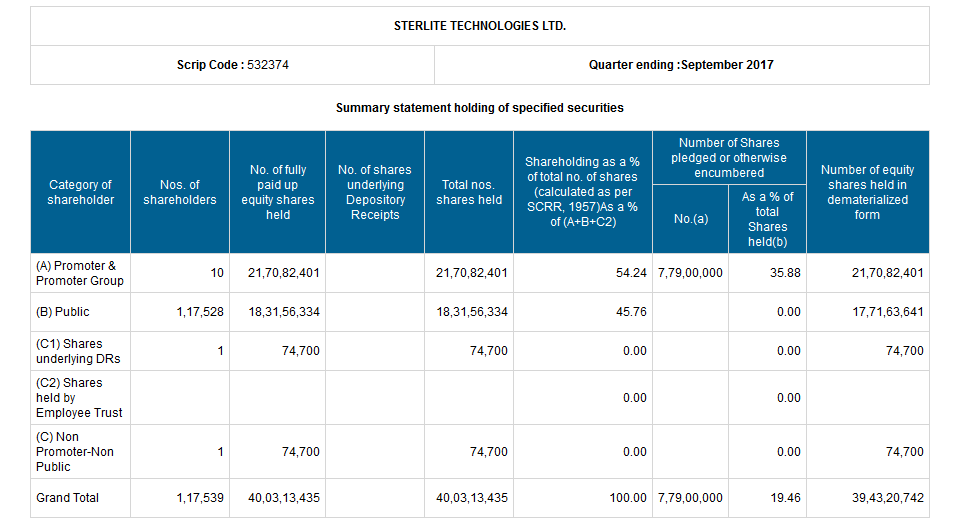

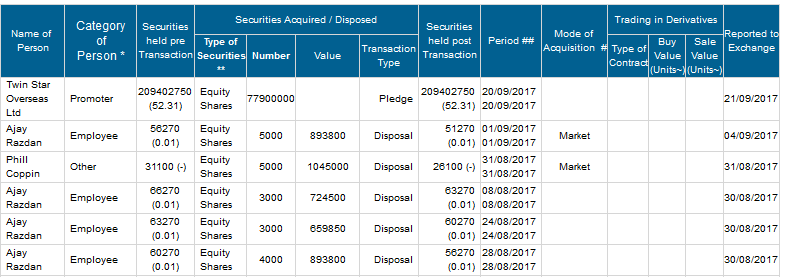

Why have they pledged shares this quarter ? Any info ?

Highlights for Q2, FY18

• Net Revenues stood at Rs 779 crore, up 42% Vs Rs 551 crore YoY

• EBITDA at Rs 179 crore, up 63% Vs Rs 109 crore YoY

• Profit After Tax at Rs 71 crore, up 40% Vs Rs 51 crore YoY

• ROCE of the business stood at 29%

D/E reduced from 1.1 end of FY17 to 0.80 post Q2 FY18.

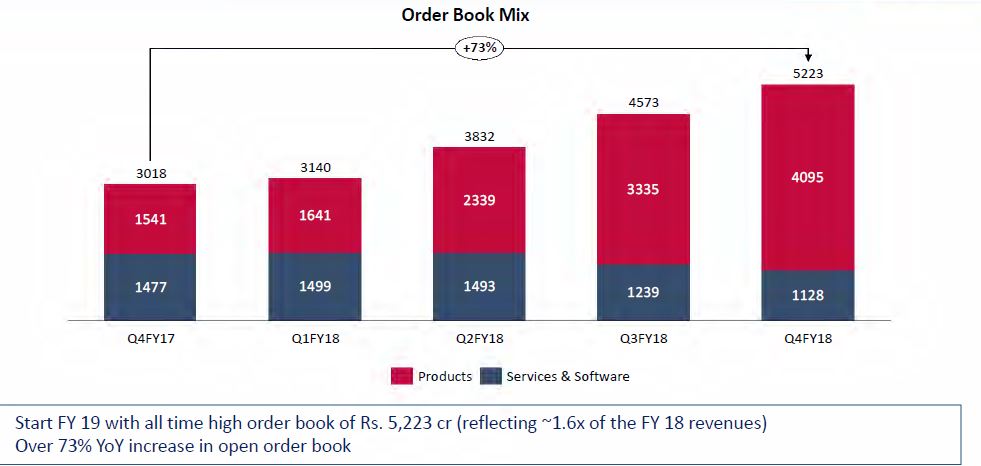

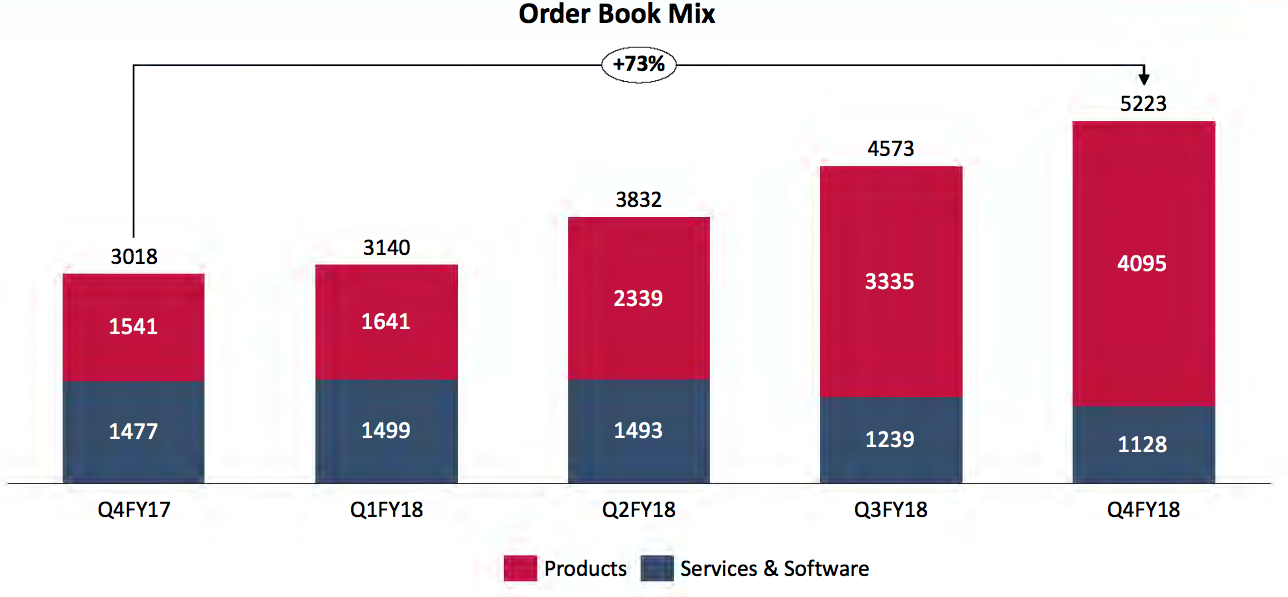

Overall open order book value increased from Rs. 3,140 Cr (at the end of Q1) to Rs.

3,832 Cr. Open order book to be further strengthened during Q3

http://www.bseindia.com/xml-data/corpfiling/AttachLive/3e0409fa-f429-4849-a14a-a2ff2f422fc1.pdf

1 Like

2 Likes

Rs.3500 Crore order from Indian Navy. This should effectively double the order book.

1 Like

The order book at the end of q3 was about 4500 crores. With this total order book stands at 8000 crores.

1 Like

The stock price has fallen quite a bit from it highs. Hopefully, a healthy correction has resulted in a good entry point this promising business. Any technical calls on what could be the next support levels to watch for?

In Elliott Wave terms, I see wave 5 of wave (3) ending at 407, and now correcting in wave (4). The stock may correct up to 262 (38.2% retracement) or could be lesser too. In worse case, can correct up to 216 (50% retracement) or in the worst case, can go down upto 120 (I don’t think that will happen) which is the end of wave (1). Since wave (4) can’t go below wave (1), 120 should be the lowest in case of recession or something. But in the long run, I see huge upside from CMP. If my Elliott Wave count is correct, it’s buy and forget kind of stock (at least for the next 5 to 6 yrs).

Here’s my chart.

https://www.tradingview.com/i/bCldukXT/

Disc: Interested. Looking for good entry point.

4 Likes

This might help boost Sterlite Techno’s margins. Especially since they already have a product for WiFi offload:

http://www.elitecore.com/pressrelease_wifioffload_mwc.htm

1 Like

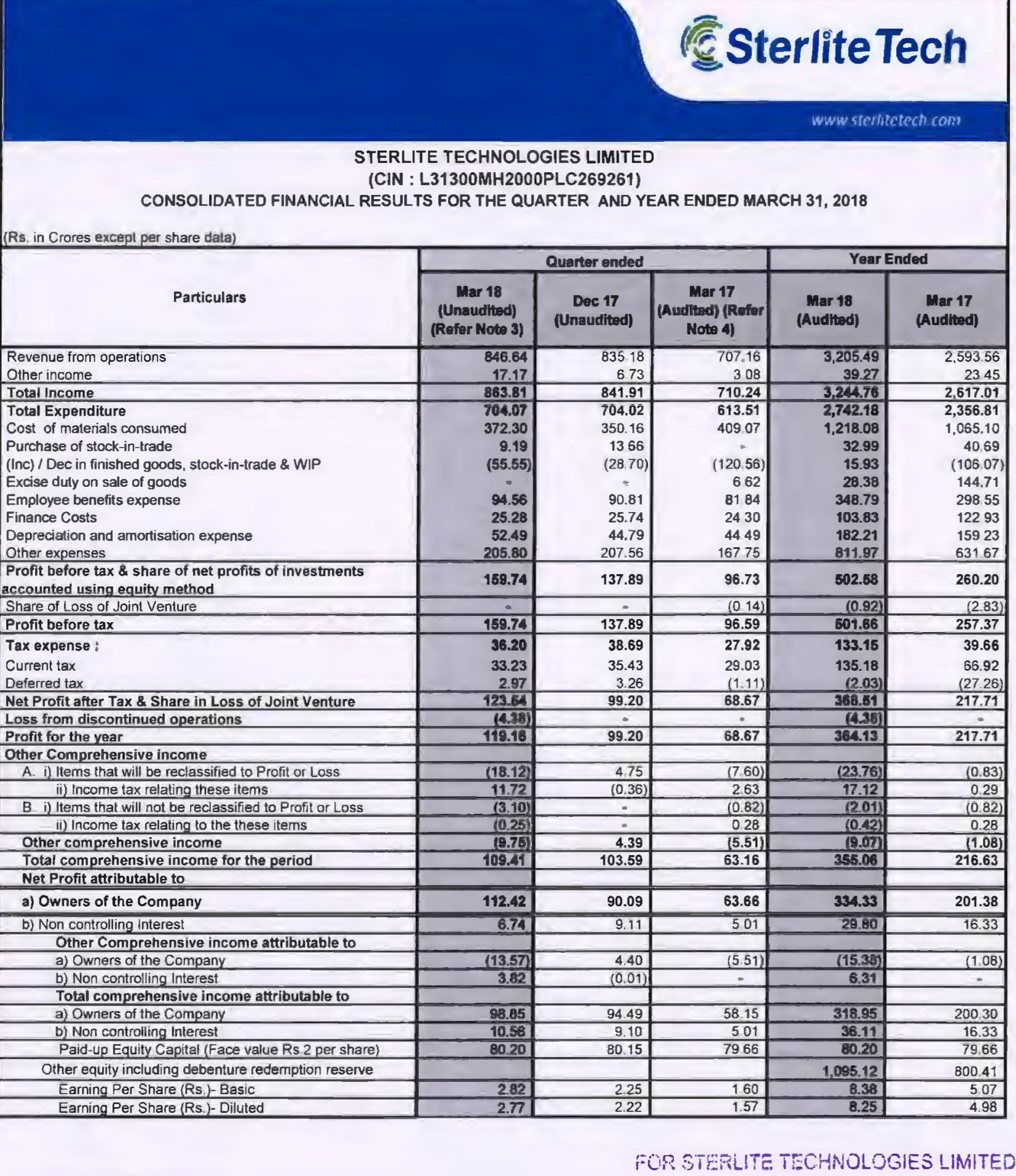

Excellent numbers from Sterlite Tech Again:

Here is the earning update link:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/55e021ad-4648-4a0f-8064-054d3ca86451.pdf

The results are once again very good. I like the consistency. But the order book at the end of Q3 was 4573, they say now it is at 5223. But they have a pre-purchase agreement with Indian Navy for orders worth ~3500. So should not the total order book stand at 5223+3500 = ~8700? Which is 2.5x 2018 Sales?

Disc: 15% of Portfolio

Orderbook at 1.6 times FY18 revenue at 5223 Cr. But I am stumped why this is not higher as the navy order of 3500 Cr came in Q4. I see only about 650 Cr increase in order book in Q4.

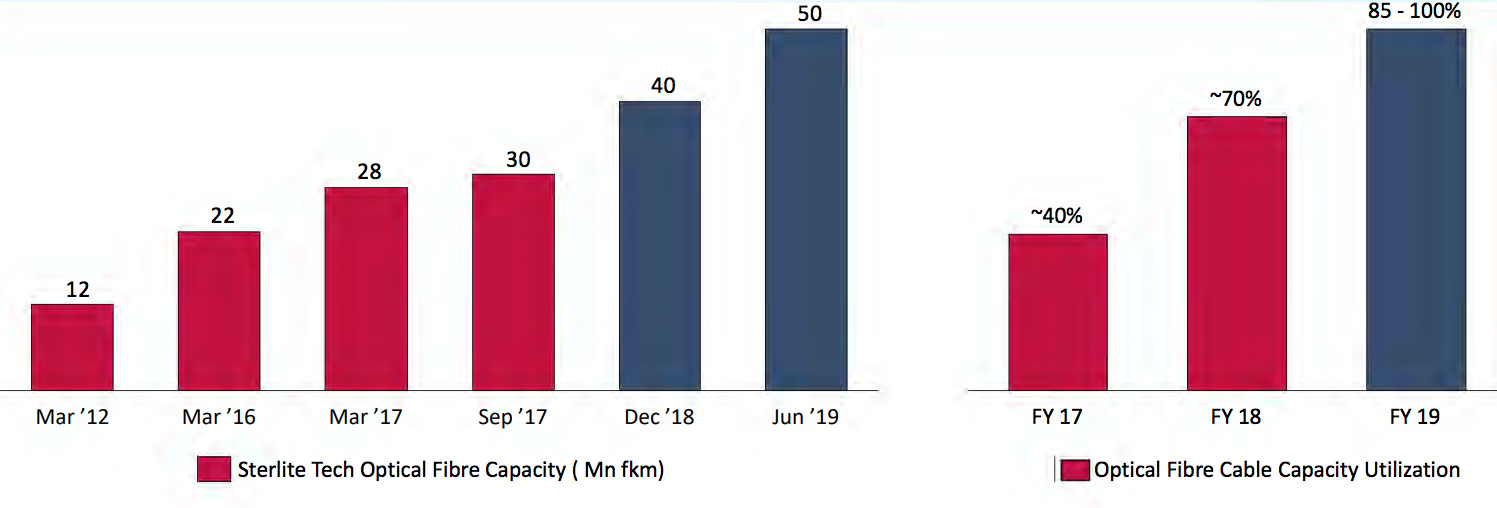

Capacity utilisation is projected to reach 85-100% which should provide excellent operating leverage.

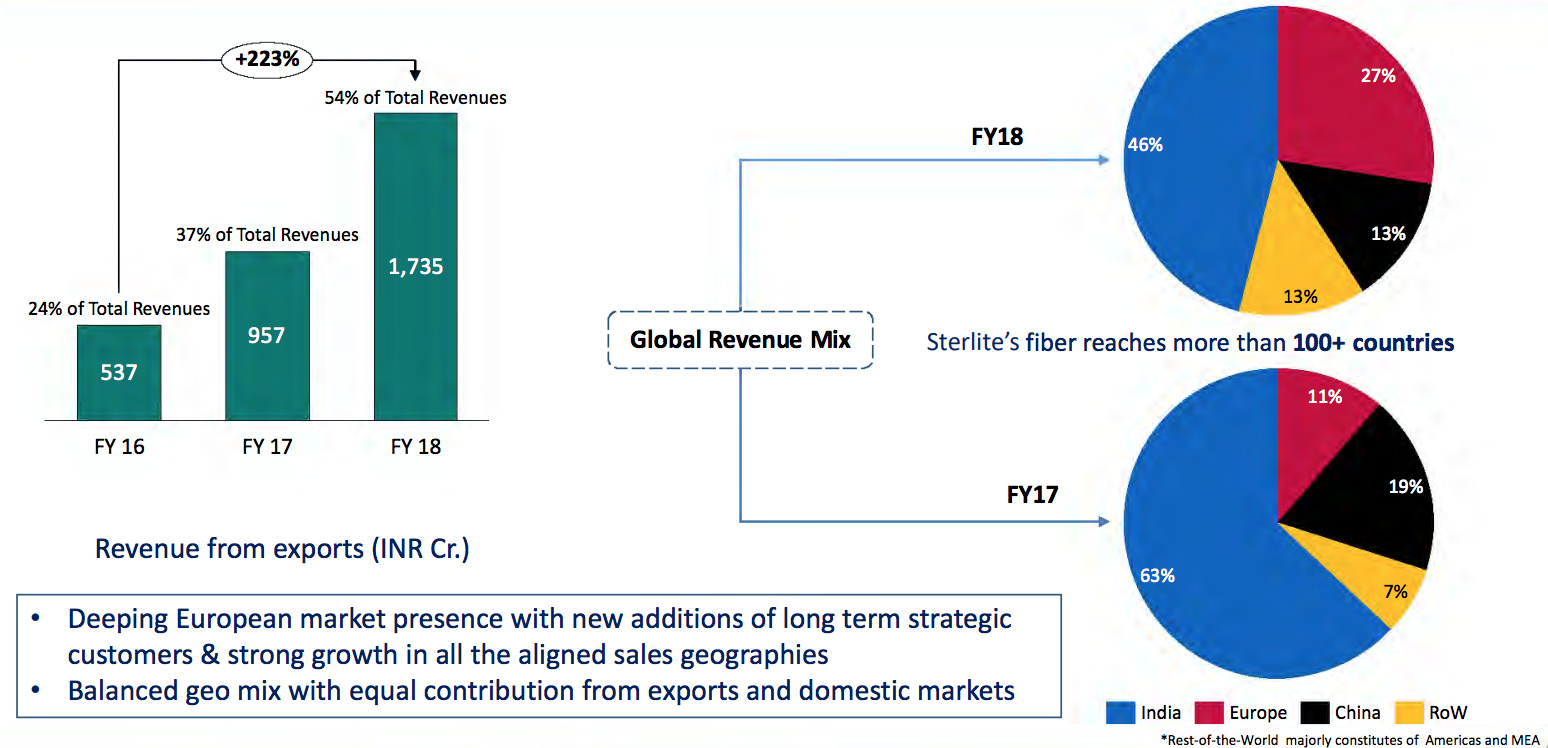

Export contribution has been rising higher and higher (24% to 37% to 54% in last 3 yrs) with each passing year which is a nice thing but its a double-edged sword exposing the company to global shocks.

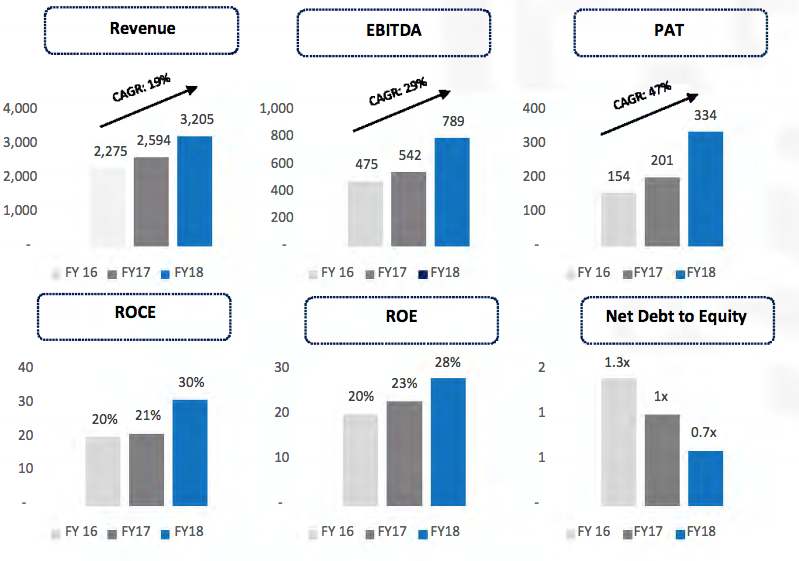

FY18 has been excellent with RoCE rising to 30% from 21% and RoE to 28% from 23%. D/E is down as well.

Currently trading at 40 P/E so is not really cheap but FY19 at least promises to be good. Got to watch the orderbook position and figure out why the Navy order is not figuring in it.

Disc: Invested

4 Likes

They explained in the call that the Order book of 5200 crores does not include the 3500 crore navy order because there are processes to comply to. For the Purchase Order, there are requirements of a cabinet approval from the Department of Telecom which will take 2-3 months. However the order (Advance Purchase Order) is secure.

3 Likes

Very good Q4 FY18 concall. Noted some important points from business point of view (left numbers).

-

Even the most conservative estimates of fiber deployment for 5G network factor a jump in fiber consumption of at least 2.5x compared to 4G. Extensive fiber demand is here to stay for another 10 years based on 5G deployment cycle in next say 8-10 years. We believe that this trend will continue with as the networks grow tomorrow with much higher bandwidth coupled with ultra low latencies that will magnify the role of fiber in the overall network CAPEX. 5g cycle is just starting now…it in itself is not contributing anything to our revenue right now.

-

In Calendar year 2017, we witnessed global demand for fiber surpassing preform capacity for first time ever keeping the tightness in fiber supply demand dynamics. We expect the global demand supply mismatch to persist in 2018 and growth in global demand will continue to enable the absorption of plant capacity additions on the preform side.

-

Regarding question on global preform shortage and new global capex to coming online in FY19 (2 year cycle) - We keep a tab of the new capacity, but it is difficult to know exactly when. The industry continues to be slightly not very open but what we are looking essentially is that the supply demand situation will continue to be tight, which is reflecting of the fact that we are actually now booking orders for the calendar year 2020 as well. So we are fully booked for 2018, we are largely booked for 2019, with the expanded capacity and we are booking some for 2020 as well. Reflection comes from what we hear from the suppliers and customers. The fact that our customers were wanting to give us contracts for 2020 gives us the confidence that the supply tightness might continue till then.**

-

Delivering both products and services and measuring outcomes at multiple stages of the value chain has provided invaluable perspective and insights enabling us to reengineer products and processes to solve customers’ network requirements and increased asset monetization. As the only company with end to end capability that extends it to software, we are uniquely poised to cater to the present and emerging needs of the networks of the future.

-

Now have a very balanced geographical split to our revenues with both exports and domestic business contributing equally to the top line and equally strong future outlook.

-

Out of 3,500 cr order, 75% will be system integration and about 25% is O&M for the subsequent 7 years. No EPC, no products. The margin profile is very similar to what we have for the other system integration business, about 12% to 14% (PAT level).

-

Utilization - Fiber running very close to 100% and OFC running at about 90%.

-

Margin improvement in Q4 is a result of couple of things. In short - 23% last year to 25% is due to better volumes, better operating leverage and more value added products. In detail - One that the products and services the ratio has been more skewed towards product. We have delivered better volume as compared to Q3 particularly on the fiber cable side where we have seen a better utilization coming close to 90% of capacity which was running at about 60% till last quarter. This one is sustainable. Number two, in terms of contribution of the new product continues to be there, so that is similar to last quarter, so that again plays a role. We can see part of this margin sustaining. We believe in growing the absolute value of EBITDA, the margin is a derivative of mix while if you look at from the full year perspective, we are still at 25%, so I think as long as we continue to maintain this kind of revenue mix, we would see that 24%, 25% margin. But absolute EBITDA we are quite sure that it will continue to improve on quarterly basis.

-

Margin in cable business is lower than fiber business but at the same time since we are now getting much better utilizations for OFC, operating leverage is coming in. So that is how the overall margins are improving and showing in the final result. Fiber business has great operating leverage and on

-

OFC the capacity utilization is increasing quarter-on-quarter.

-

Fundamentally continuing to be very-very bullish about the Indian market.

-

The order book currently is 5000 crore about 80% of which is towards the product side. With the Navy order happening, the overall mix will start becoming 50%:50%. It is very difficult to predict as to how the revenue profile will start looking three years from now.

-

We do not need to compromise on the margins with new customers (new geographies).

-

Prices continue to be very-very strong both at the spot level as well as long-term level. We are partnering with our customers particularly large customers so that we can continue to get visibility of volume rather than the realization, because as you have seen, for us volume certainty is far more important than the realization.

15 Likes

Thanks @Mridul. What I found interesting was the technical explanation of how 5G transition also means a much higher usage of fibre optics compared to a 4G or 3G. More details are available in the company presentation.

Disc- Invested and adding on dips.

Yup, decent insights on the industry.

My concern here is what happens once new preform supply comes within 2 years. This amazing re-rating got many tailwinds all at the same time starting 2017. How would things change when supply comes online? My feeling is that EBITDA margins would shrink for two reasons - one due to large navy order, and two due to supply demand coming back in balance post 2020. 5G is still some time away, so new orders on that front, we need to see how things play out.

Order book is known (growing at the moment at a decent pace but what happens on a larger base after 2 years), margins are at peak?, growth has peaked (in terms of CAGR) and this is at 36x trailing. Assuming 600-650 cr PAT in FY20, this is trading around 20x. Or is there still room for this company to dazzle?

At the moment, next 5-6 qtrs look good in terms of qtr on qtr EBITDA growth due to additional capacity coming in and operating leverage. Hopefully, EBITDA margins remain in 23-25% range for at least next 2 years.

2 Likes

Pretty good analysis. Should keep in mind that the best performance is behind it already or at-least plateaued ? The market did not cheer up to its brilliant results - already factored in the positive in CMP ?

I have a different view. The demand is just about starting globally. 5G is yet to launch, OTT videos just starting up in emerging markets and many of the robotic automobiles and robotic everything just starting up, the demand for bandwidth is at the cusp of inflection. And there is no substitute for fiber optics. This is going to be a structural story for next 5 - 10 years

Hi Raman.

Not questioning fiber demand. What we need to keep an eye on is -

How 5G demand emerges

How domestic 4G ramp up happens.

But equally important is to see how supply side situation changes in next 2 years. Preform segment in the manufacturing chain is where the supply demand mismatch exists; due to this Sterlite like integrated players and are in pole position at the moment.

Tailwinds are still very strong. But how i see things is demand comes at a steady rate, but supply is lumpy.

Another thing is that as mgmt clarified there focus is going to get long term orders (Volume is a big focus, not margins). So despite EBITDA gong up gradually, margins will come down. Order book at the moment in hand is already accounted for in price?

Just some mental models. I know everyone will have a different opinion.

1 Like