It’s in a difficult sector…quarterly eps going down…Are the restaurants that great ?

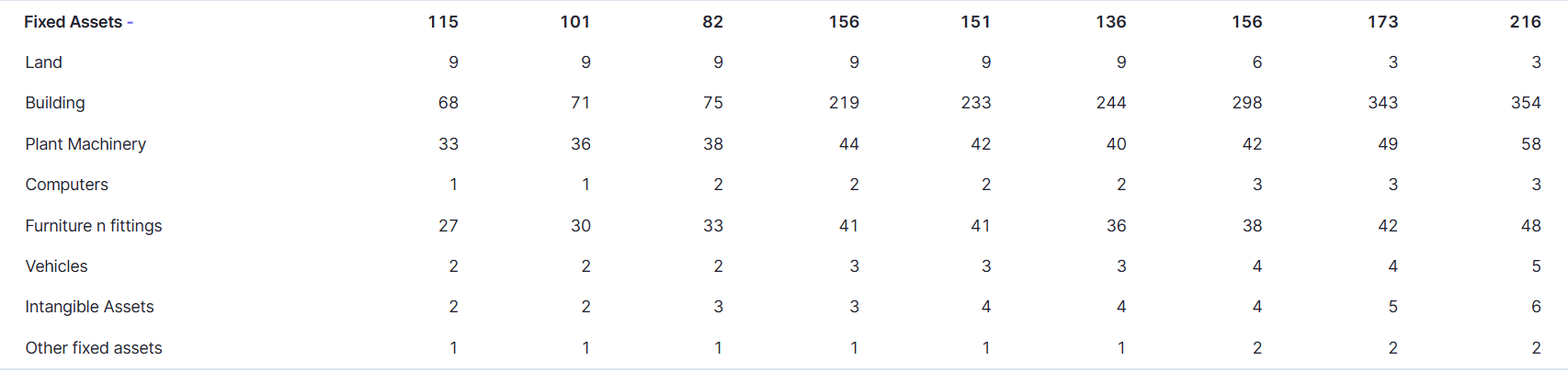

Why is the Fixed Assets on Screener not adding up?

The total is shown as 216 Cr, but their building itself is shown as 354 Cr, what am I missing?

The accumulated depreciation is provided for, after adjusting you get this number.

SRL is a rare microcap with a combination of Cash rich,passionate promoter and Low cost Innovator.

1.Diamond of Dining Industry

Speciality Restaurants Limited, an Indian hospitality company, was founded in 1992 by Anjan Chatterjee in Mumbai with its first outlet, “Only Fish,” focusing on seafood. In 1994, it expanded by launching flagship brands like “Oh! Calcutta” (Bengali cuisine) and “Mainland China” (Chinese), standardizing recipes for authentic global and regional flavors. The company grew rapidly, adding brands such as Sigree Global Grill, Haka, and Hoppipola, while entering confectionery with Sweet Bengal. Incorporated formally in 1999 as a private entity, it went public in 2012 via an IPO on BSE and NSE, listing as Speciality Restaurants Limited. Today, it operates over 124 outlets (73 restaurants, 40 confectioneries, and 11 cloud kitchens) across 11 Indian cities, plus locations in UAE, Oman, and London, emphasizing fine and casual dining with eight award-winning cuisines.

Survival rate of Dining and QSR

| Years | Fine Dining | QSR |

|---|---|---|

| 1 year | 30-40% | 50-60% |

| 2 years | 25-35% | 45-55% |

| 5 years | 15-25% | 30-40% |

| 10 years | 10-15% | 20-30% |

| 30 years | 3% | 5-10% |

The restaurant industry is notoriously challenging, with high failure rates driven by factors like operational costs, competition, and economic shifts. Fine dining establishments often face steeper declines due to higher overheads (e.g., premium ingredients, staffing, and ambiance).Specility Restaurants is among the 3% of top companies and ready for the next leg of growth.

2.Passionate leaders - Anjan chattergee is first generation leader.He founded the speciality restaurants in 1992.Expanded the company’s flagship brands Mainland China and Oh calcutta to multicities.

His son avik chattergee is inducted into management in 2018.Since then company started earning profits.He brought in the concept of Kitchen within Kitchen ,asset sweating,cloud kitchen concepts to improve Sales per assets.He is heading of innovation of new formats.He is given old furniture and minimal capital to create new formats.He introduced hoppipola,gong ,bizzare asia and walters burger etc.It shows that management is looking to create new brand which can take the business to next level.

SRL FILED FOLLOWING NAMES WITH IP INDIA

| brand | appl date | journal date |

|---|---|---|

| zariyaki | 20.06.24 | 22.09.25 |

| walters | 05.09.24 | |

| kolroll | 03.06.24 | 12.05.25 |

| kol roll co | 04.06.24 | 19.05.25 |

| kolkati | 04.06.24 | 19.05.25 |

| calkati | 04.06.24 | 19.05.25 |

| desi rolls | 27.12.22 | 17.03.25 |

| Tarratza by Mezzuna | 20.02.24 | 13.01.25 |

| siciliana by Mezzuna | 25.08.25 | |

| chary | 25.03.23 | 16.09.24 |

| chatto rheo | 23.10.23 | 23.09.24 |

| wah wah roll | 27.12.22 | 02.09.24 |

| spicy chick | 14.06.20 | 19.08.24 |

| stay hungry | 09.10.17 | 12.08.24 |

They are trying to enter several segments like rolls and chats especially.There is no panindia rolls and chats brands. It shows that SRL is trying for brands in new segments.

3.Agile Management

Company’s flagship brand is Mainland China.Its established in 1995.But people’s preference are moving towards asian cuisines.Company realised it and created Asia Kitchen by Mainland China and upgrading the existing mainland china also to Asia Kitchen.Management is recognizing the loss making outlets and closing them.

4.Cash Rich Company

Despite GST implementation 2017 ,Ban of bars nearby highways in 2018 and pandemic in 2020-21,The company is debt free and cash rich.It shows their resilience.

Company is holding 163 Crores cash as on Q1 FY 2026.It can support all future expansions with existing cash generation from business and may even try for acquisitions existing cash.Company’s market cap is 650 crores.There are hardly any companies with this much cash levels in microcap.

5.First QSR Brand - Walters Burger

| Industry | Growth rate from 2015-25 in CAGR % | Capex per store | Rental Space in Sqft |

|---|---|---|---|

| Fine Dining | 13 - 15% | Rs.2 to 3 Crores | 2000 to 3000 |

| Burger | 18 - 20% | Rs.2.5 crores | 1000 to 2000 |

| QSR | 20 - 22% | Rs.2.5 crores | 1000 to 1500 |

| Gourmet Burger | 22 - 25% | Rs.1 Crore | Around 1000 |

| Walters Burger | Rs.20 to 50 Lakhs | 500 - 600 |

Avik Chatterjee realised the importance of gourmet QSR future growth with less space utilization and asset light model.He started Walters Burgers.

Walters as the “first of many” asset-light, high-ROCE formats; the repeatable “kitchen-within-kitchen” + small-footprint + delivery-first model;

Walters is an one hand Burger with smooth potato Bun.It came up with mess free and innovative burgers.Its an Gourmet Burger.He started it in a 500 to 600 square feet which keeps the rent limited.Its established in Sept 2024.Walters is having 6 stores currently with 5 in mumbai and 1 in Pune(Recently started).

It’s using 4 outlets from their mainland china and asia kitchen units as Delivery points and 2 from physical stores.He used the Kitchen within Kitchen concept which reduces costs almost 40 to 50% like rent, electricity expenses,staff expenses etc.

Company is having 14 delivery points in Mumbai,10 in Bangalore and Chennai,6 in Kolkata and 4 in Pune in the form of Mainland China and Asia Kitchen.It covers almost 8 crore population and almost covers 90% population of each city.Without much Capex,it can expand Walters Burger in these five cities.

There are 1200 burger outlets with 25 burger chains in mumbai.However there are 4 to 5 in gourmet burger chains.Despite it’s premium costs,it’s having 4.3 to 4.5 ratings in zomato.There are hardly 25 outlets above 4.3 in mumbai among 1200 outlets.

It shows that it’s definitely a growth driver for SRL in the next 10 years.

5.Future Growth Engines

The company is planning to open 25 outlets in the next 3 years like Asian Kitchen and Gong in Fine Dining.

Asia Kitchen is designated as the growth engine number 1 for the company, and its expansion is considered key to future growth. The company’s overall strategy continues to focus on dominating the Oriental/Asian segment of the market, with Mainland China serving as the anchor brand and Asia Kitchen driving the new growth.It was created as a brand refresh or new avatar of the flagship brand, Mainland China.The creation of Asia Kitchen was driven by the need to renovate and reinvent the company’s offerings due to the changing ecosystem and consumer desire for innovation and vibe.

Asia Kitchen expands beyond Mainland China’s core Chinese offerings. Its menu is approximately 50% Chinese cuisine (the best offerings from Mainland China) and 50% new offerings in Pan-Asian cuisine

Gong is generating 8.5 crores of income per store whereas SRL’s per store income 3.6 crores.It nerates higher revenues due to increased sales from its liquor offerings.

The brand GONG is identified as a successful innovation and a key component of the company’s focus on the Oriental (Asian) cuisine segment.The brand is considered youth-oriented and caters to a younger audience.

Walters Burger is going to use these outlets also in future with Kitchen within Kitchen to grow rapidly.

- Efficiency

| Report Date | Mar-15 | Mar-16 | Mar-17 | Mar-18 | Mar-19 | Mar-20 | Mar-21 | Mar-22 | Mar-23 | Mar-24 | Mar-25 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 299 | 321 | 312 | 297 | 346 | 358 | 150 | 253 | 375 | 405 | 436 |

| Sales per store | 2.60 | 2.61 | 2.54 | 2.32 | 2.70 | 2.56 | 1.28 | 2.16 | 2.95 | 3.21 | 3.60 |

Sales per store from 2021 to 2025 is 1.28 to 3.60 crores.Despite pandemic and closure of stores, company’s sales and sales per store are increased from 2021 to 2025 with KWiK,asset sweating.It shows the management’s efficiency.

There are negatives also.They are unable to expand their flagship brands to Pan India.Walters burger is their 17th brand.They couldn’t succeed in expansion of all their other formats except Mainland China,Oh! Calcutta and Sweet bengal.

Overall,SRL is not just surviving in the Brutal industry for the past 33 years but its inventing new formats at lower cost and reinventing existing brands. They may come up with more innovations in the future as per IP data.Success of any of their brands would take SRL to new heights.

3 Likes

what could be the reason they raised money when they had enough cash already?

Supposed to do inorganic growth, but never materialised

They announced it live on tv channel, didn’t happen.

They announced onboarding of some professional as CEO, that too didn’t happen.

1 Like

Why so many formats of restaurant many with insignificant turnover and huge capital costs ?

1 Like

At 110 if it gets correct further, the stock should trade at 5.5x FY26 expected post IND AS EBITDA of Rs 100 CR. Post Pandemic, on normalising, avg EV/EBITDA is in the range of 9.0-9.5x. Expected turnaround in discretionary spends towards CDR/QSR, mid-single digit SSSG, 10-12% overall top-line growth driven by 8-10 openings in legacy formats along with post IND AS margin stabilising around 23-25% should re-rate the stock towards its 5-yr avg. Demerging of unutilised land parcels into separate vehicle eliminated the overhang to some extent. Rs 170 Cr of cash on books should get deployed into core restaurant business only. If they get a new CEO soon from a healthy background, it could trigger the rerating. This is not a play on valuation catch up with listed QSRs. CDR player will always trade at a discount to QSR given the nature of business. Rather, it’s a ‘valuation normalisation on mean reversion in business environment + execution’ play.

Disclosure - not invested but will enter at 110 levels to achieve further margin of safety.

1 Like

I had asked on concall on multibrand stratergy.

1)Mgmt said they dont intend to diversify and expand in all branded CDR/QSR they have experimented in.

But they wont be closing the profitable outlets.

-

Asian and Indian Chinese Cuise brands( Mainland China and Asia Kitchen), Italian format Siciiliana,Sweet Bengal they would focus and try to grow.

QSR- format- Walter Burger seems to be the experiment they would try and grow. -

I very categorically asked if they henceforthe wont experiment and de-WORSIFY , rather consolidate and drive business with focused efforts on few brand.To it managment acknowledge it positively

1 Like