I’ve been wanting to get to Snowman ever since the tax cuts were announced by the govt in this budget but have been price anchored to certain levels. Lucked out big time to see this stock drop to said levels.

List of criticisms levelled against the co:

- Hasn’t lived up to the hype in terms of reaching significant scale

- Failed sale to an indiscrimate buyer like Adani - is this so rotten that even Adani refused to buy it?

- Dead money - Stock is trading near 2014 IPO price of 47 per share and Adani’s open offer price of 44 per share in December 2019

- External CFO resignation within 5 days of appointment in 2022, replaced by someone promoted internally

- IT raids around the above event

- Disappointing growth and capacity expansion despite being proxies for hot high growth sectors - did/does the management not care

- High capital intensity, low ROE

- Seemingly high churn in key management personnel

- Despair/general lack of interest in the stock - retail shareholder count/retail holding as a % of TSO at 80% of Mar 2021 levels i.e. the levels where Adani unloaded after the failed open offer, lack of discussion in this forum since that point despite significant business developments - positive and negative

The claims seem superficial and melt away on closer examination

(I’m just trying to fit a narrative to the numbers and I do not have access to the management so I could be off(even by a lot).)

Examining the human capital aspect:

| Name |

Designation |

Appointment Start Date/Year |

Salary During Appointment Year (INR) |

End Date/Year |

Salary During End Year (INR) |

Resume |

| Ravi Kannan |

CEO & Wholetime Director |

February 15, 2007 |

12,174,916 (FY 2014-2015) |

February 2, 2016 |

77,82,930 (FY 2015-2016) |

B.Com and Masters in Computer Science, 56 years old in 2015, Previous Employer: Jeena and Company Private Limited, 20+ years experience, Designation at previous employment: Country Head, Supply Chain Division. |

| A M Sundar |

Chief Financial Officer & Company Secretary |

Not explicitly stated in 2015 |

74,18,028 (FY 2014-2015) |

July 31, 2022 |

|

|

| Kannan S |

Chief Financial Officer |

August 1, 2022 |

(FY 2022-2023) |

August 6, 2022 |

(FY 2022-2023) |

|

| Pradeep Kumar Dubey |

Wholetime Director & COO/CEO |

February 10, 2016 |

8,31,874 (FY 2015-2016) |

November 9, 2016 |

26,57,000 (FY 2016-2017) |

|

| Sunil Prabhakaran Nair |

Wholetime Director & CEO |

December 1, 2016 |

32,52,000 (FY 2016-2017) |

Currently in role |

1,80,00,000 (FY 2023-2024) |

M.Com., MBA., 46 years old in 2017, Previous Employer: Coldex Logistics Private Limited, 25 years experience in 2017, Designation at previous employment: Chief Executive Officer, 28+ years experience in 20225, 30 years experience in 2023. |

| N Balakrishna |

Chief Financial Officer |

January 24, 2023 |

(FY 2022-2023) |

Currently in role |

(FY 2023-2024) |

|

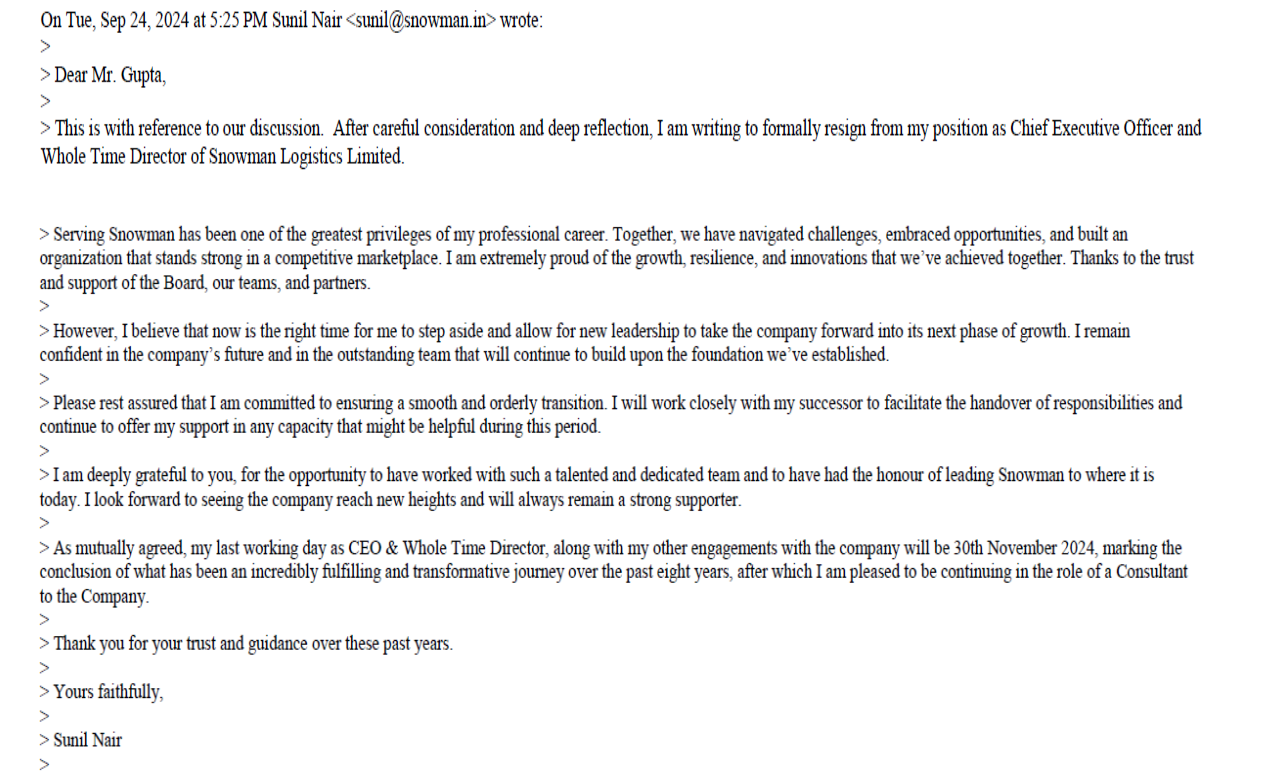

Sunil Nair has vacated his position recently and his replacement has been an internal promotion.

| FY |

Headcount (End of FY) |

YoY Headcount Growth (%) |

Median Change in Remuneration (%) |

| 2014-15 |

408 |

N/A |

2.48% |

| 2015-16 |

401 |

-1.72% |

-2.55% |

| 2016-17 |

362 |

-9.73% |

-2.55% |

| 2017-18 |

394 |

8.84% |

9.95% |

| 2018-19 |

399 |

1.27% |

6.74% |

| 2019-20 |

411 |

3.01% |

7.43% |

| 2020-21 |

424 |

3.16% |

0.00% |

| 2021-22 |

451 |

6.37% |

6.36% |

| 2022-23 |

480 |

6.43% |

17.00% |

| 2023-24 |

507 |

5.63% |

4.00% |

Takeaways:

It appears as though a growth-oriented CEO was hired before/during IPO after which the economic slowdown led to him no longer being suited for the role. Headcount rationalisation took place around that period.

Under Sunil Nair, the company’s performance hadn’t picked up meaningfully(same for shareholder returns). However, he continued to line his pockets significantly

Sunil Nair’s resignation letter sounds like a firing/mutual parting of ways

The 5-day CFO isn’t a red flag since

a. the person had been defacto CFO for months before officially taking over

b. he hasn’t taken up another job post the resignation so this isn’t a poor reflection of the company

[CFO’s LinkedIn]

He was succeeding a tenured CFO who had retired.

There doesn’t seem to be any major alarms in the financials either:

no shady related party txns, no egregious salaries, no old receivables or large provisions/writeoffs historically. No alarming cont liab. Can’t find counts of fraud too

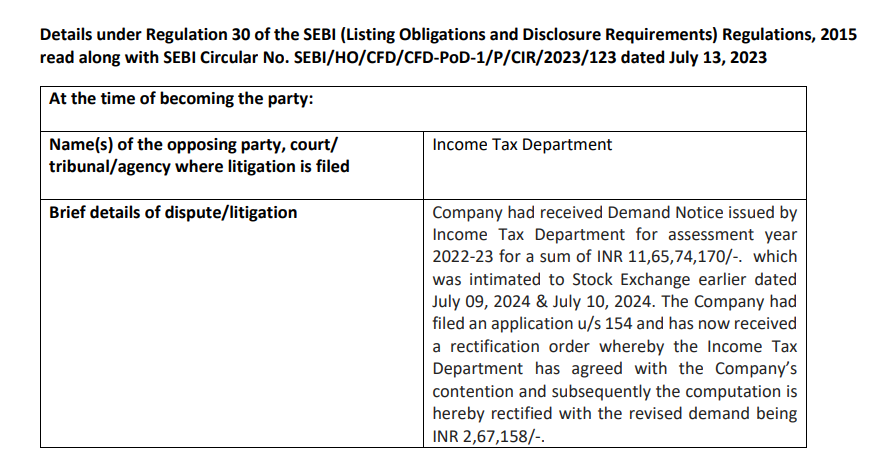

The IT raid in 2022 didn’t amount to anything meaningful

auditor expense spiked in FY22-24 from 17 to 34 to 43 but that is due to the newly added 5PL biz

So, overall, The organisation just seems to have been stuck in mediocrity with apathetic management during this period from 2016-2022. The blame entirely isn’t on them though

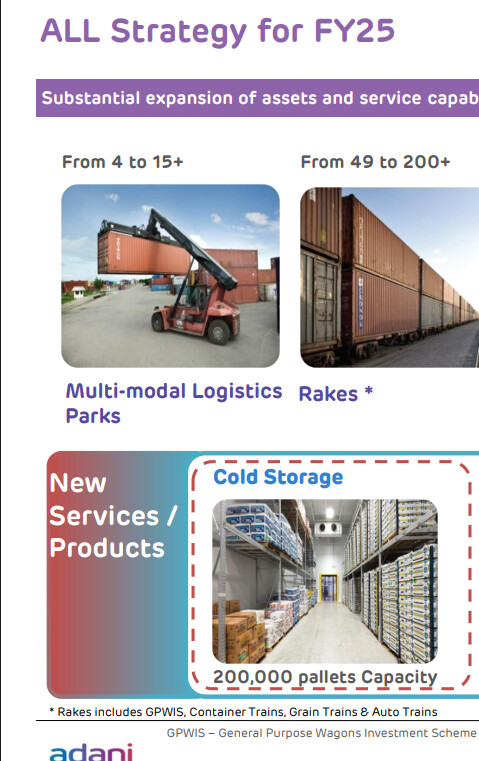

Adani Ports’ presentation on Snowman’s acquisition is very revealing and indicative of the same.

Business developments:

The failed sale to Adani seems to be due to covid related uncertainties since the fit seemed to be pretty good for Adani.,

Business growth has been subdued

| FY |

Pallet Capacity |

YoY Growth in Capacity (%) |

Capacity Utilisation (%) |

| 2014-15 |

85,500 |

N/A |

92% (as of March 2015) |

| 2015-16 |

98,500 |

15.21% |

74% |

| 2016-17 |

103,600 |

5.18% |

64% |

| 2017-18 |

106,964 |

3.25% |

72% |

| 2018-19 |

104,343 |

-2.45% |

86% |

| 2019-20 |

105,228 |

0.85% |

Data not available |

| 2020-21 |

107,450 |

2.11% |

Data not available |

| 2021-22 |

117,526 |

9.38% |

89% |

| 2022-23 |

135,552 |

15.34% |

89% |

| 2023-24 |

141,405 |

4.32% |

91% |

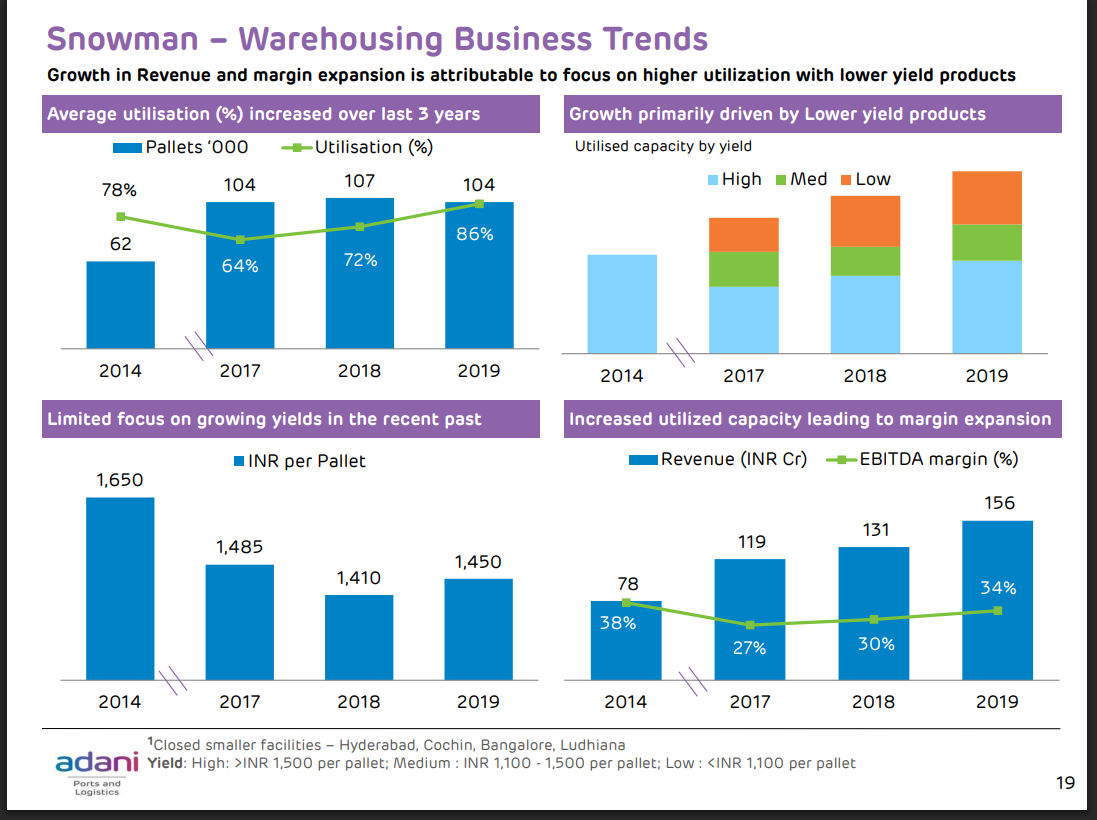

Capacity addition and growth has been pretty abysmal. So has the revenue per pallet

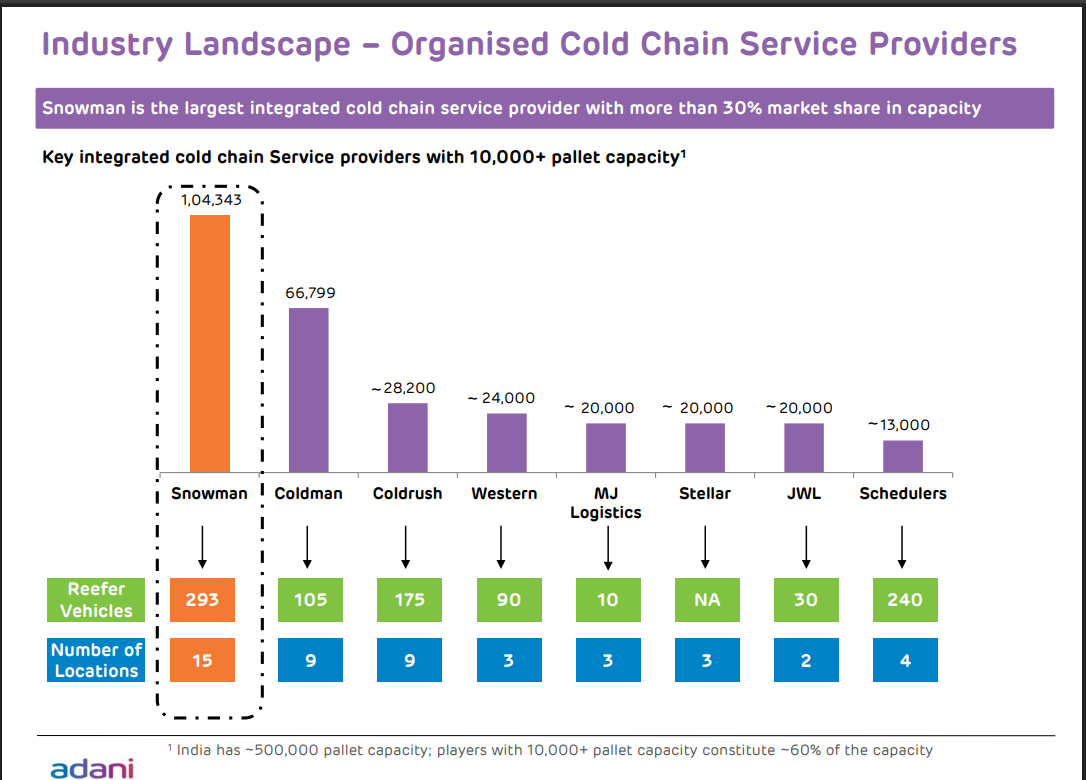

Current 141k capacity is short of Adani’s targeted 200k

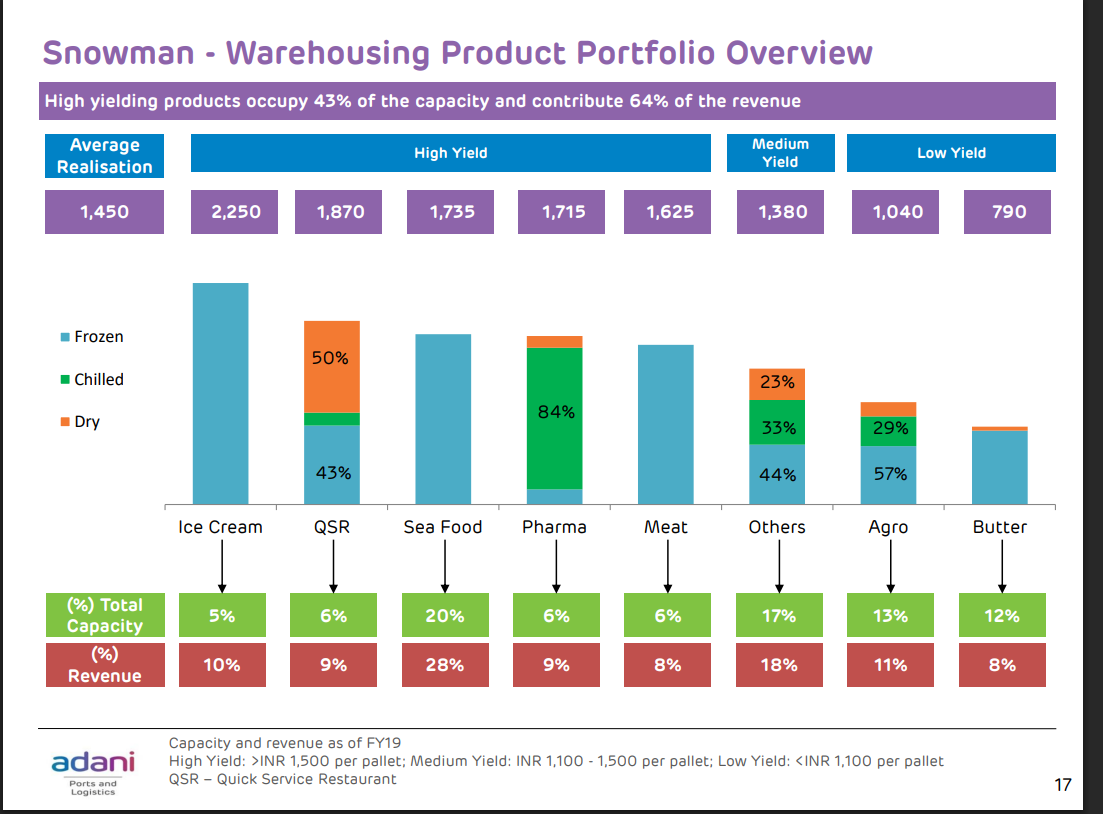

Snowman’s business mix has been underwhelming leading to lower yields

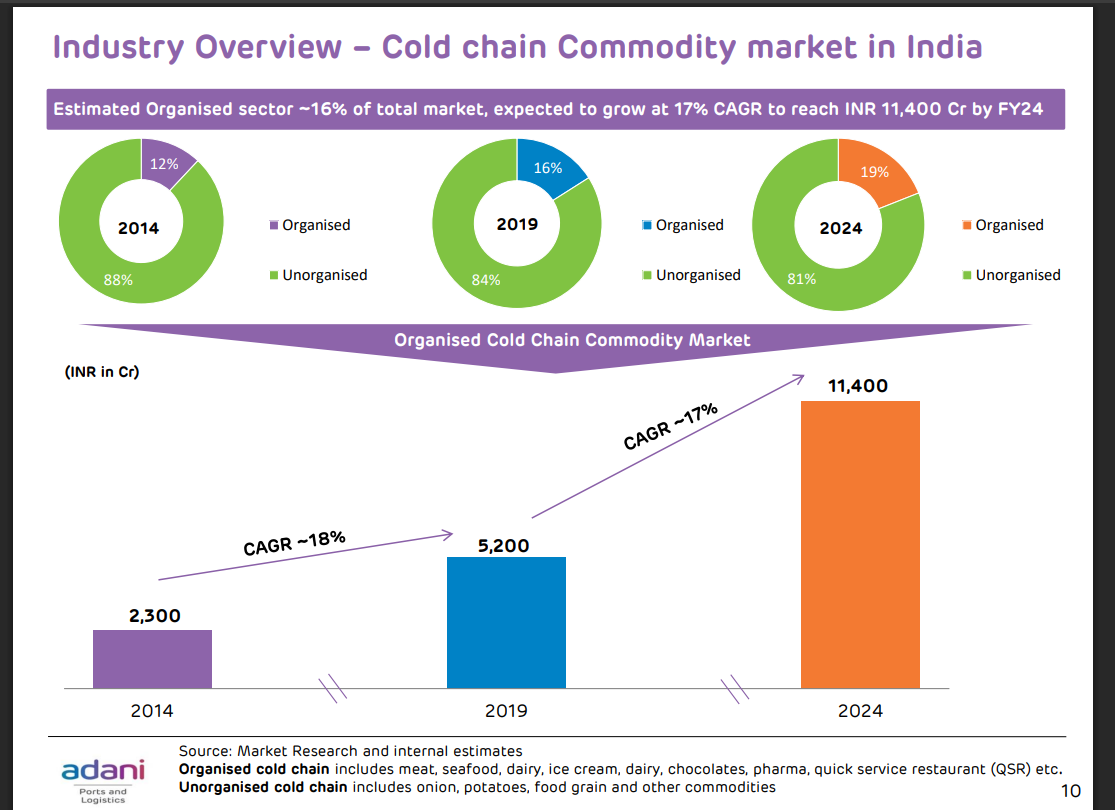

But the market itself was pretty small

with Snowman holding their market share till now

Management claimms that online retail demand is volatile so it could lead to oversupply in warehouse capacity if the expansion is not done in a calibrated fashion.

While Snowman grew capacity from 104k to 141k, the second largest player Coldman expanded capacity at a much slower pace from 66k to 85k pallets

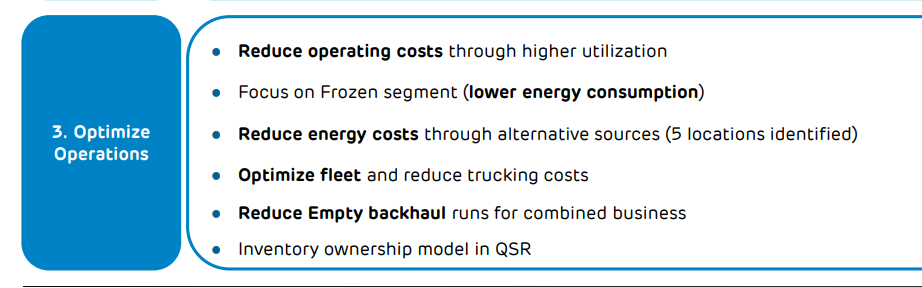

Some of the cost optimisation strategies like reducing empty backhaul runs could naturally happen as the scale increases

Things have been slowly getting better.

- Yield during Q1FY23 was INR 1521, which is higher than that of 2017

- Utilisation has been consistently higher

- Transportation division turned and has stayed profitable since FY23(partly due to 5PL)

- shift to a less upfront capital intensive model

From FY24 AR: opened an advanced multi temperature-controlled facility in Guwahati, Assam. This facility, our first fully leased cold storage unit, has a capacity of 5,152 pallets, bringing our total pallet capacity to 1,41,405 and reinforcing our shift towards an asset-light model

- India’s percapita income inching up over the years led to brands wanting to enter India(along with the ecom/qcom boom) and requesting end-to-end solutions from players like Snowman (this demand has been mentioned in coldman’s credit reports too) etc

So, Snowman Logistics has introduced a Fifth-Party Logistics (5PL) business division, This makes them the first Indian company to offer 5PL services in the cold chain logistics and supply chain management sector.

Business Models:

- Snowman’s 5PL services operate under the brand SnowDistribute

It provides comprehensive end-to-end supply chain management solutions, optimizing efficiency and reducing costs for clients

This includes services from sourcing to distribution, covering vendor development, quality audits, inventory procurement, and selling to potential customers as a sourcing partner23.

SnowDistribute leverages technologies to drive highly efficient networks, guaranteeing the best optimization of every step of the supply chain

It involves sourcing services and securing the best contracts for client companies

Snowman takes on more responsibilities from the customer’s supply chain team.

The gross margin for the 5PL business is expected to be around 10%, with a net margin of around 4% to 5%

The business model aims to optimize warehousing and transport resources

It involves back-to-back arrangements where procurement is done against customer projections, mitigating the risk of over-inventory and expiry in food products.

Target Customers:

- The initial focus is on e-commerce companies with no physical store space.

Snowman is also targeting existing 3PL customers to transition them to 5PL services

New brands and Quick Service Restaurants (QSRs) entering India are a significant target, as Snowman can offer them a full package of cold storage and distribution

Examples of current 5PL clients include IKEA, Baskin Robbins, and Tim Hortons

The company is engaging with potential customers who value the value-add offered by this model

Future Prospects:

- Snowman views the 5PL division as having huge potential and expects it to become one of its biggest segments in the coming years

The company anticipates a significant revenue growth (around 15% to 20%) due to the addition of the 5PL business

The scalability of this opportunity is considered very big, as Snowman is indirectly becoming a complete food service distribution company, following a model similar to Sysco Corp

The growth will come from increasing the basket of supplies for existing 5PL customers, adding new locations for these customers, and onboarding new clients

Snowman aims to leverage its existing 3PL customer base and convert them to 5PL arrangements

The company expects to grow along with new chains entering India, offering them a full package of services

The increasing share of the 5PL business is expected to significantly improve Snowman’s Return on Capital Employed (ROCE) due to the low capital deployment (primarily working capital for inventory)

Snowman foresees its transition from a pure warehousing and transportation company to a food services or food distribution company in the future

The company aims to continue focusing on SnowLink for deeper integration with customers by offering most distribution solutions

Snowman anticipates reaching a revenue of Rs. 800 crores to Rs. 900 crores by the end of FY27, primarily driven by the SnowDistribute (5PL) business

Competitive Advantage:

- Snowman is the first company in India to introduce 5PL in the cold chain logistics and SCM sector, giving them a first-mover advantage

They offer a single platform for a full range of services, unlike pure cold chain suppliers or distributors

Their existing large client base in 3PL provides a readily available market for 5PL services

Some of their existing clients are suppliers to other clients within Snowman’s network, creating a unique synergy

Snowman’s strong foundation in warehousing and transportation forms the base for the additional 5PL services

Their ability to offer an integrated solution is a key differentiator, especially for new market entrants who would already be speaking to them for cold storage

Snowman’s 5PL offering provides better integration and allows clients to offload more responsibilities from their supply chain teams

This has become a growth driver and the promoters started buying 5% of the company in FY23 and FY24(and haven’t ruled out further acquisition)

Cost basis for this acquisition is 55.47 per share with the last buy at 75.4

The income tax cuts in the current Union Budget can only supercharge the growth. QSRs have posted strong updates/recovery this quarter making this the most opportune moment to enter and participate in one of the most attractive proxies to the percapita income story

5PL seems to have attracted famous fund managers like Kenneth Andrade(via MIT) and Shyam Sekhar of ithoughtpms(the latter has doubled down in the March 2025 quarter, probably post budget announcement)

The snow seems to have cleared out; clearer road ahead?

Disc:

invested, pushback invited

assisted by AI. There might be a couple of minor factually incorrect numbers I might have overlooked while verifying. Kindly DYODD. NFA