re 1 to 1.5 per Kg

.

50 basis points, not 500. 500 would be huge. The link to your article does not work, but I guess that the normal recovery in UP is around 10-10.5 %, so this time it will be 10.5-11%. This should augur well for profits.

ISMA:

ISMA:

2016-17 sugar supply seen comfortable, no imports needed

2016-17 gur output to see a significant fall

ISMA sees 2016-17 closing sugar stock higher at 6.0-6.1 mln tn

ISMA cuts '16-17 sugar sale estimate to 24.5-25 mln tn vs 25.5 mln

Uttar Pradesh Oct 1-Dec 15 sugar output 1.8 mln tn vs 0.9 mln

Maharashtra Oct 1-Dec 15 sugar output 1.73 mln tn vs 2.25 mln

After a long time whole sugar sector is performing very well today …

hoping for an end to the consolidation… and new rally to start…

since technically too most of the stocks will be closing at their weekly highs today

expecting a good next week too …

but what started the rally today … am i missing an announcement

or if someone could update if there was any news !

regards

Manish

After going through the recent concalls its very clear that the total production number will be less than 22 million tonnes. India will have to import sugar in 2017. There is no escaping that.

In the next leg south based sugar companies with refining capacities will the biggest gainers , as they are closer to the ports and can involve in lucrative trading . UP based sugar companies will miss out on that.

One point not mentioned fully in the report is the port based refining capacity. It imports from wherever raw sugar is available cheap , refines it and exports it to nearby countries. Right now they are not allowed to sell in India. But when India is importing sugar, it can sell directly in the local market. The margins will be extremely high.

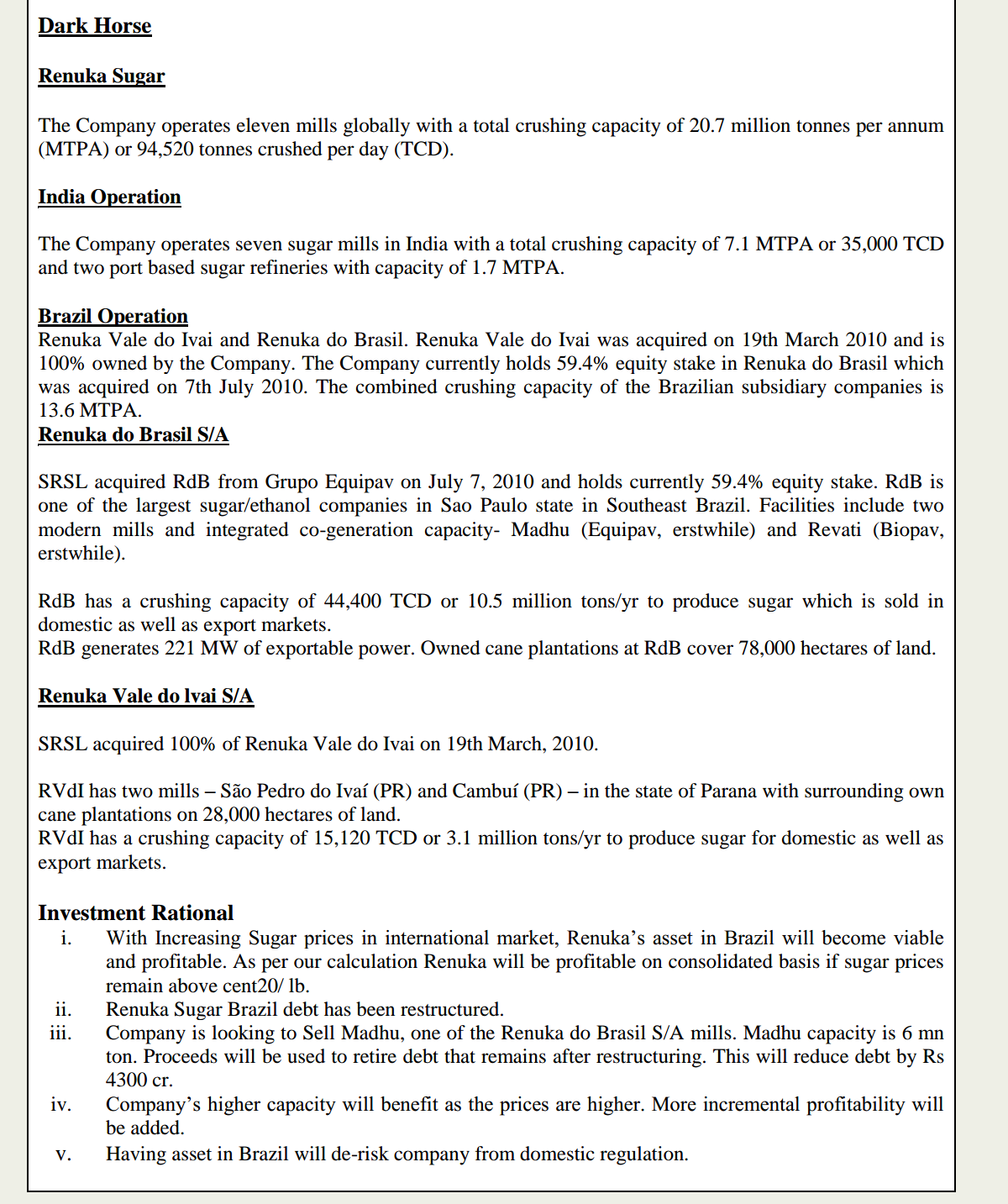

http://m.thehindubusinessline.com/companies/renuka-sugars/article9124879.ece

I recently exited dwarikesh and dalmia sugar. I have entered Shree renuka.

The reasons are

-

Debt reduction : By Jan 23rd its Renuka do brasil subsidiary will be auctioned off completely( Both revati and madhu plant) .4300cr of debt will be wiped out. This was Renuka’s biggest problem. Just this one event will rerate the stock.

-

Still renuka will be left with one Brazil asset. A very attractive asset. Renuka do ivai with 3 million tonne capacity and 28,000 hectares of cultivable land and certain port assets. This subsidiary will have only Rs 1000cr debt, to be paid back only in 14 years at 5% interest rate.

-

Its port based refinary in India already earns 5000crs sales at 10% margin. This will only increase as the year progresses. Its valuation alone will be higher than the current Mcap.

-

Valuation : Its grossly undervalued. Available at dirt cheap price because market looks at renuka with clouded eyes, looking at the debt picture. …even though it will mostly disappear in the next 30 days.

-

Tamil nadu based Shyam sekar of iThought has entered Shree renuka. Though I hate him for his MFI ,NBFC comments ,tweets, interview etc … His expertise here in sugar sector is very high and he is piling up renuka in a big way. He has a history of identifying and taking up big stakes in dhampur , balrampur

Last point probably is more of a confirmation bias but its like a thick filter test.

6 Likes

Thanks this looks really interesting. However do you have any link or insider news which can substantiate this claim.I tried finding on internet but could not get my hands on any. What i got is this -“Renuka’s mill madhu fails in first attempt” Is this correct? And second auction is to be held on 23rd Jan 2017.

Yes first attempt failed. Second attempt involves letting go of the entire renuka do brasil . Going forward …renuka will be a domestic sugar story again. Its refinery capacity the trump card.

consolidated debt is in range of 9100 crores. only 4300 crores will be paid off. so substantial debt will still remain. is that so?