Late to the yolk party?

I only recently screened this stock via a modified “Magic Formula” screen. Magic formula is used to screen stocks with high earnings yield (PE reversed) and high return on capital. This post is my quick study of the company at the current valuation. Please feel free to comment and share your opinions.

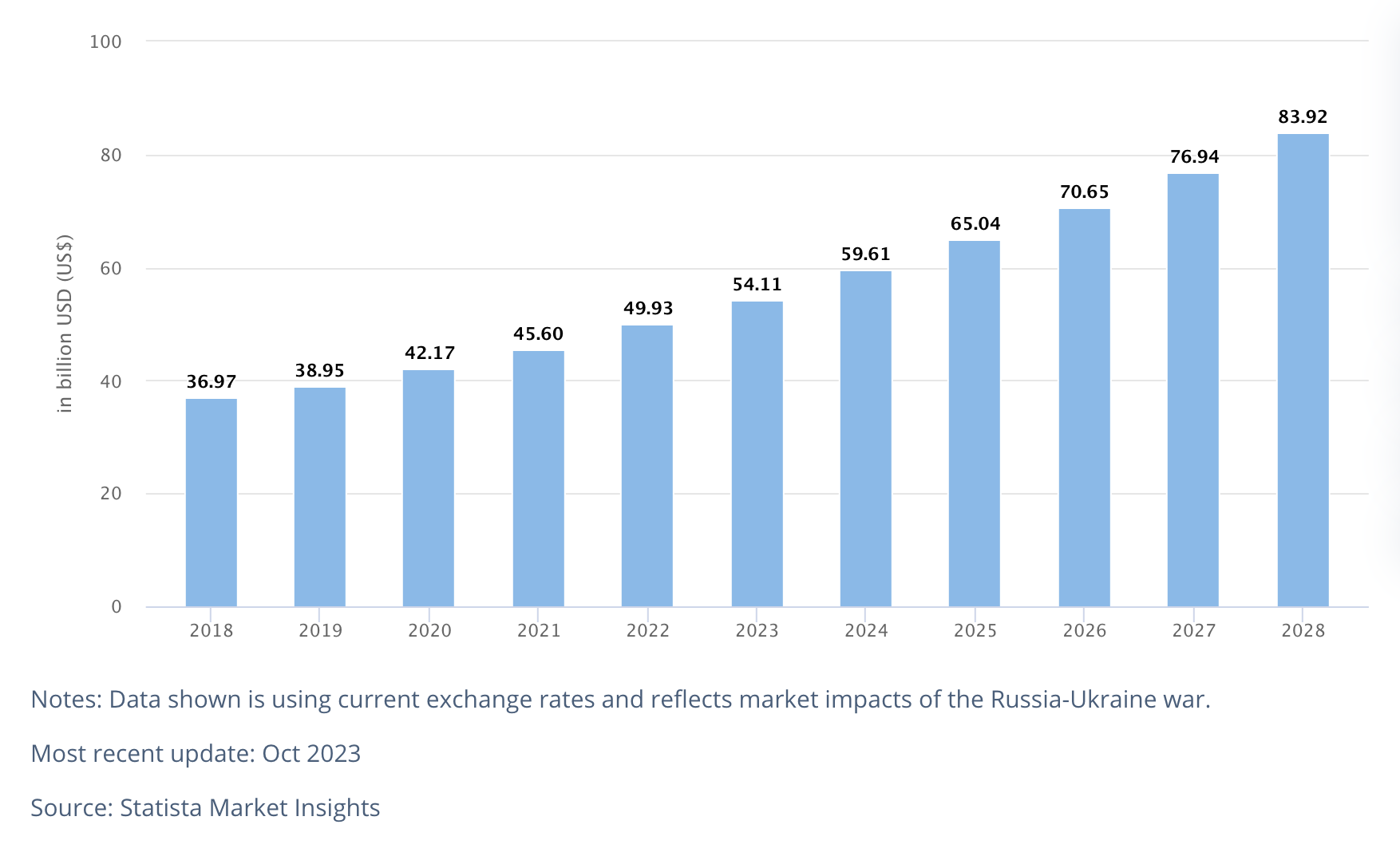

Eggs market (Asia):

- The market is expected to grow annually by 9.17% (CAGR 2023-2028)

- Biggest consumer is China (Around 37%)

- Consistent consumption growth (not exponential) expected. Below graph shows revenue growth from Egg market in Asia:

Is this a pure commodity play? Understanding cyclicality

You’re absolutely right as eggs are nothing but a commodity. But an important characteristic of a commodity company is cyclicality. Speaking specifically about the egg market, demand side cyclicality is very minimal. Examples of demand side cyclical sectors would be hotels, tourism etc. Sure there could be some shallow cyclicality around the holidays when baking volume and egg consumption increases, but the majority of the fluctuation in price revolves around supply side cyclicality:

- Mortality rate: Mortality rate may rise due to high temperature. The average mortality rate of a flock is from 20 to 25 percent per year. Hence the summer months have higher hen mortality rates due to heat stress, respiratory diseases, insect diseases and change in water intake and appetite. In order to combat many of these factors, poultry farmers may reduce ventilation to maintain a comfortable temperature for the birds. However, this can lead to poor air quality and an increased risk of respiratory problems. What’s the biggest concern is that Egg-laying hens are more productive during warmer months. Hence, one bad summer could affect the business rather drastically.

- Production costs: Fluctuations in the cost of feed ingredients, such as grains and protein sources, can affect egg prices. If feed prices rise, the company may need to pass on those higher costs to consumers in the form of higher egg prices.

- Extreme conditions: Extreme weather conditions, such as droughts or floods, can affect feed availability and transportation of eggs, potentially leading to supply shortages and higher prices. Along with this don’t forget possible outbreaks of H5N1, a highly transmissible and fatal strain of avian influenza, or bird flu.

Those tracking this company might have already realised that, apart from a black swan sort of an event (such as point 3), SKM is backward integrated. They have a Rs 10 Cr feed mill for producing poultry feed. Laboratories attached to the mill to ensure nutrient composition and feed free of toxins, pesticides etc. Allows for specific formulations for different types of chicks. Why is this important? This removes a lot of the cyclicality aspect in production costs. When it comes to mortality rate, they have high end infrastructure to minimise external effects to the production cycle. What about unpredictable bird flu outbreaks? Looks like the company has this taken care of as well. The company’s website mentions:

Avian Influenza - Strict biosecurity measures are deployed to avoid the Avian Influenza outbreak. Fencing, No vegetation in the farm, sanitation of vehicles are part of biosecurity measures.

What this ultimately means is that SKM is able to reduce a lot of cyclical aspects in a cyclical commodity such as eggs. That’s a huge advantage that often goes unnoticed.

Egg prices (Asia):

Recently, @ankit_tripathi brought up a very important point in this thread regarding egg price trends in the US. However, SKM’s primary client base being Asia and Europe, egg prices in China should be a better descriptor of the trend. It has gone up by around 10%. However it looks like the egg prices are trending upwards. This can be interpreted in a positive way if the company is able to prevent a supply side shock due to a bird flu outbreak and maintain a stable production rate, they should benefit from higher egg prices even if they maintain their current volumes.

Financial performancee:

- Profit/Sales growth: Probably the most important point in this post. The scepticism of the jump in profit growth! Operating profit in Mar’22 stood at 31Cr and in Mar’23 jumped to a whopping 144Cr. There’s no way that’s normal right? Well the primary reason for this is the sales growth and margin expansion causing a combined exponential jump. This is a classic case of Operating leverage! Sales during the same period doubled while the OPM also doubled during this time causing a whopping 4X on the profit during this year. The real question you’re supposed to be asking is what is a normal profit growth rate going forward and that will depend on whether your margins are sustainable or not! More in the Valuation section.

- Margins: They are currently at peak margins of 24%. Normally, peak margins would be a red flag in a commodity company. Especially when the management has not provided any PPTs/Concalls recently to clarify the guidance. However, as I said earlier about cyclicality, the company seems to have infrastructure capable of eliminating much of that cyclicality. These margins of 20-25% are looking stable for the past 4 quarters. Hence, these margins could end up being sustainable in the long run, but only time will tell (if not the management).

- Piotroski score: A piotroski score of 8/9 indicates a very strong financial performance all round.

- Cash flow: Sitting on healthy Cash flow from operations of 60Cr

- Debt situation: Now if you haven’t noticed already, debt on the company’s balance sheet is something to consider. They have Rs 141 Cr of borrowings. Debt is not necessarily a bad thing. Especially if the company is able to make good use of the debt. What do we check for that? ROCE - 46% and ROIC - 31% shows that the company is generating good return on the capital at hand. Besides, the company has reserves of Rs 225Cr showing that they are have undertaken a manageable amount of debt. The CARE rating also suggests that the outlook is stable and has improved significantly from last year (D/E of 0.8 to 0.5) however any more debt would start to slip out of hand:

Any further large debt-funded capex leading to deterioration in the capital structure with overall gearing above the range of 0.75x.

- Capex: the company had planned for capex towards setting up of Environmental controlled (EC) shed for birds and Bio -gas plant with total project cost of ₹70 crore of which ₹50 crore funded by debt and rest by accruals. The project is expected to be completed by Q1FY25. The debt looks to be primarily used to fund this Capex.

Valuation:

- PE ratio: Trading at a PE of 8.7, the PE ratio has decreased from levels of 27 in 2022. The primary reason for the decrease looks to be the exponential increase in earnings. These growth rates are probably not sustainable due to which the PE does not entirely reflect the recent earnings. So is it undervalued? The PEG is a great measure for this!

- PEG ratio: A PEG of 0.07!? Surely that’s a steal! Well, this only points to the fact that the growth is absolutely unsustainable. So what is a sustainable number that we can expect? The honest answer is that no-one can tell considering the company’s lumpy numbers in the past. But what we can do is be prepared for a few different scenarios. If we were to expect a modest 10% EBITDA growth rate, that would give us a PEG of 0.9 for the current PE, which is in my opinion fairly valued. And any growth rate above 10% would start making the current PE more and more undervalued. In my opinion, the Capex initiative to be completed in Q1 FY’25 will only help the company expand its margins. So they are on the right track to sustainable profitability. I would assume a 15% growth rate is not out of the question.

Anything to watch out for?

- Operating deleverage: Currently operating leverage looks to have kicked in. What does this mean? It’s a period when your fixed costs remain constant but your revenue increases, leading to margin expansion and improved asset turns. This leads to explosive growth rates, as seen for SKM over the last year. Asset turnover improved from 1.3 in FY’21 to 2.3 in FY’23. But the exact opposite would lead to a situation of operating deleverage. Where companies lose demand, but their fixed costs remain the same and their margins slump ultimately leading to asset turns dropping again. What goes up exponentially could come down exponentially!

- Lack of info: No matter how much you dig and dig, unless you have someone from the inside of the business telling you what’s happening, everything that we discuss is just speculation. I hate it when companies do the bare minimum when it comes to concalls/PPTs/interviews, SKM is another such company where you are not going to get any upfront guidance. It makes our jobs as retail investors much harder.

So are you too late to the yolk party? What do you guys think? ![]()

Open to everyone’s opinion