In 2022, SRF had said they will be doing capex of 15000 crore between FY 2024-2028, out of which 12000-13000 was towards chemical, how much of it has been incurred and how much is left?

2 Likes

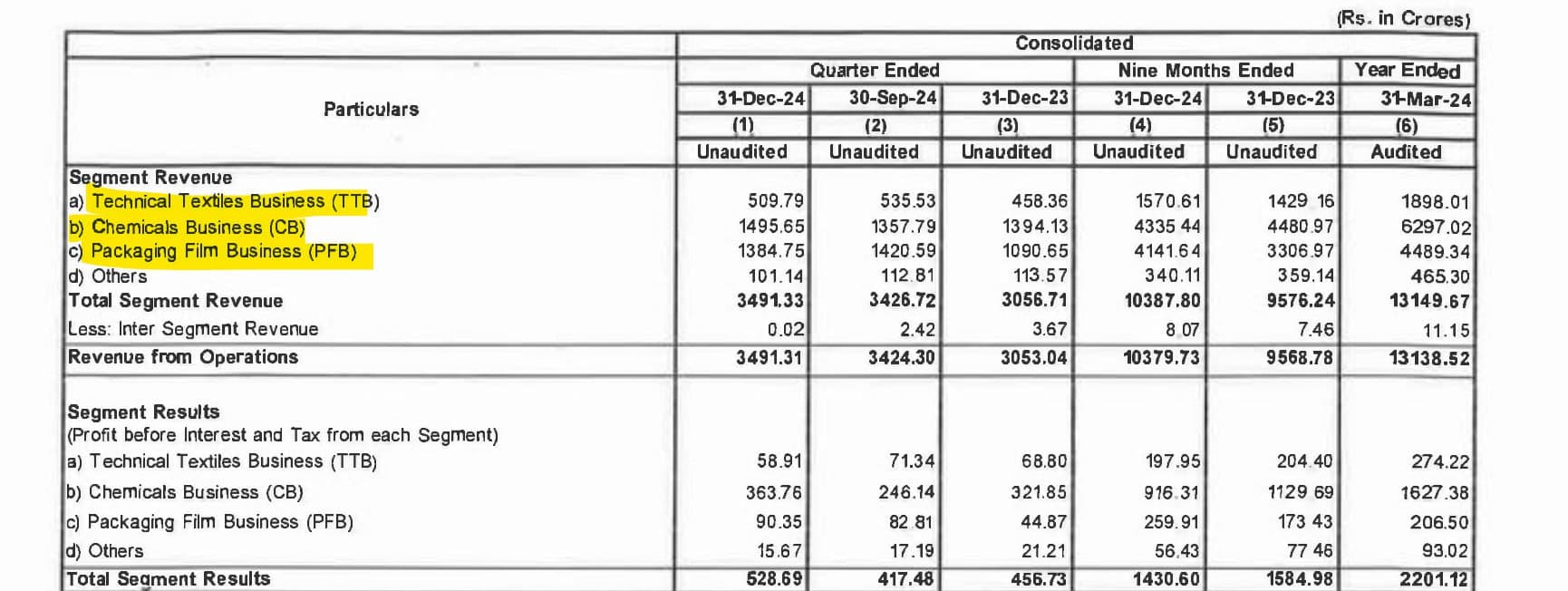

Results Out, key concern is drop in OPM% across the segments. Refer the calculations below:

-

Technical Textiles Business (TTB):

Q2’23: (74.95 / 506.15) * 100 = 14.81%

Q2’24: (71.34 / 535.53) * 100 = 13.31% -

Chemicals Business (CB):

Q2’23: (347.77 / 1426.30) * 100 = 24.38%

Q2’24: (246.14 / 1357.79) * 100 = 18.13% -

Packaging Film Business (PFB):

Q2’23: (77.26 / 1121.51) * 100 = 6.89%

Q2’24: (82.81 / 1420.59) * 100 = 5.83% -

Others:

Q2’23: (33.09 / 126.86) * 100 = 26.08%

Q2’24: (17.19 / 112.81) * 100 = 15.24%

Disc. : Holding through Kama Holdings, waiting for management commentary.

8 Likes

2 Likes

20% Up in last 3 days, SRF, Navin Fluorine shares rally 14% as refrigerant gas price increase

3 Likes

| Segment | Segment Assets (₹ Cr) | Asset Turnover (x) | |

|---|---|---|---|

| Technical Textiles | 2170.93 | 0.86 | |

| Chemicals | 11268.31 | 0.65 | |

| Films & Foils | 6926.69 | 0.82 | |

| Others | 257.20 | 1.48 |

Decent result for SRF, There is improvement in Marterial margins may be mainly because of increase in prices of PFB.

Has any one asked management about spin off of its Chemical business? Asset turns of CB is still about 0.6 times, there is ample room to grow the topline.

Chemicals Business

The Board has approved the establishment of a dedicated facility at Dahej to produce 12,000 MT per annum of an agrochemical intermediate, with an estimated investment of ₹250 crore, to address projected future demand.

Performance Films & Foil Business

The Board has approved a ₹490 crore investment to set up a BOPP film manufacturing facility in Indore, featuring state-of-the-art 10.4m wide Bruckner film line and a metallizer. The project is expected to be completed in 24 months. Impact of Jindal Poly fire incident. There is temporarily high spreads in BOPP, I heard Uflex is also coming up with BOPP capacity of similar size.

3 Likes

After nearly 3.5 years of consolidation, SRF Ltd has finally broken out — rallying nearly 50% since Nov 2024.

But this may just be the beginning.

SRF isn’t just any chemical player — it ranks among India’s highest capex spenders in the sector, with ₹2,200–2,300 Cr planned for FY26. ~70% of this goes into chemicals (especially specialty and fluorochem) —

- New manufacturing facilities

- New product lines (especially in fluorochemicals, specialty chemicals)

- Backward integration & process innovation

These capacities are starting to commercialize — and once revenues start getting booked, EBITDA will compound faster than topline thanks to operating leverage. That’s where the real rerating happens.

Capex = future EBITDA = future rerating.

This isn’t random optimism — it’s backed by structural demand (China+1, global diversification), SRF’s scale, and execution history.

The runway is long — and the ramp-up just began.

Institutions typically price in this growth 6–9 months in advance. Retailers join in at the peak with FOMO.

Then comes a correction, triggering panic selling. The cycle repeats.

The difference?

Conviction.

Research.

Patience.

Capex-heavy stories need time to play out. And if you’ve done your homework, these dips are not exits — they’re entries.

Disclaimer: These are purely my personal viewpoints, not investment recommendations. I am not a SEBI-registered Research Analyst (RA). Please do your own independent and thorough research or consult a qualified financial advisor before making any investment decisions. This content is shared for educational and knowledge-sharing purposes only.

13 Likes