Which geography is this for? SKM doesn’t export to the US.

Anyone with the understanding of this company and industry can help how should we read last 5 qtrs of subdued results? Not only the sales has come down, but the knock on operating margins is much higher. Following reasons:

- Lower prices of finished goods with stable volumes?

- Stable prices with lower volumes?

- A combination of above 2 options?

Similarly on operating margins side:

- Lower finished goods prices with higher raw material prices?

- Any other combination?

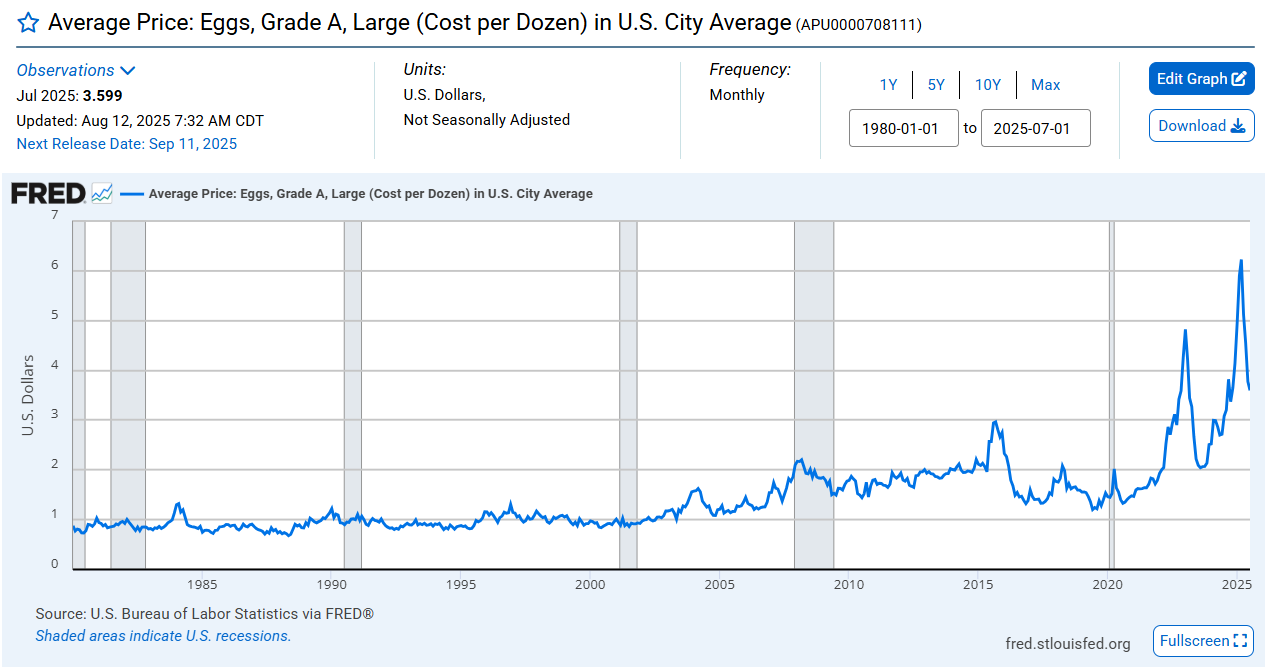

Russia / Japan and Europe are the top 3 places where they were exporting. Bird flu is a seasonal factor and happens every year. Is there anything specific / special that has impacted this company adversely this time? Best of my understanding, egg prices in US are up by ~50% in last 12 months. Don’t know how this is playing in SKMs exporting territories, but the probability of anything substantially different should be low.

There is little available in the public domain to develop better understanding. Any industry / domain expert can help.

Thanks

1 Like

Egg prices globally in most countries have sky rocketted to lifetime high levels. Especially USA and Japan.

The incidence of bird flu has been severe in both these countries as comoared to last year especially in the birds that are bred to lay eggs… called layers.

To replenish the layer stock should take 6 to 9 months which means high egg prices for next 2 to 3 quarters with a hope that there is a milder incidence of bird flu next season.

The negatives of the egg price spike 2 years back was that many formulations were moved to plant based substitutes which subsequently led to higher global inventory levels esp in albumen.

As dried egg powder inventories get run down better pricing will follow for subsequent contracts. My sense is that prices of dried egg powder will see a meaningful increase from 1QFY26.

3 Likes

Current quarter will be impacted due to following events.

Outbreak of bird flu in some remote cases (in other states not Tamil Nadu) >>> this in turn had depressed egg prices across all egg markets.

The average price for Namakkal for 4Q was Rs 457 per 100 eggs thus down 15% QoQ and 8% YoY.

The company has increased insourcing production through contracts with farmers. Also with high inventory in international markets more sales were getting diverted to local markets.

Thus performance in this quarter could see an impact sequentially.

But soon international egg powder prices should start increasing as inventory levels revert to normal. This will have a much greater bearing on the company’s financials.

Promoters had also started buying just before shut period.

Views and insights welcome.

5 Likes

The stock moved quickly from 160 to 240 levels. Further upside/downside will depend on q1 results. FY 25 was bad for the company.

2 Likes

Management has added decent stake in June. Better days for the company may be expected in the next few quarters. Price is already above 300 well before Q1 results are out.

This company may also have a positive effect of the tariff wars.

2 Likes

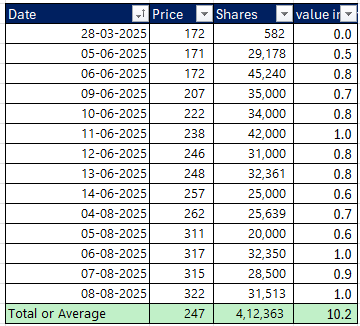

Promoter has created FOMO now, we are not getting chance to add near 300 levels.

Orders are executing today. Bought some today.

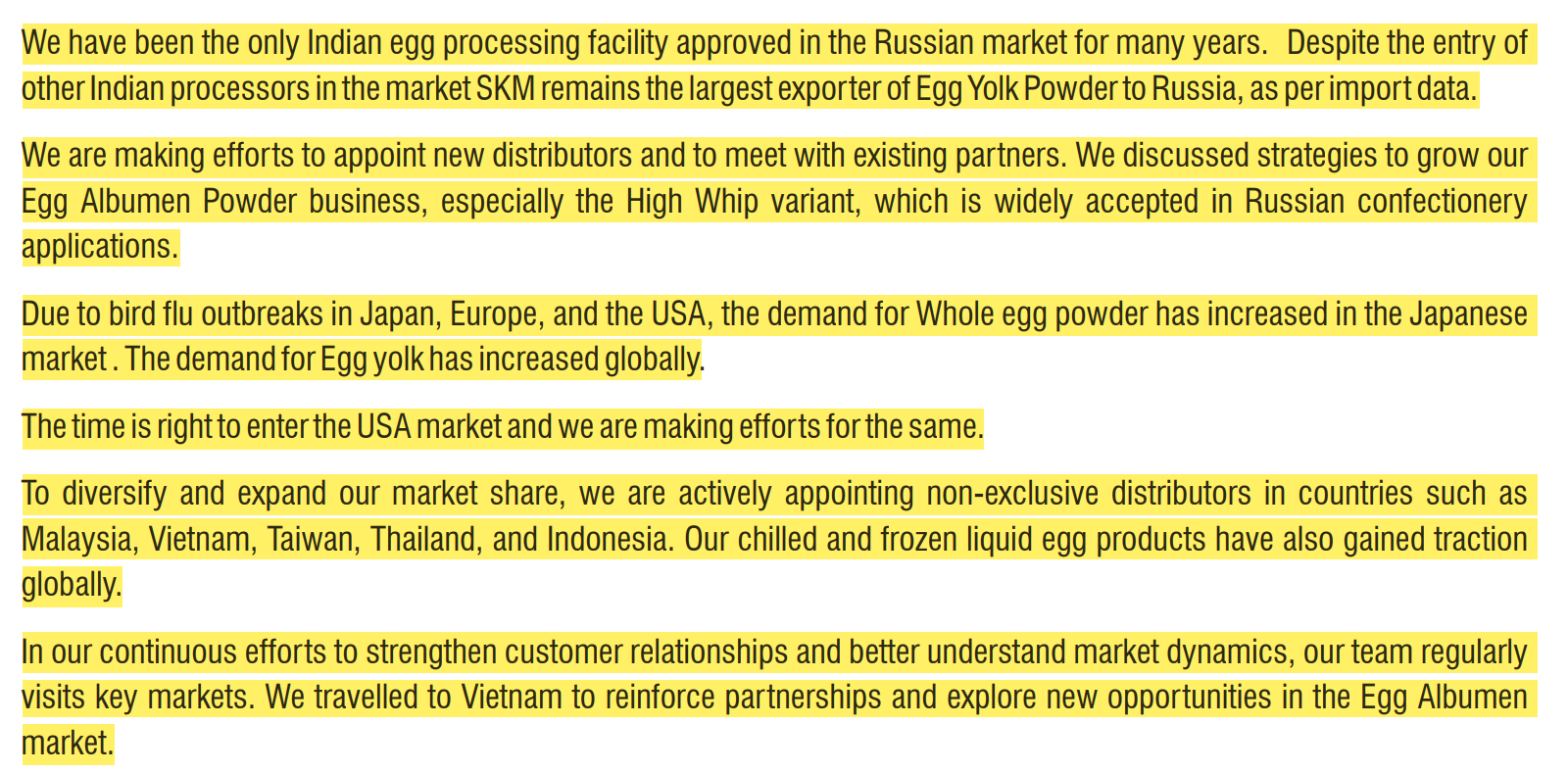

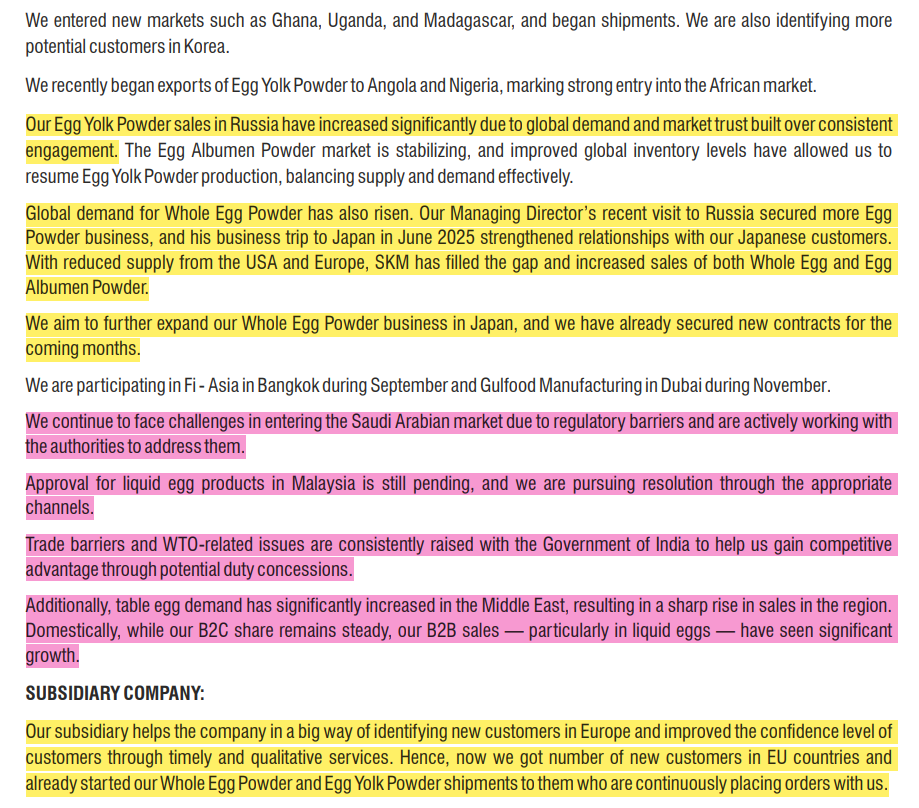

Below snippets are from AR. Struggling to find more information.

4 Likes

Very noticeable times are FY 2022 when the SKM Egg made good PAT

SKM Egg from india one which benefited the most last time around. Coz of certifications too SKM got preferred. This time around Px they get in export market to US good be very attractive (given the realizations last time) - Good to note the capacity utilization this time - Expecting north of 20% margins

Historical Bird Flu times:

SKM could command higher realisations without proportional increase in raw material costs.

2025 outbreak seems fierce vs past. Longer too. 2025 prices peaked higher ($6.70/dozen wholesale) than 2015 or 2022.

3 Likes

Notes from AGM 2025

Egg Drying Capacity to increase from 7000 MT to 10000 MT next Financial Year. Management expects to utilize this capacity fully over the next 2 to 3 years.

Has been running at hundred percent capacity realization for the last five months.

Booked for Japan and Russia till the end of Dec via tenders. Prices across product segments in line or marginally better sequentially.

Eyeing new markets in Africa and new mixes especially catering towards B2C.

Also investing 65 crores in environmentally controlled shed part two. This will enable better yield and also increase biosecurity of the birds.

The biogas plant has a capacity will be better utilized with new EC Shed coming online.

Currently has got backward integration to 24 lakh birds laying 18 lakh eggs every day. Another 2 lakh eggs are purchased from the open market. This enables significant control over costs.

As funds permit the company will keep adding birds to match up with increased dried egg demand.

Views welcome as well as points that i might have missed.

11 Likes

Thanks for sharing AGM summary.

Did management give clarity on below points? or does anyone from community have any clue on below points?

- SKM Order book for Fy2026

- Any increase in demand of company’s egg products globally due to major bird flu cases in US/Europe in Q4Fy25? Similar to what we saw post 2022 bird flu outbreak.

- Revenue, margin, earnings guidance for Fy2026

So,

(1) they are currently running at 100% capacity utilization and from orders perspecitve are comfortably booked till December 2026.

(2) Expect FY 26 EBITDA margins to be14% or better.

(3) Expect 7000 MTPA to 10000 MTPA expansion by FY 27 and full utilization in next 3 years.

(4) Bird flue in other countries helps them a lot as it brings down supplies and it take about an year for such a country to resume production. In order to control bird flue for themselves, they are investing about 65 Cr to move their full production to environmentally controlled sheds.

9 Likes

(1) Management is already considering a stock split.

(2) Expect quaterly earnings call going forward.

(3) Changed invoicing to INR from USD whereever they could.

(4) 98% is exports. All B2B.

(5) Products shelf life is 18 months or so.

(6) 1000 employees.

11 Likes

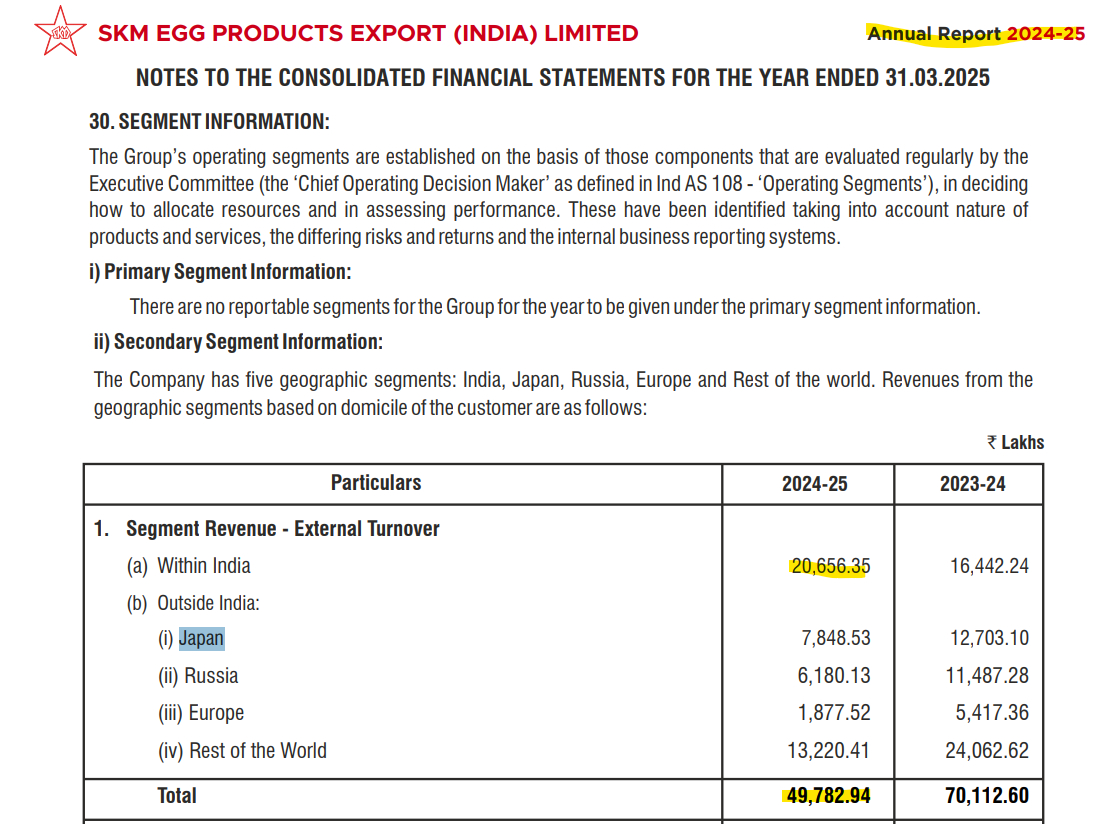

FY25 Annual report shows revenue from exports and domestic is approximately 60% and 40% respectively.

Not sure why exports are mentioned as 98%. Please throw some light on this.

2 Likes

Large part of domestic sales is where they sell feed to the farmers and in turn buy eggs as per terms agreed. Thus actual domestic sales is much lower than what the above numbers suggest. Refer Pg 190 of the annual report. Broadly domestic sales will be ~ 15% of total.

3 Likes

5 Likes

Japan and parts of Europe continue to see bird flu

4 Likes