Yes, it appears to be so. That is why they sold recently to preferential investors.

I have learnt a big lesson in my investment journey. Always be wary of any kind of hype being created about any stock/ sector. Invariably it is a precursor to negative reaction, rarely positive.

Having said that, personally I am positive on SKY. Because gold demand is always there in India. And the company has a relatively safer business model.

3 Likes

Pace of sales growth goes down in q1 fy26 it does 56℅yoy so it is note so lucrative as earlier

Investor presentation for the quarter

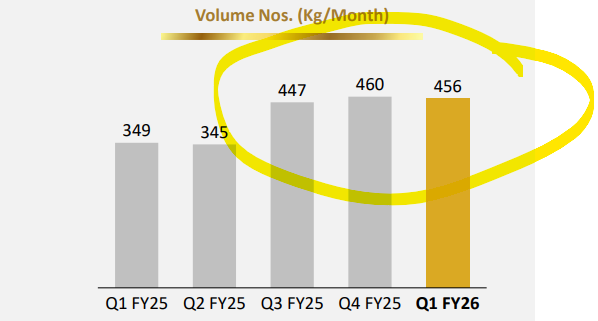

Volumes are flat for 3 Qtrs…no wonder, 2 back2back LCs..at these valuations, the expectation is that Q on Q too has to be pristine, without a single wrinkle…about 6.9% Rev growth Q on Q and 35basis points in EBITDA is not going to delight these markets

have to execute well but it is the EBITDA margin improvement that will eventually get it going in market

PS - holding and no new transaction in recent times…and cringing

1 Like

As proportion of sales from Advance gold increase - that impacts gold volume - leading to flat qoq. That is getting reflected in gross margin.

5 Likes

Just sharing two interesting videos after the latest results.

Just sharing.

Not invested.

dr.vikas

1 Like

At the price gold has been in past 3 months, no sane person should expect volume growth to be better than last year . Everyone would be waiting for the price to cool down( may not do so though) before they decide to buy unless its a case of urgent need like marriage etc.I have relatives who work as gold artisans and they are unable to get job orders from the jewellery stores for past few months .Same is happening for organised stores as well .No surprise there .

Disc. Not invested .

2 Likes

Q4, Q1 these are lean quarters

They did announce receiving a 200 kg/month order from a big client. Does the Q1 numbers include the revenue from rhat contract or would it come later?

1 Like

A post was merged into an existing topic: 52 week highs and all time highs strategy

Low Volume Growth is compensated by value growth. The charge customers on a markup basis on gold price & not on Volume basis. So in such a business top line growth is important - it may come from volumes or value.

5 Likes

Sky Gold Q1FY26 Concall Update

Robust growth continues in direction of becoming the largest B2B jewellery manufacturer in India

Strategy in place to improve profitability and cash flows by FY27

GML - Gold metal loans have reached 20% mix and on track to reach 70% by Q4FY26

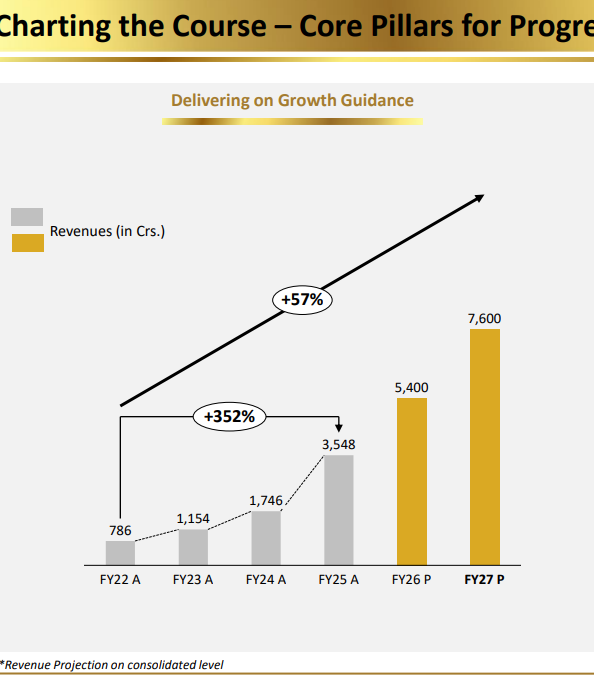

FY27 guidance maintained; implying revenue CAGR of 46% over FY25-27E

Outlook: Positive

Key monitorables: Increase in GML; reduction in working capital cycle; move positive operating cash flows in FY27.

Guidance for FY27 has been re-iterated at –

• Revenue of Rs. 7600 Cr

• Volume sales of 900 kg per month (650 kg/m runrate by Q4FY26)

• PAT margin of 4.5% (4.0% in FY26) aided by rising mix of advance gold model & diamonds; and use of gold metal loans.

• ROCE of 30-35%

• Reduce working capital days to 55 from 98 in FY25.

• Deliver positive operating cash flow

Advance gold model on a rising trend

• Revenue mix has increased to 5% in Q1FY26 vs 4% sequentially.

• Likely to increase to 7.5%/10% mix in FY26/27 which will positively impact PAT margins as well as working capital.

• Recent customers added like Reliance, AB group and Caratlane are on advance gold model.

• Started supplies to Caratlane only till now. Will start with Reliance and AB group in Aug/Sep.

• Recently SG secured a substantial recurring export order of 200 kilograms per month.

• Recent acquisition of Ganna & Gold (bangle maker) operates on 100% advance gold model. Should do 60-70 kgs per month this year starting Q2.

• 18 karat revenue mix was 7% vs 4% in FY25. It has higher margins compared to 22 karat.

• Diamond studded mix is at 0.7%.

Capacity

• Co aims to be India’s largest jewellery manufacturer by expanding its installed capacity. Current capacity is 1 ton per month. Total capacity will increase to 4.5 tons per month by FY28. Production in FY25 was just 0.5 ton; so there is growth runway of 9x sales over next 8-9 years.

Other Highlights

• Onboarded new clients like PMJ and KalaMandir.

• Opened an office in UAE to cater to exports.

• Recent receipt of export order has started execution and till now co has delivered 40 kgs. Will reach runrate of 80 kg per month by Q3FY26.

• Exports mix will reach 17-20% by Q4FY26 from 8% last year.

• GML mix is at 20% in Q1 and will reach 70% by March 2026. Co has received approval for ~Rs. 150 Cr from 3 prominent banks (including Axis Bank).

• Co charges clients on percentage basis and not on per gram basis.

• Debtor days are likely to reduce to 25-30 days in FY26.

Stock is trading at P/E of 13.1x FY27E EPS.

8 Likes

This might be the reason of stock falling after good result. Maybe some insider might know the full story hence selling is happening.

@Sourabh_Gupta , But why this will affect SkyGold? Its not a Jeweller. And actually, even for Jewellers, this will turnnout good for invetsors as the real profits will come out which will be higher than what they are showing in books using LIFO Inventory method??

2 Likes

Yes, it might the same case as Polycab which under shown the revenue by proving its distributor without billing where it dropped more than 15%. Same thing might be happening here else I don’t see any reason of falling after such good result. Valuation is very comfortable with strong guidance. Trying to explore the reason of this fall. ![]()

Dis: Invested/Largest allocation/Biased

1 Like

Reached Oct 2024 price, breaking May low

2 Likes

After the recent selling off by the promoter, stock started falling. Don’t understand what’s the real reason.

Just my thesis behind the fall,

If you look at the current Q1 results, consolidation revenue looks good with a good yoy growth, but standalone revenue for the same looks disappointing, growth rate has come down significantly if you compare it on yoy or qoq basis both looks bad.

Adding more to it in concall when analyst ask the management about the reason, management had no answer to it and asked to mail the investor relations. (I mean a CFO in a concall must have an answer to this simple question on its own company)

I believe the upcoming festive season followed by marriage season can give a boost to sales and company can achieve its year target revenue of 5400Cr with target OPMargin, but we have to see on upcoming quarters how the standalone business does.

Disclosure: Invested

4 Likes

Good points. Is the reason for Promoter selloff clear?

Promoter re-iterated in an interview and concall that it was an attempt to monetize thier stake (which they haven’t done for 2 decades). Also, it was supposed to go to institutions, which couldn’t happen due to execution challenge.

2 Likes

Fair Point. conference call was not managed properly. What I don’t understand, if your communication in English is not decent, let the professionals in your team answer the questions or Speak in Hindi. There were some questions that promoter was not able to understand but still tried answering without thinking. Other than these hygiene issues, the management is walking the talk and is delivering as per their guidance. I think, pin pointing standalone numbers is not a fair assessment in my opinion. we should always look at consolidated numbers

2 Likes