I am summarizing my research and investment thesis on Strides here, for everyone’s benefit. Please feel free to poke holes in this and pose questions/comments.

About the company

Strides Pharma is a global branded generics pharma company that sells products in 100+ countries and has manufacturing plants in over eight countries worldwide.

Strides main headquarters is in India with a global headquarters in Singapore. The reason they have a Singapore HQ is cause Singapore doesn’t have capital gains tax, so whenever Strides divests a business (which they do a lot) they tend to benefit by saving a large chunk in capital gains tax.

The same strategy is deployed by Flipkart and so many other savvy businesses.

Strides also has a Singapore manufacturing unit. The benefit of having a manufacturing unit in Singapore is that its one of the countries that has a good designation with USFDA and any pharma products manufactured in Singapore, gets USFDA nod relatively easier. (There are some other favorable Singapore specific policies as well, if someone is aware of them, please comment them here).

Divisions of the Company

Strides operates in three main divisions

- Branded Generics

- Pharma Generics

- Institutional Business

Branded Generics This is the main cash cow and most profitable part of business for Strides. Branded Generics simply means generic medicines that are sold under a brand. For example, Crocin Pain Relief is a branded generic. These products are like FMCG, they command loyalty from their customers, customers do not like to replace the product frequently and once a brand is established you can pretty much sell anything under it.

Strides sells majority of its products under branded generics. Here is an example of a brand Strides has created for children (for its regulated markets)

Pharma Generics This is simply a generic business, similar to the likes of Granules. Strides does earn some portion of its revenues from this business, not a lot. I believe branded generic business will keep getting stronger and as such this part of the pie should get smaller with time.

Institutional This is the tender driven business with tenders given out by WHO, GAVI etc. Very miniscule low single digit contribution of this business to Strides revenue pie. I imagine this along with Pharma Generics are there as complimentary businesses for Strides.

In all essence, Strides is a Branded Pharma Generics business that operates in a majority of countries worldwide.

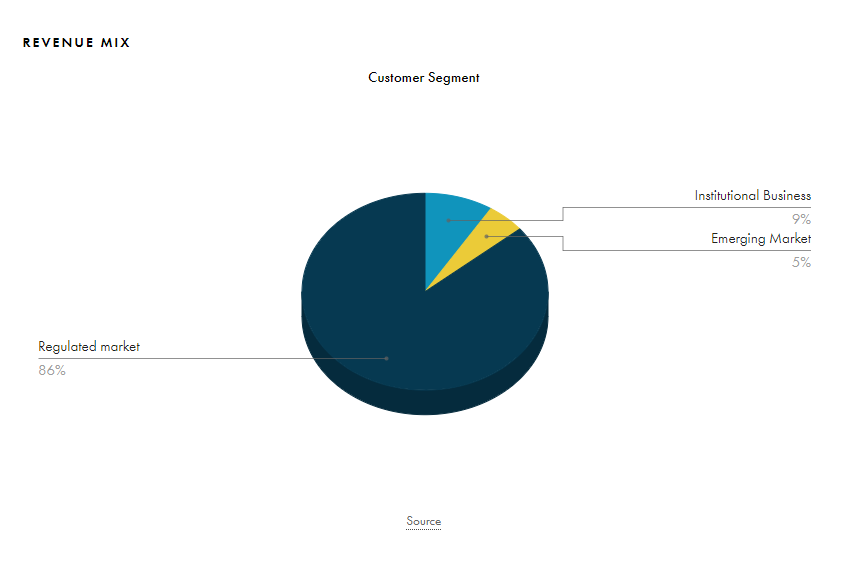

This is what the revenue pie of Strides looks like

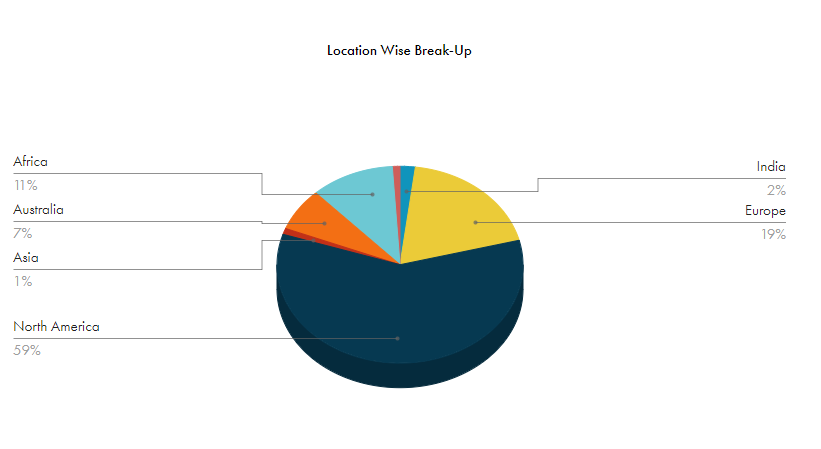

and this is how different geographies contribute to Strides Revenue

Regulated + Other Regulated Markets (Europe, Canada and Australia) make up about 85% of the total revenue pie for Strides. This is good cause Canada and Australia are highly profitable markets and both have a similar pharma market structure for generics. Strides once used to rule Australian generic market before they made several divestments (there are many divestments throughout the lifetime of the business which makes it hard to track as it loses continuity, if someone knows better then please highlight).

For each of its Regulated Markets, Strides has a front end (Pharma speak for a sales team). Having a front end is very important esp. for US Markets as its these pharma sales reps that reach out to doctors and help them substitute their products in prescriptions. In US markets, only what is written on the prescription can be dispensed to you by the pharmacist, its a crime to dispense something else.

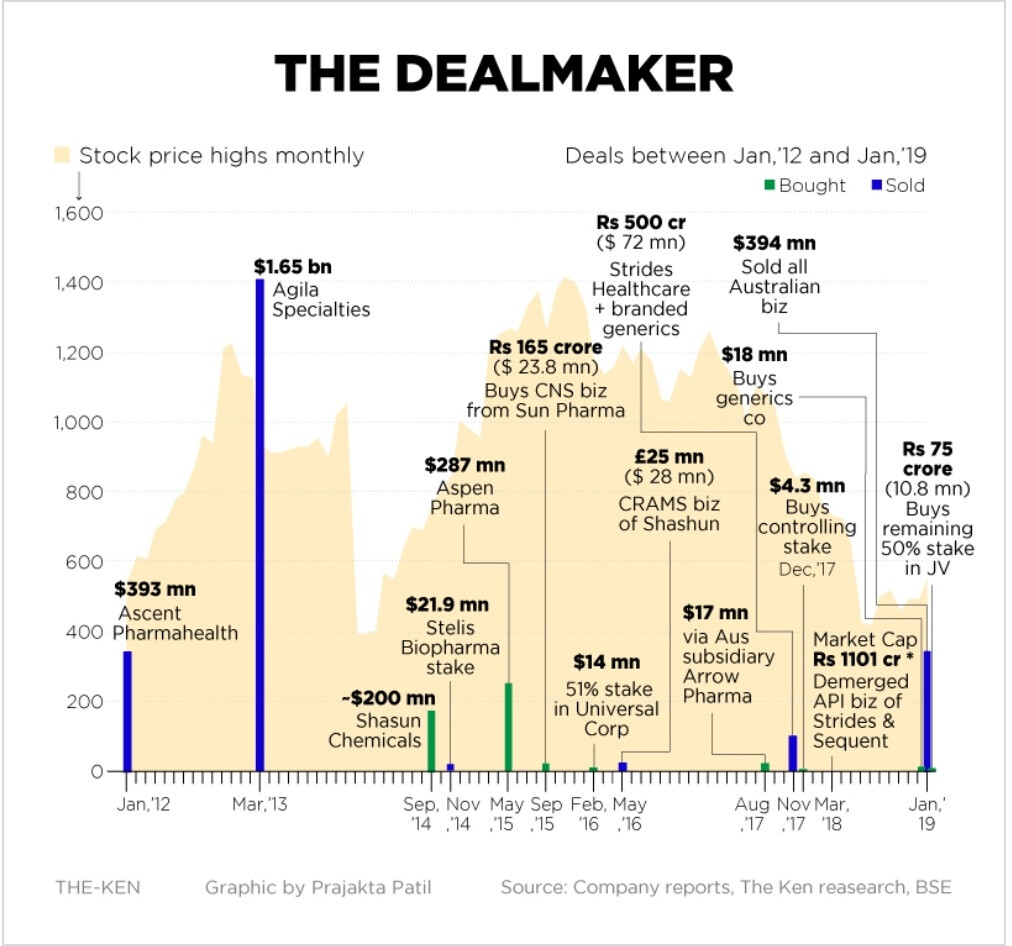

Here is a snapshot of everything Strides bought and sold during its lifetime.

Till 2020, Strides was better evaluated as a Pharma incubator business, as they consistently bought and sold businesses. Whoever is the new promoter (I write about it later in this thread) will definitely provide some stability to the business and maybe that’s why the top management team has been firmed up and represents a very strong professionally driven team recruited from top pharma names worldwide.

I am not going to write about the known parts about Strides, its financials etc. you can get those details from its investor presentation.

Here are some lesser known growth areas for Strides

US Veteran Affairs Business: US VA has an annual 100 Billion USD plus budget for sourcing generic medications for its members. Since this a govt sponsored budget, they usually want majority of sourcing to be done by American Firms that produce products in American Plants employing Americans and paying American Tax. For this purpose, Strides set up its Florida manufacturing plant, some part of manufacturing in Singapore is also routed to VA program. This should be a big revenue driver for Strides for its US business which is already 59% of its revenue pie.

Canada Business Strides has a well crafted and clear strategy to enter and gain market share in Canada. They are in execution mode and this business should show meaningful growth in the coming years for Strides. Same goes for their Australia business.

Africa Business This is the fastest growing area for Strides with revenue growing by over 65% last year for Strides in this region. Strides employs a ‘In Africa for Africa’ model which simply means that they are manufacturing employing and selling to Africans nations. Strides has a its own front end here as well. While this is a fast growing business, dollar wise it doesn’t amount as much as US or other regulated market business for Strides.

Sterile Injectables Strides is the leader in developing sterile injectables. Sterile Injectables simply refers to medicines that are given via injections to either veins or by IV. They cannot be consumed orally. Strides was a leader in this space when they built their Australia business and sold it off to Mylan for USD 1.2 Billion. 7 years since, their non compete with Mylan has ended and Strides wants to re enter this business. Interestingly, no one not even Mylan has been able to advance or replicate the sterile injectables business like Strides did. Manufacturing of Sterile Injectables (SI) is a difficult task, you need to have a separate manufacturing unit as the unit that produces oral medications cannot produce SIs and its a compliance nightmare to have both SI and non SI product manufacturing in the same unit. To counteract this problem, Strides is outsourcing all manufacturing of SIs to CMOs and simply using its in house technical and research expertise while outsourcing all manufacturing. This effectively removes any headache or investment from Strides into SI manufacturing and compliance while also allowing it to enter this market again. This business should deliver some revenue additions in next 2 years or so. Arun Kumar Family Office is also launching another company called SteriScience which will manufacture specialized SIs, Strides has the option to pick and choose which SIs it wants to participate in.

Transformation of the company Under the new CEO, company is on a transformational path with a professional leadership and management team in place. Gone are the days when Strides used to undertake huge investments on direction of Arun Kumar to incubate several pharma businesses and sell them off couple years later at a big profit. Strides now is a pure branded generic pharma business that operates in majorly regulated markets. This was evident when current CEO refused to put more money into Stelis or SteriScience.

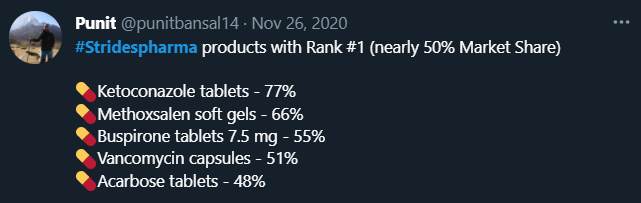

Products and Pipeline Strides has the maximum ANDA filings of any company in the world. It has over 120+ ANDA filings out of which 100 ANDAs are approved. Strides also has market leadership in majority of its products. Here are a few examples below

US FDA Compliance Strides has a good record of US FDA compliance with only 1 warning letter and observation in the history of the company for its Puducherry plant. Strides follows a two manufacturing site for each product method where every product is produced in over two sites globally, so the Puducherry observation didn’t drastically impact Strides ability to earn revenue. Further, Strides, has now divided the quality management role into two separate roles with quality assurance professionals having a direct reporting line to CEO. This should ensure no future instances of such cases.

Rest of the stuff is pretty well known for Strides and discussed multiple times in this thread so I won’t be repeating it here.

Short Term Risks Shipping costs is a major short term risk for the company, it dampened last Q margins and I expect it to impact this Q margin even more severely cause shipping costs have risen further 5 fold in last few months.

D: Invested and playing out a investment thesis, may exit anytime or may stay invested for long run, please do your own due diligence

Note I do not know why promoters are selling shares, I do not know which PE will take over, I do not know when Stelis will be demerged and I do not know what price will Stelis be demerged at