Ayush,

Completion of expansion is a big plus. Q3 results will show a huge jump and you will see stock action following it. Almost 6% of my portfolio is invested in this company.

Most importantly, there is huge safety margin here.

Ayush,

Completion of expansion is a big plus. Q3 results will show a huge jump and you will see stock action following it. Almost 6% of my portfolio is invested in this company.

Most importantly, there is huge safety margin here.

Have done a brief post at blog recently:

**Sree Rayalaseema Hi-Strength Hypo (BSE Code a 532842, NSE Code a SRHHYPOLTD):**We haddiscussedabout the companyas expansion plants earlier. In theSeptember quarter, the company has reported a good growth of 27% in turnover and the stock looks quite cheap, if it is able to maintain this growth in up-coming quarters (which is should cause of the recent expansion).

The company is operating in a niche area of water treatment chemical a Calcium Hypochloride**and itas the only Indian company doing this work.The company has healthy operating margins of about 19-20% and the business requires little working capital. The valuations seem quite attractive as the stock is tradingat a PE of just 3.5 times and the Price to Book Value of only 0.50.**We feel itas a value pick at these levels.

Negativea The promoters have been increasing stake by doing preferential allotment and merging of group companies.

Hi Ayush, are you still holding? Can you provide updates on this stock?

Hi, I’m not invested

Can anyone please provide any update on the stock? Looks like there is a lack of growth. Your views the future potential of Hypo chloride business… Thanks…

Great resut posted by SREE RAYALASEEMA HI-STRENGTH HYPO LTD.

Howeve the concern : Is it the ONLY manufacturer of Calcium Hypo Chloride ?? Acooreding to a couple of websites , there are lot of companies in this…

http://www.indianindustry.com/chemicals/calcium-hypochlorite.html

http://www.tradeindia.com/manufacturers/calcium-hypochlorite.html

http://www.vigyanchemicals.com/industrial-chemicals/

Thanks

Disc: Tracking not invested

Is anyone still following this company? The claim that it is the only manufacturer or Calcium Hypo Chlorate seems to be worn down after all these years, with more companies entering the field, But the company still claims it in the company website. But the company continues to be cheap in it PBV and PE ratios. But the growth is still stagnant over years.

Disc: Tracking, not invested yet

SREE RAYALASEEMA ALKALIES AND ALLIED … - Environment Clearance

PDFenvironmentclearance.nic.in › TOR › 0_…

Recently Sreerayalaseema Hypo has amended the Memorandum of association and now they are coming up with carbon business.

They are importing coal for captive use and for tgv sraac. And rest selling in market. As it’s more cost effective.

Ps. Not invested in this company. Just tracking due to tgv sraac.as both agm is on same day on same venue.

Sree Rayalaseema Hi-Strength Hypo Ltd posted very good results

The stock is expected to be a key water treatment theme play…

It has continued to post decent results…

For the 9 month period, the profit has almost doubled from Rs.26.5 cr for Dec 19 to Rs.47 cr for Dec 20.

The PB is at 1.13, PE below 7… makes it very attractive and a candidate for accumulation.

The idea has not been heavily chased in the the last quarter…

However during the last 12 months, it has gone up 4 times from the lows…

With the EPS progressing steadily, it may have still lot more in store for the investors taking new position.

As of september 2020 half yearly basis cash in hand and bank balance 114 cr 39 cr mutual fund investments nearly 60/65 cr investments in TGV SAARC company changed to profit loss account AND present market value of property investment around 50 cr.

Approx 700 cr sales without considering trading and opm of 15 percent itself should give 100 cr. Virtually debt free depreciation claimed at accelarted 50 cr so the plant will become completely depricated which should add to the bottom line full tax paid NPM can be around 10 percent.

They have patent for the hypo process of calcium hypochlorite they manufacture 60/70% chlorine content calcium hypochlorite they are among the large manufacturers of this product.

They have increased the capacity for sulphuric acid and monochrlo acetic acid they have clear pollution control approval till 2025.

with WHO also given mandate for calcium hypochlorite usage as surface disinfectant during covid times the demand for hypo has increased the additional capacity of mono chlro actectic acid for pharma supply has also added to the top and bottom line.

Second line TGV bharat son of TG venkatash has already taken charge for last 4/5 years.

Cash flow is very good for the last five years and balance sheet is now clean all the preferential allotment is now converted.

For the present mcap cash and investment itself is approx 225/250 cr

Looks interesting at the present market cap

Discl invested

Interesting market research report on calcium hypochlorite

In this report Sree royal seema is listed among the leading players in the world.

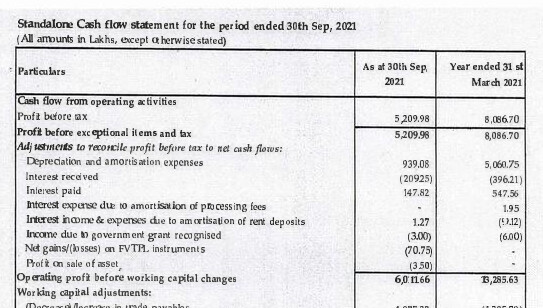

Interest received deducted and interest paid credited to OCF…what is the logic behind this?

I have a few queries for which I was not able to find answers. I would appreciate if any investor tracking this company can answer the following questions.

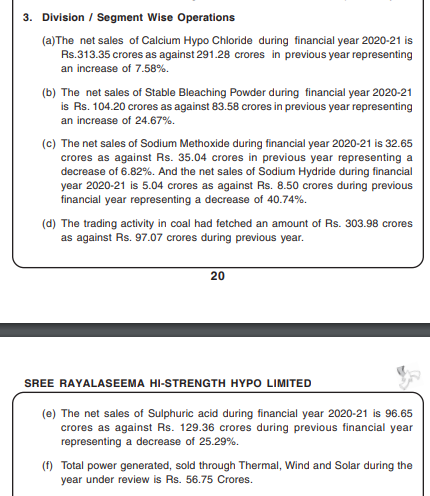

Annual Sales Data

Remarkable increase in revenues from trading of Coal and Bleaching Powder

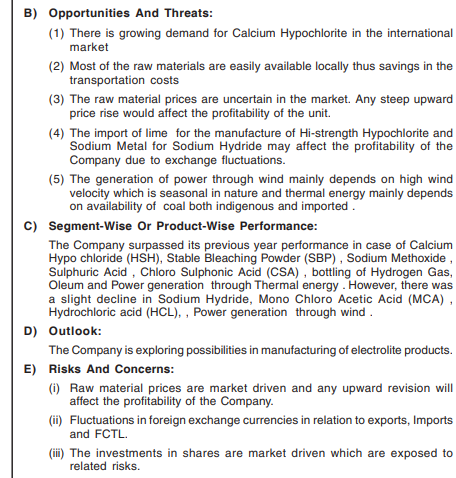

Opportunities Risk and Concerns

No discussion on mitigating the risks

Improvements Made

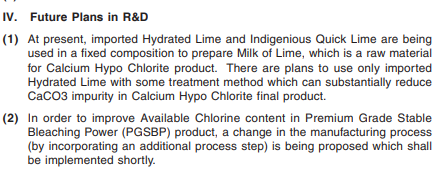

Future Plans

This quarter inventory increased by 40 crore seems they have imported Hydrated Lime but no mentions any where i could find

Red Flags

Presently company has lowest OPM since 2018…This year the plants and machinary become completely depreciated adding 50Cr every year to bottom line as mentioned by @visitkumaresh … if they get in to electrolyte manufacturing as told in AR, re-rating can happen…

Hey fellow investors.

Came across this business recently. Haven’t heard any earning calls, can anyone let me know about the recent years other investment items of 87 cr and 31 cr. Where have they invested it and any rationale being shared by them . Thanks.

The OPM of the chemical division if considered without depreciation is hovering around 10/13 percent so with a sales of around 650 cr in fy 21/22 with other income of 5 cr we can take a base of 70 to 85 cr and power generation was taking the depreciation so this year it should generate around 15/20 cr as far coal trading is concerned around 8 cr but let not consider it.

So around 85 to 110 cr earnings before interest and tax possible without trading considered at 25 percent tax rate a net profit in the range of 60 to 75 cr a base line is possible at high RM cost and frieght rates

As cash of around 180 cr and real estate investment changed to current investment at 124 cr there is approx 300 cr safety net here

At present market price that will workout to less than 3 EVEBITA at 500 cr equity we can expect around 17 to 20 percent ROE

Chemical division can grow at 8 to 10 percent power can give some standard income trading is just a opportunity

Has a good cash flow of 80/90 cr very less debt and there is a chance of real estate income as mentioned in the sept results

All we can see is at PMV it looks good and even at 5 EVEBITA IT should be valued around 750/800 cr for a price of 500/550

Last six months have seen a accumulation around 300/330 level testing bottoms of 270 and up of 380

Management is decent not very aggressive kind of conservative in expansion and no interaction with investors but a low floating stock a reasonable dividend and good csr activities has be done

Let us see how the market values but as of it seems we have safety in investment and a good scope for upside

Discl invested

I have attended two , three AGM of sh raya hypo , as it’s agm is scheduled on the same day of its sister concern TGV(rayalseema alkalies) .

My first impression is hypos management is less conservative then tgv otherwise they have not thought of venturing into real estate. Also hypo giving dividend where as tgv is using all profit in expansion .

Also inspite of being father and son relation what I observed that they didn’t attend each other AGM , even when they were held next bldg. so I think their is no interference in each other business except mutual beneficial commercial arrangement between both, like they both purchase bulk coal and import as it’s cost beneficial.

Disc not invested in hypo, just min shares for agm purpose.

Invested in rayalseema (TGV sraac)