"We hereby inform that Joby M C, joint general manager, head of inspection and vigilance department and Head of internal audit and chief of internal vigilance and key managerial personnel of the bank is retiring from the service of the Bank. The Board of Directors of the bank has appointed Nandakumar G, general manager as head of inspection and vigilance department and head of internal audit and chief of internal vigilance of the bank with effect from 1st June 2023”.

- South Indian Bank’s share price has surged after experiencing double-digit growth in its gross advances during the first quarter.

- The bank’s strong performance in expanding its loan portfolio has attracted investor attention.

- The rise in the bank’s share price reflects positive market sentiment towards its growth prospects.

5 Likes

From the above link,

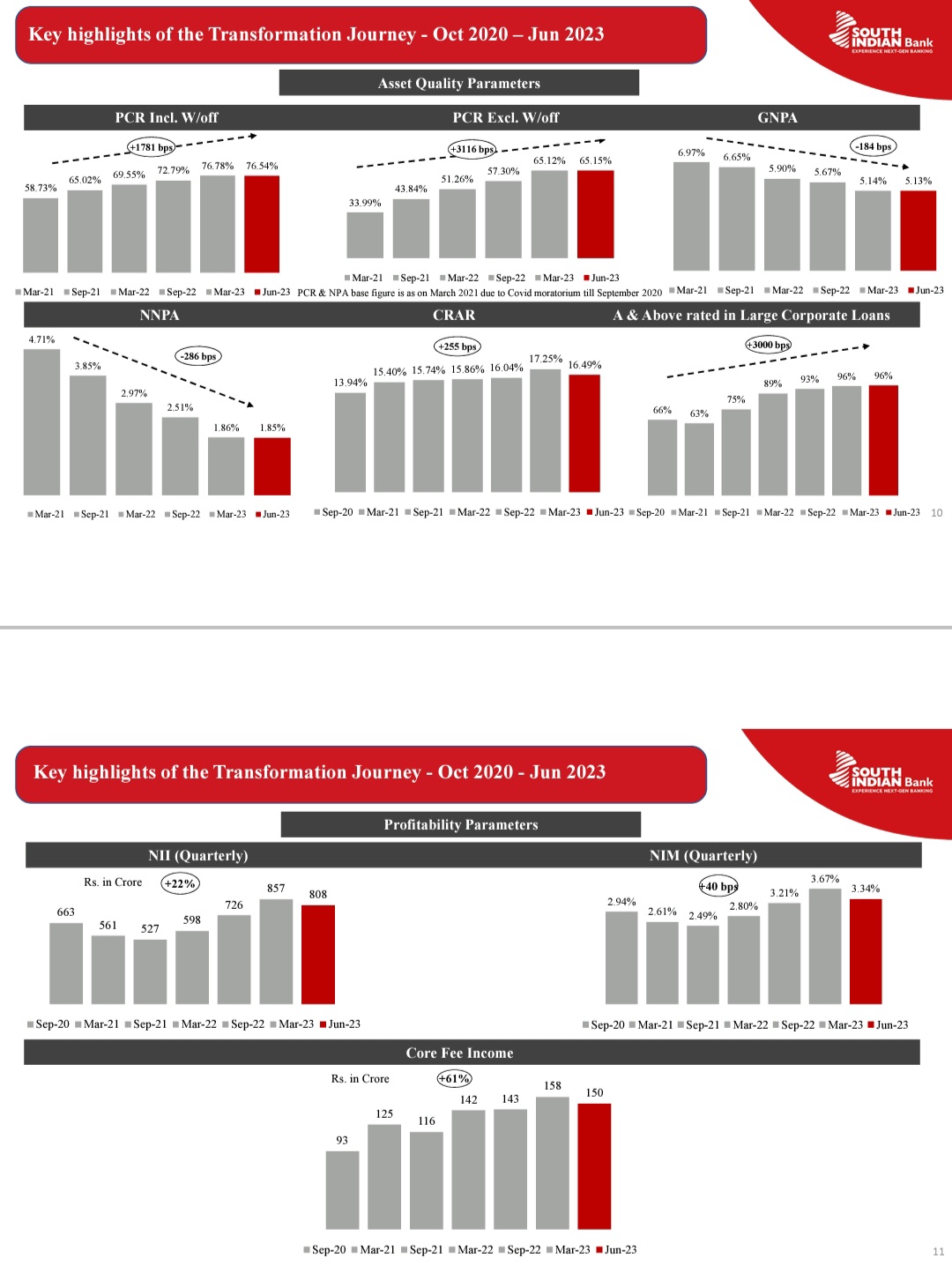

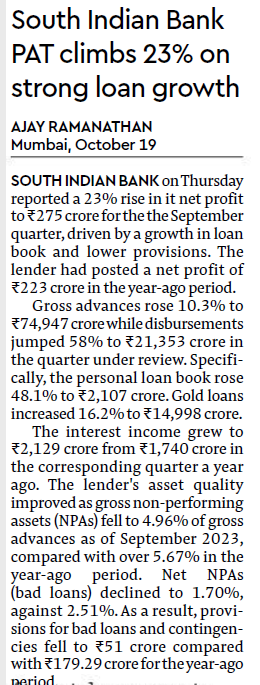

The lender reported that its gross non-performing asset (GNPA) came down by 74 bps from 5.87 per cent to 5.14 per cent on Y-o-Y basis. The net NPA (NNPA) of the lender for the quarter stood at 1.85 per cent, which was down from 1.86 per cent on a year-on-year basis.

Other than that all other parameters look good.

Other highlights of the report are:

NIM improved by 60 bps from 2.74% to 3.34% on Y-o-Y basis

Return on Equity improved by 412 bps from 7.68% to 11.80% Y-o-Y basis

Return on Assets increased by 27 bps from 0.46% to 0.73% Y-o-Y basis

Recovery and upgradation in NPA accounts increased from Rs. 296.23 Cr in Q1 FY23 to Rs.

361.71 Cr in Q1 FY24

Why is the Market reacting brutally to the stock price? Am I missing something?

Dears,

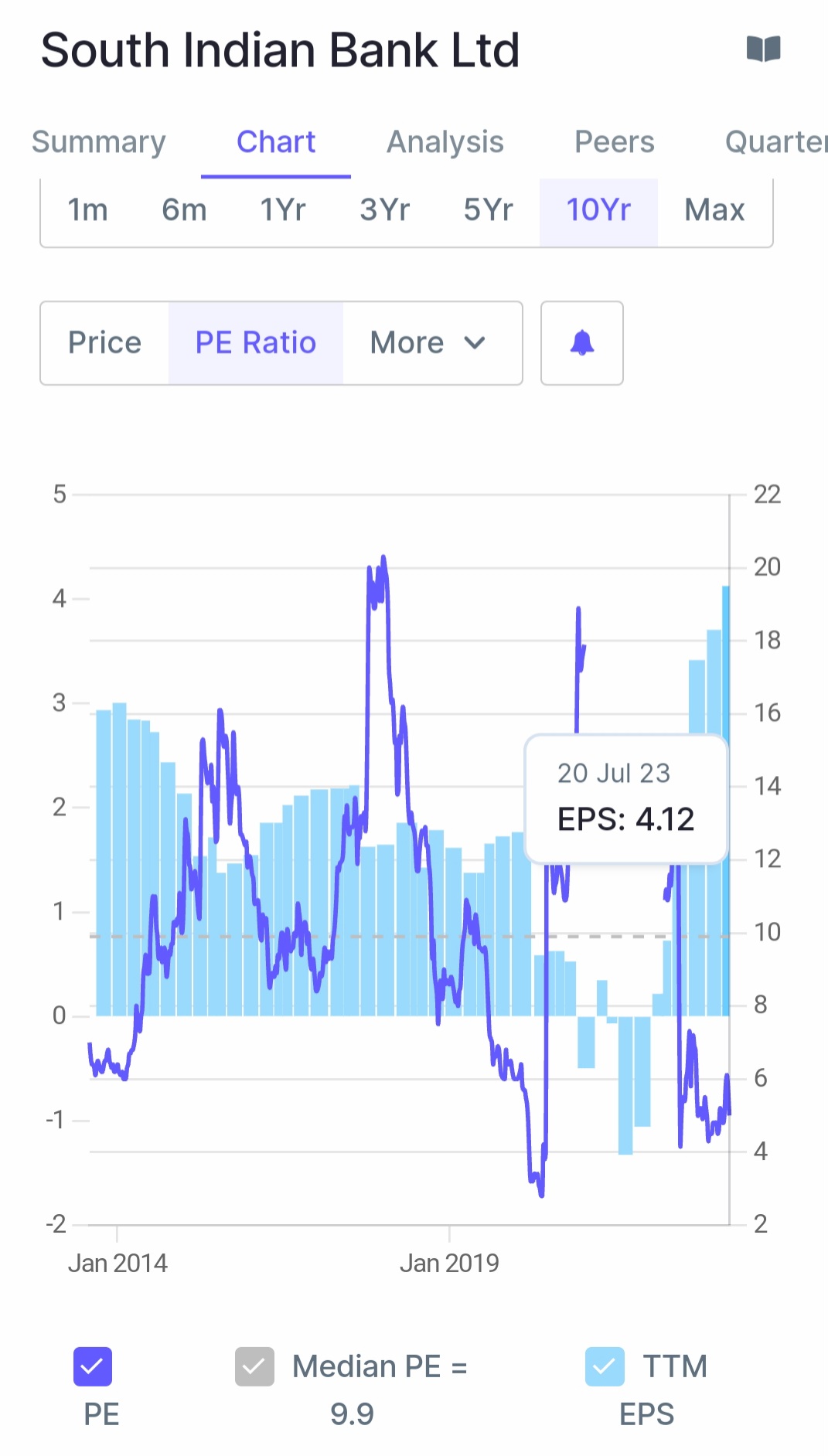

#southindianbank , this is just quick profit booking and its temporary as usual Though result is shown little week against Q4 2023 however overall mumbers are really impressive. It still under valued, see below historical charts sbaps of SIB price, PE ,EPS and opearing performance.

Its not any recommendation but i belive its still has excellent opportunities to grow.

1 Like

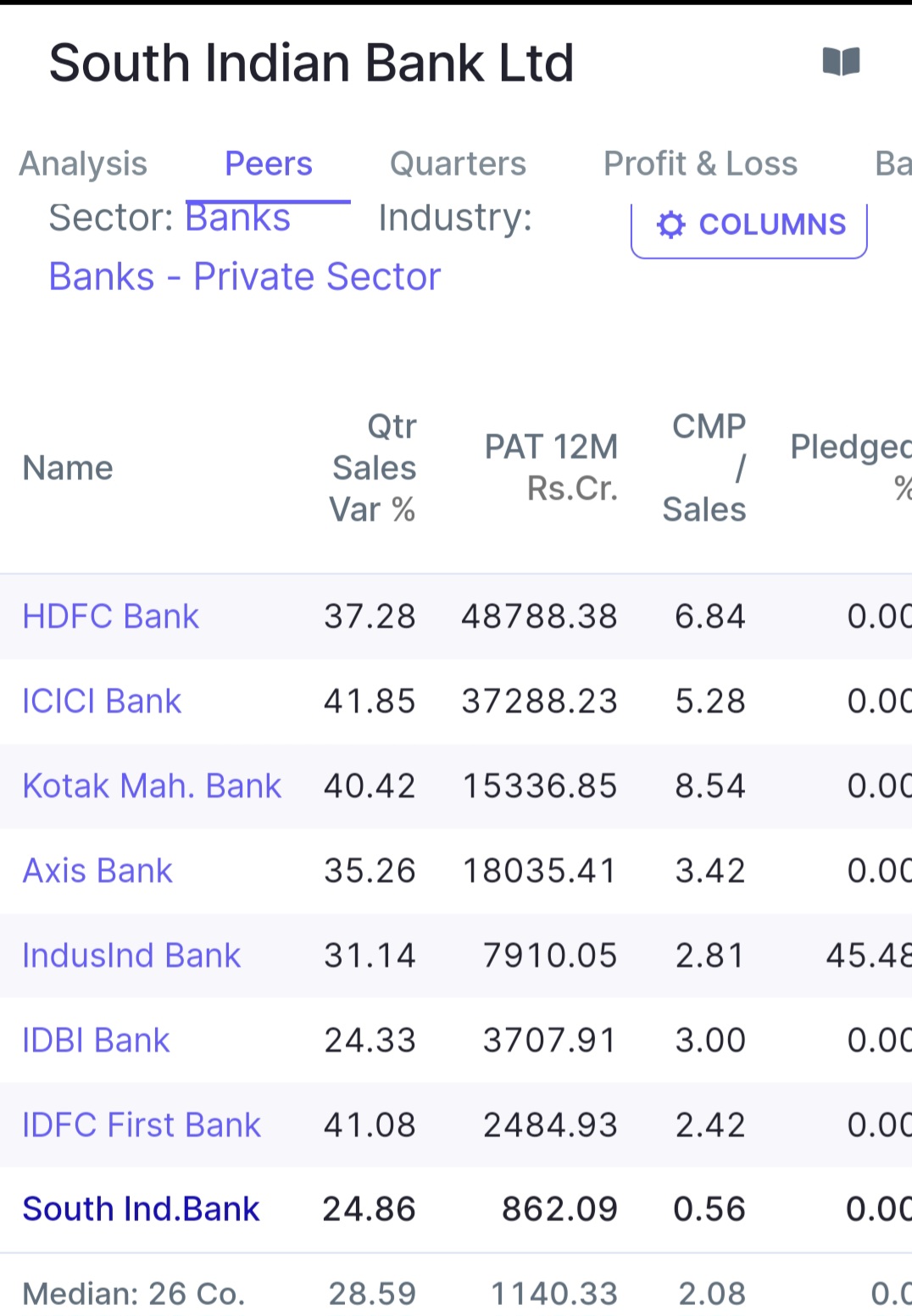

Banks are usually evaluated on PB basis not on PE

3 Likes

The Bank reported a significant rise in net profit by 75% in Q1, enabling them to explore good corporate deals based on liquidity and profitability. The bank plans to focus on credit growth of 12-13% for the fiscal year 2023-2024, targeting a CD ratio of 75-77%. Their strategy emphasizes profitability through quality credit growth.

The bank’s CASA growth has moderated in Q1 due to the rising interest rate scenario, with customers shifting funds to term deposits seeking higher interest rates. However, they expect this trend to reverse in the second half of the financial year when rate hikes are paused, and liquidity eases in the market.

Regarding unsecured advances, the RBI has tightened norms due to the increasing risks of default. The South Indian Bank has implemented stringent measures to mitigate risk, including credit checks, data analytics, and pre-approved personal and credit card loans. Their total unsecured loan book is within ₹3,000 crore, and they continuously monitor their portfolios to keep delinquency levels in check.

3 Likes

Any insights from people who have been studying this sector on how this bank holds up in comparison with Karnataka bank / CSB bank?

RBI approved a new CEO for South Indian Bank. I guess it’s old news. He was previously employed with Karur Vysya Bank at one point. However, he resigned from KVB due to personal reasons 5 months before his term ended. I hope he is an able administrator and CEO like the outgoing CEO seems to have been. What has been a constant in South Indian Bank seems to be the chairman. Let’s hope the chairman and the board have done a good job picking the new MD and CEO.

Disclosure: Invested

1 Like

-

South Indian Bank stock has rallied 180% in a year and 200% over three years, gaining 15% year-to-date.

South Indian Bank stock has rallied 180% in a year and 200% over three years, gaining 15% year-to-date. -

ICICI Securities gives the stock a ‘Buy’ rating with a revised target price of Rs 28, citing a 27% potential upside.

ICICI Securities gives the stock a ‘Buy’ rating with a revised target price of Rs 28, citing a 27% potential upside. -

RBI approves PR Seshadri as MD and CEO, seen as a positive move by analysts.

RBI approves PR Seshadri as MD and CEO, seen as a positive move by analysts. -

South Indian Bank’s Q1 2023 financials show a 75% increase in net profit and reduced NPAs.

South Indian Bank’s Q1 2023 financials show a 75% increase in net profit and reduced NPAs. -

Net interest income surged 33.87% to Rs 807.77 crore in Q1 2023.

Net interest income surged 33.87% to Rs 807.77 crore in Q1 2023. -

Operating profit in Q1 2023 rose 54.74% to Rs 490.24 crore.

Operating profit in Q1 2023 rose 54.74% to Rs 490.24 crore.

2 Likes

I have been tracking this company for a while and remained invested for the past year. But post this Q2FY24 result and call, I have exited as there are concerns that are not comforting like:

-

Ex-MD Murli had made a huge transformation in SIB, but deviated from the original agenda to grow the personal, MSME Loan segment. Business + Personal Loan formed 55% of Loan Book Mix as of Q1FY21, which stands at 43.7%.

-

He wanted to de-grow the Corporate Book which he initially did from 30.5% of the Loan Book to 24.5% of the Loan Book till Q1FY22, but due to the market environment, he started giving back High Quality Corporate Loans with A-rating. This led to an increase in Corporate Loan Book to 36.7% as of today. Although the quality of loans has tremendously improved from 70% of the total corporate loan under A-rating to 96% of the total corporate loan under A-rating.

-

What is more disappointing is, all this corporate lending has been very short-term. In H1FY24 so far, he has disbursed 43k Cr. but managed to grow the loan book only from 72k to 74k in two quarters. The loan book did not increase v/s disbursement because the new corporate book which was short-term was churned basically. So, now another round of short-term loan disbursement is given? and upon all these the larger scheme of growing retail books has vanished?

-

Now, the new MD Mr. P R Seshadri has again reiterated to grow MSME loans. But, it will take a lot of time to grow and reduce the short-term loan book of corporate. If the disbursement is too fast in MSME to quickly turn around the loan book mix, the riskiness will be higher if not underwritten well. In fact, since FY21 the Business Loan mix & absolute size have reduced but segments GNPA have increased from 10.2% to 14%. This means the corporate loan book will remain in the mix for some time.

-

30% of the liability franchise is pending for repricing. Along with this, the new churned book will be at very competitive rates if I assume. There can be temporary stress on NIMs/Spread.

-

And, the legacy loan book is reducing. New Loan book since 2020 now forms 64% of the overall book. And that too most of it being A-rated corporates. It is very obvious that GNPA and NNPA will fall. I feel it was more of an illusion that GNPA has been reducing, rather it should be obvious that it has to reduce.

-

And lastly, the new MD is just 3 weeks old and did not confidently answer the questions on call (as per my basic understanding). He wanted to have more time at SIB before commenting.

All these reasons were urging me to take an exit, and I wanted to have more clarity on the progress at SIB. Things over the past 2 years have changed a lot in this Bank. And transformation led by the ex-MD was just superb, but currently, things are not so clear.

I am just learning and have listed down things from my perspective. I request members following this company to post views on the same.

Regards,

Mukul Jain

Exited post Q2FY24 call.

12 Likes

SIB has announced a rights issue for 1750 cr, which I think is a good move considering its trading below book value.

I am also holding Karnataka bank, which is also is being transformed under new CEO, fingers crossed

Holding since 6 months

3 Likes

5 Likes

q3 concall notes and update attached

q3 fy24 update sib.pdf (5.0 MB)

4 Likes

The one concern I have is that if you look at Segment Reporting, it is clear that the results of Q3 2024 are greatly improved due to treasury income. In fact Corporate segment is showing a loss partly due to write off of 28crs of fraud

3 Likes

Quick notes from SIB concall:

- Cost of funds → continue to rise due to deposit repricing, cost of deposit 5.18%

- Cost to income → As compared to peer, is higher; close to 62%; provided IBA rate settlement, accounted for 15%, but final settlement amount was 17% (additional Rs. 24 crore); even without this cost to income is still higher, management is looking to improve it - Looking to increase customer facing employee from 75% to 85% thus increasing branch productivity; can decrease cost to income

- CD Ratio → Currently ~78% CD ratio, deposits book grew 9% yoy; have some space to grow which can be P&L accretive

- Contraction of NIMs → NIMs currently is 3.19% on account of liabilities repricing faster than assets, squeezing the margins. Want to restructure balance sheet, have higher yielding assets.

- Will be targeting MSME and retail, in 3-4 years want to bring corporate loan book to near 30% from 38%, the 6-7% difference will be added to higher yielding assets (MSME, LAP etc.)

- Capital Raise → No decision has been taken yet

- Enhancing Portfolio Resilience → want to have more granular book

- Deposit Concentration → 62% of deposits come from Kerala

2 Likes

Very good run-up in stock after the result from Rs. 28 to Rs. 33. So, obviously results are taken up very well by the market. Below is my comment on Q3FY24 results:

-

To repeat, Since the corporate book is a shorter term with very high ratings, NIMs will continue to remain under stress until MSME loans are not grown. The share of Corporate Loan in the mix increased Q-o-Q and MSME reduced. So, a thing to watch out for.

-

Employee expenses have been a bigger issue in the last few quarters due to which C/I Ratio is increasing. Despite a marginal reduction in employees and adjustment of 24cr. one-time additional expenses in Q3FY24, the cost has grown. So, again need to see how this will be managed.

-

However, slippage numbers are well as guided. Also, GNPA, NNPA, PCR, etc. numbers along with ROA (>1% now) and ROE (>15% now) are very encouraging signs and as guided by management.

-

But we need to be again careful that this ROA/ROE are outcome of very healthy recoveries. We need to analyze ROA/ROE given that recoveries slow down going forward.

-

The major focus area is laid down to grow MSME loans and rationalize costs by management in Q3FY24 with no clear guidance as of now. However, he mentioned that we will continue to function the way the previous MD has laid and make some slight changes as we go ahead.

Conclusion:

I will keep tracking this stock till the time I get more hang on the new MD at SIB. Also, actively looking to see how MSME will grow with good underwriting standards. Currently, looking at numbers would not be in a hurry to buy as I have already taken an exit post Q2FY24 results.

No-Position Currently

Regards,

Mukul Jain

4 Likes

MF lining up too + Insurance + Guys from SG i guess too looking to diversify away from top 4 banks into PSU’ish banks like SIB.

5 Likes

Interesting to see finally Sameer Arora cracked the case !!

1 Like