The Steel Pipe Industry Story is ripe and lot of tailwind going in for the sector. I have done a detailed analysis and am happy to share the details for the feedback of this group.

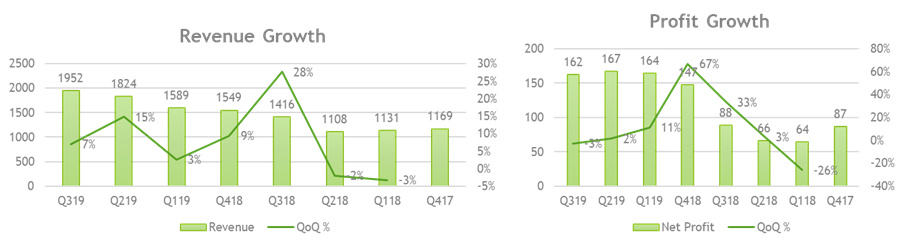

A. Top three India focussed Pipeline Manufactures : Ratnamani, Maharashtra, Goodluck – Last Eight Quarters Cumulative Results

-

Revenue and NP almost doubled in last eight Quarters – indicates a strong momentum on the numbers.

-

Discounted - Man, Apollo Tube, Welspun and Jindal Saw due to their Overseas exposure , balance sheet or low Margins

B. Valuation Comparison

- Goodluck Expansion is a brownfield one so will discount that

- Maharashtra Seamless is capacity acquired through NCLAT acquisition + Capex so not reflective of actual cost

- The actual replacement cost can be around 3Cr per 1000 MT looking at Ratnamani

- Ratnamani is a good company but expensive. Goodluck is available cheap but the balance sheet of MSL is better and Orderbook Scenario of MSL is far robust

- MSL looks the best bet based on the above parameters

C. Further Upside in MSL - Its Production is still at 55% @ 104 T as per Q3-19 with their current capacity so a long runway available for growth

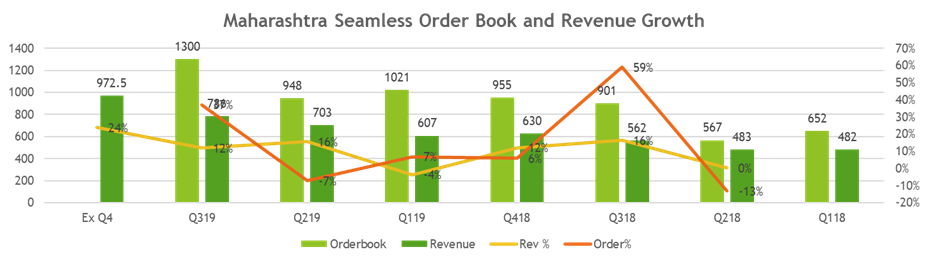

D. MSL Immediate Future Order Book

- Orderbook has almost doubled in 7 qtrs. like the Revenue

- Q3 Orderbook at 1300 Cr and the story is evolving and Markets should reward sooner than later

- Assuming 95% Revenue Contribution from Pipes the Blended Realization are

- This shows a very decent growth in Realization per ton and the Order Book further provides some cushion

Strong Order Book , Current PE of 8.5 and EV / Ton of 3.4 Cr at Near Replacement Cost minimizes the risk in favor of Investor

Disclaimer : I am already invested and views my be biased. Pls do your own research before any action