Well, the shares were worth 30 cr when they pledged them which later became 70 cr and honestly it’s impossible to predict where the share price will be so seems like the promoters just took a risky bet. Waved off almost all the interest they paid and got more capital.

Convenient or not they said they would be selling these shares in the Q1 con-call so doesn’t seem like they decided to sell these shares after seeing Q2 performance. If they sell there are questions and if they don’t sell there are questions. What is one supposed to do? Yeah, i understand that it’s difficult to gauge promoter’s honesty in a company of this size and this pace of growth so invest where you are confident and exit where you are skeptical. I have found discrepancies in a few famous small-cap names based on facts and figures and took an exit yet 1 company still continues to do well and a few doomed right after my exit such companies are always just 1 day away from a catastrophe. In the case of sky-gold there is a lack of 100% clarity but whatever is visible looks quite usual to me.

Even if they made decent money of HDFC bank still timing is just too convinient. Also for preferential warrants one should be always sceptical in my belief. Nobody knows better than promoter as to what is the expected growth we depend heavily on guidance numbers from promoters to establish a stock value. So it’s never a risky bet especially if preferential warrant price is below current price. In this case it was ~9% below so promoter did take some buffer there so don’t believe there was lot of risk involved in taking those bets.

Also yes I agree it is wrong to have conclusions based on assumptions rather than facts. Although even if sales of shares was profitable still there is no denying the fact the promoter made more than company made in 2 quarters.

It’s not about that it’s more about loosing one’s hard earned money some investors maybe okay to make one wrong bet and loose some money. But for someone it might be a oversized leveraged bet. So all facts to be upfront and clear if one wishes to invest regardless then good for them.

But it’s never wrong to question more and have deeper insights.

Also its highly competetive industry its very difficult to have clear defining moat. Basically one is betting on management skill and them walking the talk.

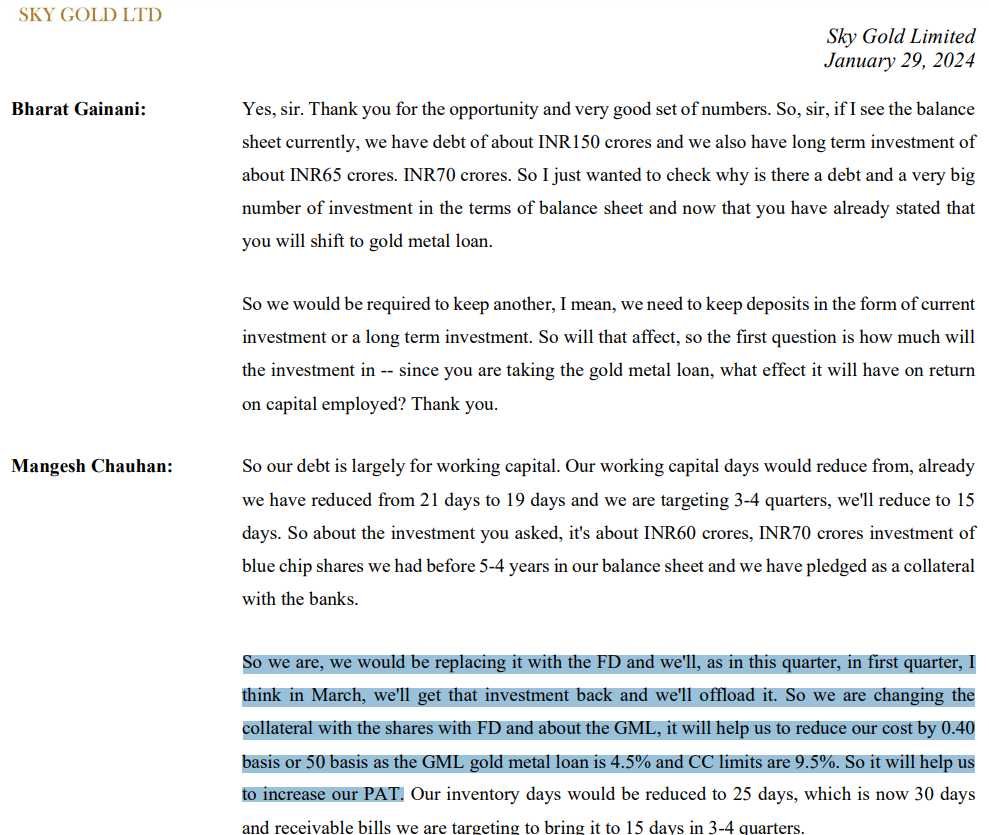

Bluechip shares are being sold to save 4-5% of interest cost as shares will be replaced by FD for GML collateral. Management explained it in Q3FY24 concall.

Warrants have been allotted to the promoters, not the shares. Promoters will have to pay remaining 75% within allowed time frame to be eligible for conversion of warrants to shares.

Remember that Sky Gold’s market cap is close to Rs. 5000cr now. Its no longer a Rs. 200-300cr microcap which can be easily manipulated. Please refrain to make such strong allegations without any strong substantial proof. Opinions are dime a dozen.

Please spend some time to read all concalls and understand its structural nature of the business model. Valuations may be stretched at any time during the journey of the stock - but management doesn’t get to decide the valuation - its the market forces which decide.

@aastar98 - please remove the link to your twitter handle post. Adding links to your personal social media handle posts are not allowed. You cannot use VP platform to get your Twitter post viral.

Every VP’er is encouraged to be skeptical and to do thorough forensic checks for all the businesses. So please use facts and verifiable data (and not some illogical math) before putting serious stock manipulators allegations for the promoters.

I have not read anything in your posts or Vijay Malik’s posts claiming it to be proof that promoters are manipulators. These are just opinions and illogical math.

In future, you are welcome to call promoters as manipulators, but please back it up with solid proof and not illogical math.

Here is a summary of the Sky Gold Limited (SGL) Q2 FY25 Earnings Conference Call held on November 19, 2024. This summary includes key figures and insights from the management’s presentation and the Q&A session:

SGL Q2 FY25 Earnings Call Summary

Strong Q2 and H1 FY25 Performance: SGL achieved record-high quarterly revenues and profits, driven by positive market dynamics and the anticipation of a strong wedding season.

Q2 FY25 revenue reached INR768.8 crores, a 94% year-over-year increase.

Q2 FY25 profit after tax (PAT) was INR36.7 crores, a 405% surge compared to the previous year.

H1 FY25 revenue came in at INR1,491.9 crores, reflecting a 93.3% year-over-year growth.

Growth Drivers and Market Outlook: The Indian jewelry market is poised for substantial growth, fueled by various factors.

The overall market, currently valued at approximately $90 billion, is projected to expand by 12% to 15% annually in the coming years.

Demand is being driven by stock market volatility, a robust wedding season, and general economic stability.

The casual jewelry segment is experiencing rapid growth due to its appeal to younger consumers who appreciate its lightweight and diverse designs.

Strategic Investments and Initiatives: SGL recently secured INR270 crores in funding, which will be allocated to support several key initiatives.

Product Portfolio Expansion: SGL plans to introduce new offerings in 18-carat gold and diamond jewelry to cater to changing consumer preferences.

Subsidiary Growth: Increased capital will be injected into Star Mangalsutra Private Limited and Sparkling Chains Private Limited, with the goal of capturing a larger share of an expanded TAM.

Capacity Enhancement: The company is investing in its workforce by hiring more skilled designers, artisans, and sales and merchandising professionals.

International Expansion: SGL aims to establish a strong presence in key international markets, including the Middle East, UAE, Singapore, and Malaysia.

Acquisitions: The company is actively exploring acquisition opportunities.

Production, Exports, and Key Personnel: SGL reported positive trends in both production and exports.

Monthly production volume in Q2 FY25 averaged 345 kgs, a significant 38% increase from 250 kgs per month in the prior year.

Export sales reached INR63.9 crores, representing 9% of total quarterly sales.

The company appointed Mr. Akash Talesara, a seasoned industry veteran with over 20 years of experience, as President of Sales and Business Development.

Financial Guidance: SGL provided insights into its financial expectations for the remainder of FY25.

The company anticipates generating INR3,300 crores in revenue for FY25.

This projection includes INR2,700 crores from core operations and INR600 crores from the recently acquired subsidiaries.

Management expects a gross margin of 7% to 8% in FY25, driven by an optimized product mix and increased export sales.

The company is targeting a long-term EBITDA margin of 5% to 5.5%.

PAT margin expansion is expected to be achieved through a reduction in interest costs facilitated by increased utilization of gold-metal loans (GMLs).

Key Insights from the Q&A Session

The Q&A session covered various topics, providing further insights into SGL’s operations and strategic direction. Some key highlights include:

Revenue Contribution from Subsidiaries: SGL projects a combined revenue of INR1,000 crores in the next quarter, comprising INR700-750 crores from its core business and INR150-350 crores from the subsidiaries.

Wedding Season Demand: Management expressed confidence in a strong upcoming wedding season.

The management noted that gold prices have decreased by 5% in recent months, leading to greater affordability and potentially boosting demand.

India is expected to see 4.8 million weddings this year, with 25% more weddings occurring in the current quarter.

This increase in weddings is estimated to generate $6 billion in revenue across various sectors, with jewelry accounting for approximately 25% of this total.

Gold Price Outlook: SGL believes gold prices will stabilize in the next 2-3 quarters after experiencing a 20%-25% surge.

Employee Count and Hiring: The company’s employee count has increased to 800, including approximately 650 employees at SGL and 150-180 employees across both subsidiaries.

SGL is open to adding more employees as needed, particularly as its turnover and volume increase.

The company is actively seeking to hire a CFO and add two new board members with significant industry experience.

New Client Contributions: Both CaratLane and P.N. Gadgil contributed to Q2 revenue, and SGL expects their contributions to grow in the coming quarters.

P.N. Gadgil is projected to add INR50-100 crores to SGL’s sales.

CaratLane, which provides SGL with raw materials, is expected to increase production volume by 50 kg in the next two quarters.

Gold-Metal Loan Utilization: SGL is aiming to increase its reliance on GMLs, which are currently at 20%-22% of total debt, to 50%-60% by December and potentially 80%-85% by March.

The blended cost of debt for GMLs is estimated to be around 3%.

Working Capital Cycle: SGL’s working capital cycle is currently around 75 days.

Retail Expansion: The company is currently focused on B2B manufacturing and has no plans to expand into retail in the near future.

Subsidiary EBITDA Margins: The subsidiaries currently have an EBITDA margin of 4.5%, and management aims to increase this to 5.5% by the December quarter.

Subsidiary Sales Estimates: SGL expects its subsidiaries to generate INR1,300 crores in revenue in FY26.

Capacity Utilization:

SGL’s subsidiaries are currently operating at 30%-33% capacity utilization, and the company intends to ramp this up to 100%.

SGL itself has a capacity utilization of 46%.

Export Growth Strategy: SGL plans to increase its export sales from the current 9%-10% to 15% by next year, focusing on markets like Malaysia, Singapore, and Middle Eastern countries like the UAE, Dubai, and Qatar.

Exports are expected to contribute 12%-13% to sales by the end of the current year.

The gross margin for exports is approximately 6.5%.

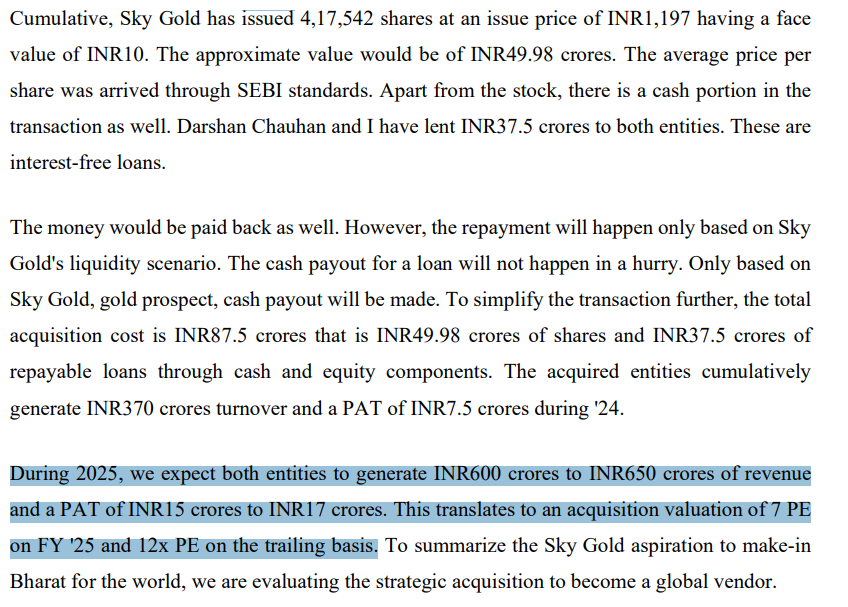

Source of Increased Other Income: The significant other income in Q2 FY25 stemmed from the sale of shares in HDFC Bank and TCS that SGL held for several years.

The company plans to divest its remaining shares, currently held by SBI Bank as collateral, in the December quarter.

Volume Guidance:

SGL’s current monthly production volume is 350 kgs.

The company aims to reach 375-400 kgs per month by the end of FY25.

FY26 volume guidance is 550-600 kgs per month.

SGL expects to reach 750 kgs per month by FY27.

Risk Mitigation Strategy for Gold-Metal Loans: SGL mitigates the risk of gold price fluctuations associated with GMLs by hedging its inventory in the MCX, a commodity derivatives exchange in India.

“Studded Ratio” and Product Mix: SGL plans to increase the proportion of studded and 18-carat gold jewelry in its offerings.

Client Acquisition:

SGL is actively pursuing Tanishq as a potential client.

The company is targeting new clients in the Middle East and Singapore, focusing on mid-sized and smaller companies with growth potential.

Margin Guidance: SGL projects a gross margin of 6.5% and an EBITDA margin of 5%-5.5% for FY25.

Receivables Management:

Increased receivable days in Q2 FY25 were attributed to SGL offering clients extended payment terms due to the substantial rise in gold prices.

Management expects receivable days to decrease in future quarters as they revert to previous practices, onboard new clients with shorter credit terms, and focus on cash-and-carry transactions.

The company expects the growth of its export business, which primarily operates on a cash-and-carry basis, to contribute to a reduction in overall receivable days.

PAT Margin Expectations:

SGL aims to achieve a PAT margin of 3.5% in FY25 by reducing interest costs through increased GML utilization.

The company’s long-term goal is to reach a 4% PAT margin by FY26, supported by new product launches and a focus on high-margin segments like studded jewelry, 18-carat gold, and potentially lab-grown diamonds and Moissanite jewelry.

App Development: SGL is developing an app that will allow clients to view products, check inventory, and place orders online.

The app is currently in its trial phase and is expected to launch in December.

Rationale for Bonus Share Issuance: SGL’s decision to issue bonus shares in a 1:9 ratio aims to improve liquidity and make the company’s shares more accessible to retail investors.

Management believes this move is sustainable given the company’s robust financial position, substantial reserves, and positive profit outlook.

Dividend Distribution Policy: SGL plans to retain profits for the next 1-2 years, focusing on strengthening its financial position and becoming debt-free.

The company will consider dividend distributions once it achieves its financial targets, likely in FY26 or FY27.

International Expansion Risks and Mitigation: The primary risks associated with SGL’s international expansion plans are related to potential credit and payment issues with international clients.

SGL intends to mitigate these risks by focusing on cash-and-carry transactions and limiting credit terms, especially for new clients.

Addressing Competition: SGL believes its strengths, including its position as a leading manufacturer in India, its large-scale infrastructure, skilled workforce, advanced technology, and focus on quality and design innovation, will enable it to compete effectively against both organized and unorganized players.

This summary provides a detailed overview of SGL’s Q2 FY25 Earnings Conference Call, capturing key highlights and insights from both the management’s presentation and the Q&A session. The company’s strong performance, ambitious growth plans, and focus on strategic investments suggest a positive outlook for the future. However, it’s important to note that all information in this summary is derived from the sources you provided.

Sky Gold Ltd (9:1)

Gold jewellery manufacturer and marketer Sky Gold is turning ex-bonus on December 16, 2024. The company’s board on October 26 approved a bonus issue of 9:1, which means the issue of nine new shares for every one share held by shareholders as of the record date.

The board later fixed the record date for the bonus issue as December 16, 2024.

Mumbai-based Sky Gold, listed on both NSE and BSE, is engaged in the business of designing, manufacturing and marketing of gold jewellery.

The company reported a 94.2% year-on-year rise in consolidated revenue from operations to ₹768.8 crore in the July-September quarter. Its EBITDA grew by 154.3% Y-o-Y to ₹38.8 crore. Its Profit After Tax (PAT) grew by 405.2% to ₹36.7 crore over the year-ago period.

The allotment of bonus shares is currently being processed. It will be interesting to see if the distribution of bonus shares leads to selling pressure on the stock.

It’s a usual phenomenon after a bonus/split in a stock. They have an analyst/investor meeting scheduled on Friday, 10th January 2025. In my understanding of the charts, the stock should consolidate between 375 - 400 and then show the move based on the upcoming results. As long as the management maintains the guidance, there is no reason to sell.

I noted the following from their recent filing and earnings call for the quarter ended September 30, 2024:

Unsold inventory stands at Rs. 319 Crores (consolidated).

Capacity utilization is at 46% (Standalone).

The unsold inventory has risen significantly compared to previous quarters. Furthermore, if capacity utilization improves, inventory levels could increase further, but if existing inventory itself remains unsold, improving capacity utilization will not be effective.

Additionally, Sky Gold faces seems to face inventory risks due to its design-focused business model. If a client, such as Kalyan Jewellers, rejects a design or if the design becomes obsolete, inventory may remain unsold. However, a mitigating factor is the ability to recover value by melting the unsold inventory and selling the gold, with losses primarily limited to the making charges.