GS Sundararajan, MD and Subhasri Sriram ED add the call:Highlights by Capital Mkt

The company has witnessed very good quarter, while showing healthy loan growth. The key segments such as two wheelers and small enterprise have exhibited better loan growth.Assets under Management (AUM) growth of the company accelerated to 16% at Rs 17483 crore at end June 2015 against 14% a quarter ago and decline of 2% a year ago. The disbursements improved 10% to Rs 4234 crore in Q1FY2016.However, the key operating states such as Tamil Nadu and Andhra Pradesh have been performing weak.The company is number one two wheelers financier by size in state of Andhra Pradesh and Tamil Nadu.The company expects loan growth for SME and Two wheelers at around 14-15% for FY2016.The company has not conducted any securitization deals in Q1FY2016.The recent gold price decline do not worries the company on its gold loan book asset quality.As a result of decline in gold prices, the company as reduced the per gram lending rate by Rs 100. Gold Loan Book GNPA stood at 2.35% and NNPA at 1.17% at end June 2015.

Overall Gross NPA ratio rose to 3.17% at end June 2015 from 3.12% at end March 2015.The capital adequacy ratio was healthy at 28.2% with the Tier I ratio at around 24%% at end June 2015.The company plans to shift NPA recognition norms from existing 180 days to 150 days over dues basis on 31 March 2016. As per the company, the GNPA ratio is higher at 5-5.5% under 150 days over dues norms compared with 3.17% under 180 days.The company and its collections teams are orienting customers to adapt to the new NPA recognition norms.The company expects the employee count to remain flat in FY2016. The company is planning to improve the expense ratio to 36% over next 3-4 quarters.

The company has doubled the dividend rate because of excess capital position. While utilizing the excess capital for new acquisitions, the company would take such decisions cautiously.

GS Sundararajan, MD &Subhasri Sriram, ED addr the call:Highlights by Capital Mkt

The company continues to exhibit steady growth across all segments in Q2FY2016, while well penetrating in to all geographies. The company expects second half of FY2016 to be better in terms of growth.Assets under Management (AUM) growth of the company accelerated to 17% at Rs 18165 crore at end September 2015 against a growth of 16% a quarter ago and 3% a year ago.The disbursements increased 9% to Rs 4527 crore in Q2FY2016 over Q2FY2015. Segment wise disbursement stood at Rs 1995 crore - small enterprise finance, Rs 800 crore - two wheelers, auto loans - Rs 200 crore, personal loans Rs 250 crore and Rs 1291 crore – gold in Q2FY2016.Off-balance sheet AUM of the company stood at Rs 500 crore, which is less 3% of AUM. The company has not conducted any securitization deals in H1FY2016, while expects to conduct securitization deals only in Q4FY2016.Overall Gross NPA ratio rose to 3.3% at end September 2015 from 3.17% at end June 2015. However, the Net NPA ratio was maintained at 0.65% with strong provision coverage ratio of 80.2% at end September 2015.Write-offs stood at Rs 71.23 crore, GNPA ratio including write-offs, stood at 3.69% at end September 2015.

Gross NPA increased by 50 crore in Q2FY2016 to Rs 582 crore at end September 2015, mainly contributed by small enterprise finance and gold loan book.Gold Loan Book GNPA stood at 2.55%, while non-gold GNPA was at 3.51% at end September 2015.

The company plans to shift NPA recognition norms from existing 180 days to 150 days over dues basis on 31 March 2016.As per the company, the GNPA would double to Rs 1000 crore from present level of Rs 582 crore, after shifting to 150 days over dues NPA recognition norms from present 150 days.Based on the current balance sheet position, the company estimates GNPA to be at Rs 1300 crore on 120 days and Rs 1700 crore on 90 days over dues basis.

With the huge customer base and small ticket size, the company and its collections teams are educating customers to adapt to the new NPA recognition norms.

Shriram Housing Finance:Shriram Housing Finance has crossed the AUM level of Rs 1000 crore at end September 2015. The AUM comprises mainly 90% of retail loans and 10% builder finance.The branch network of the company stood at 77 branches at end September 2015.

During the quarter, Shriram Housing Finance has tightened its NPA coverage and provisioning norms, which had a impact of Rs 1.2 crore on profitability. Accordingly, the provision coverage ratio was raised to 24% from 18%.

CONFERENCE CALL

Shriram City Union Finance

Expects AUM growth of 15%+ for FY2016 and FY2017

Shriram City Union Finance conducted a conference call on 28 January 2016 to discuss the financial results of the company for quarter ended December 2015. Subhasri Sriram, Executive Director of the company addressed the call:

Highlights:

Assets under Management galloped 18% yoy to Rs 19015 crore at end December 2015, driven by gold loan book rising 25% to Rs 3488 crore at end December 2015. Non-gold loan book increased 16% yoy to Rs 15528 crore at end December 2015.

Disbursement increased mere 3% to Rs 4665 crore in Q3FY2016 over Q3FY2015, which were hit by rains and floods in Tamil Nadu and Coastal Andhra Pradesh.

The Tier II and III cities continued to contribute to the loan growth of the company.

The small enterprise finance loan of the company increased 19% constituting 5% of the overall AUM.

The traditional markets such as Tamil Nadu, Andhra Pradesh, Maharashtra contributed 86% of the SME loan down from 90% a year ago.

The traditional markets also contributed 70% of two wheelers and above 99% of gold loan book AUM.

The provision coverage ratio was maintained stable at 80.6% at end December 2015, while maintaining credit cost.

The yield on loans stood at 21.53%, while the company has improved NIMs to 13.94% in Q3FY2016 from 13.51% in Q2FY2016. The cost of borrowings has eased to 10.34% at end December 2015 from 10.54% at end September 2015.

The CRAR ratio of the company stood at 26.08% with Tier I ratio at 23.83% at end December 2015.

The cost-to-income ratio of the company stood at 41.47% in 9MFY2016 compared with 41.26% in FY2015.

The employee count of the company was stable at 25400 staff at end December 2015, which is expected to rise marginally over next one year.

As per the company, the board would decide whether to maintain provision coverage ratio higher at 80% after GNPA would rise on shifting to 150 days overdues NPA recognition norms by March 2016 from present 180 days.

Write-offs stood at Rs 81.47 crore in Q3FY2016 up from Rs 71.23 crore in Q2FY2016.

Gross NPA rose slightly to 3.39% at end December 2015 compared with 3.30% a quarter ago and 3.02% a year ago. Meanwhile, Net NPA ratio was flat on sequential basis at 0.66% at end December 2015, while rose from 0.64% a year ago.

Non-gold GNPA was at 3.59% at end December 2015 up from 3.51% at end September 2015.

The company plans to shift NPA recognition norms from existing 180 days to 150 days over dues basis on 31 March 2016. As per the company, the GNPA would rise 5%+ after shifting to 150 days over dues NPA recognition norms 7%+ on 120 days and 9% o n 90 days over dues basis.

The company expects AUM growth of 15%+ for FY2016 and FY2017.

Shriram Housing Finance

Shriram Housing Finance reported PAT at Rs 7.89 crore in Q3FY2016, up 63% yoy.

The loan book improved 8% qoq to Rs 1082 crore in at end December 2015, which consisted of Rs 1017 crore of retail loans and Rs 65 crore of builder finance.

The branch network of the company stood at 79 branches at end December 2015.

GNPA ratio stood at 3.09% at end December 2015. which was marginally impacted by Tamil Nadu rains.

The company has received SARFAESI licence, while also succeeded in acheiving NHB refinance in Q3FY2016.

I absolutely loved the way the MD Mr. Sundararajan spoke about “serving” the segment of people who don’t have regular cash flows, and how it is very important to be “real” when we talk about financial inclusion.

It always biases me (+vely) when the management seems honest to the bigger purpose of the organization, rather than just the next quarterly results.

CONFERENCE CALL - from Capital Markets

Expects to maintain healthy growth trajectory for FY2017

Shriram City Union Finance conducted a conference call on 28 April 2016 to discuss the financial results of the company for quarter ended March 2016. Subhasri Sriram, Executive Director of the company addressed the call:

Highlights:

- Assets under Management increased 17% yoy to Rs 19576 crore at end March 2016.Gold loan book increased 13% to Rs 3328 crore at end March 2016, while non-gold loan book moved up 18% yoy to Rs 16248 crore at end March 2016.

- Disbursement increased 12% to Rs 5222 crore in Q4FY2016 over Q4FY2015.

- The small enterprise finance loan of the company increased 19% constituting 54% of the overall AUM. Two-wheelers loan (18% share) moved up 17%, while gold loans (17% share) increased 13% at end March 2016 over March 2015.

- The company has shifted NPA recognition norms to 150 days over due basis from 180 days over due basis. This has caused surge in GNPA ratio to 5.15% at end March 2016 from 3.39% at end December 2015 on 180 days over due basis.

- GNPA ratio for non-gold book stood at Rs 5.44% and gold book at 3.82% at end March 2016. Segment wise GNPA was at 5.4% for small enterprise finance, 5.05% for two-wheelers, 6.44% for auto loans, 5.96% for personal loans.

- On account of shift to 150 day over due NPA recognition norms, the company exhibited surge in NPAs along with jump in provisions and write-offs. The impact of higher NPA provisions at Rs 139 crore, accelerated standard asset provision from 0.25% to 0.3% at Rs 8 crore and income de-recognition at Rs 30 crore, together impacted P&L by Rs 177 crore in Q4FY2016.

- As per the company, the GNPA would rise to 7% after shifting to 120 days over dues NPA recognition norms by March 2017 and 9.3-9.5% on 90 days over dues basis by March 2018.

- The write-offs stood at Rs 305 crore in FY2016 compared with Rs 326 crore in FY2015.

- The company also made employee benefit provisions of Rs 22.89 crore (Rs 12.62 crore for FY15 and Rs 10.27 crore for 9MFY16) in Q4FY2016 on account of changes in Bonus Act impacting the P&L of the company.

- The provision coverage ratio on NPAs declined to 69.6%, on 150 days over due basis, at end March 2016 from 80.6%, 180 days over due basis, at end December 2015. the company is examining room for further reduction in provision coverage ratio in FY2017.

- The yield on loans stood at 21.5%, while the company has maintained NIMs to 13.5% in FY2016. The company dont expect any reduction in lending rates, which remains steady for last one year. Thus, the company is expecting margins to maintain or improve, with the further reduction in cost of borrowings.

- The company expects RoA at 2.3-2.5% for FY2017, factoring in additional NPA provisions on account of shifting to 120 days over due NPA recognition norms in FY2017.

- The company expects to maintain AUM growth trajectory in FY2017.

Shriram Housing Finance

- Shriram Housing Finance reported PAT at Rs 7.3 crore in Q4FY2016, up 16% yoy.

- The loan book improved 18% qoq and 73% yoy to Rs 1275 crore in at end March 2016, which consisted of Rs 1187 crore of retail loans and Rs 88 crore of non-retail loans.

- The disbursements of the company stood at Rs 273 crore in Q4FY2016 and Rs 792 crore in FY2016.

- The branch network of the company stood at 79 branches at end March 2016.

- GNPA ratio declined to 2.76% at end March 2016 from 3.09% at end December 2015. The NNPA ratio also moderated to 1.99% at end March 2016 from 2.3% at end December 2015.

- The provision coverage ratio of the company stood at 27%.

- As per the company, the AUM growth of above 50% is possible for next three years.

Shriram Transport Finance

Expects AUM growth of 15% for FY2017

Shriram Transport Finance conducted a conference call on 29 April 2016 to discuss the financial results of the company for quarter ended March 2016. Umesh Revankar, Managing Director of the company addressed the call:

Highlights:

- The company has exhibited acceleration in loans growth to 23% at Rs 72760.6 crore at end March 2016. The company has overachieved the loan growth against the target of 15%.

- Disbursements stood at Rs 12700 crore for Q4FY2016, of which new commercial vehicles disbursements stood at Rs 1920 crore.

- As per the company, the expectations of excess monsoon for southwest monsoon season 2016 is big positive, while rising infrastructure spending is also a major positive with lot of tendering activity taking place. Also the Union Budget 2016-17 is pro-rural, which is making company optimistic about second half of FY2017.

- The company has maintained the guidance of loan book growth of 15% for FY2017.

- The company conducted Rs 4800 crore of secularization deals at reasonable rates in Q4FY2016.

- Net interest margin of the company improved to 7.65% in Q4FY2016 from 7.47% in the previous quarter and 6.67% in the corresponding quarter last year. The better treasury management with low cash levels, decline in borrowing cost and strong securitization deals at better rates have propped up NIMs of the company in Q4FY2016.

- The company expects to maintain NIMs in FY2017. However, expects some pressure on loan yields from rising share of new vehicles loans. Also, the company dont expect any benefit from banks MCLR based lending rate regime, as its borrowing are mainly for over 3-years duration where the MCLR based lending rates are higher than the base rates.

- The company has shifted NPA recognition norms to 150 days over due basis at end March 2016 from 180 days over due basis. Due to shifting NPA recognition norms to 150 days overdue basis, the GNPA ratio of the company increased to 6.18% at end March 2016 and Net NPA ratio galloped to 1.91% at end March 2016.

- The merger of Shriram Equipment Finance Company (SEFCL) was completed with Shriram Transport Finance Company. About 130 bps of rise in GNPA ratio (at 6.18% at end March 2016) was contributed by merger of SEFCL. The GNPAs of the SEFCL stood at Rs 893 crore at end March 2016.

- Excluding the merger impact, the GNPA ratio of the company is showing increase to 4.88% (150 days over basis) at end March 2016 from 4.29% (180 days over due basis), entirely on account of shifting NPA recognition norms to 150 days over due basis. However, the company is showing an improvement in asset quality, reducing GNPA ratio 4.22-4.25% at end March 2016 with 180 days overdue basis NPA norms.

- As per the company, the GNPA ratio would increase by 150 bps on further shifting to 120 days NPA recognition norm in FY2017 and by another 150 bps on shifting to 90 days NPA recognition norms in FY2018.

- On account of shifting to 150 days over dues NPA recognition norms, the NPA coverage ratio of the company is reduced to 70.5% (150 days over due basis) at end March 2016 from 80.2% at (180 days over due basis) end December 2015. As per the company, coverage ratio would be reduced by 10 percentages each year in FY2017 and FY2018.

- As per the company, the loan book of the SEFCL has declined to Rs 1650 crore at end March 2016 from Rs 3000 crore a year ago, driven by recoveries, while the company has also conducted write-offs of Rs 300 crore.

- As per the company, the company had to make additional provisions of Rs 300 crore on shifting to 150 days over dues NPA recognition norms from 180 days over due basis. The company also recorded interest income de-recognition of Rs 16 crore. However, the loss on merger of SEFCL was at Rs 360 crore.

- The write-back of provisions on account of reduction in provision coverage ratio from 80% to 70% was Rs 415 crore.

Can anyone shed some light on this deal? Does this mean there is not much coming out for Sriram from this deal? Time to exit or simply wait and watch?

Highlights of the Q4 concall (source: capital market)

- The company accelerated loan growth 19% to Rs 27461 crore at end March 2018. Disbursement increased 6% to Rs 6632 crore in Q2FY2018 over Q2FY2017. The company has also accelerated the net profit growth to 20% at Rs 665 crore in FY2018.

- The company expects 20% loan growth and stronger earnings growth for FY2019. The loan growth in two-wheeler loan segment is expected to be 20-22% in FY2019. The company proposes to re-focus on gold loan segment and bring in a strategy to grow gold loan book.

- The company has implemented robust loan sourcing and underwriting strategy across the country, which is expected to help improve employee efficiency, expense ratio and credit quality.

- About 50-60% of the borrowings of the company are on fixed rate base, so the company expects to maintain cost of funds at steady level in FY2019.

- The company has shift its NPA recognition norms to 90 days overdue basis end March 2018, while expects credit cost to decline to 3% (+/-15 bps) in FY2019. The company would maintain provision coverage ratio in the range of 60-65%.

- The GNPA ratio stood at 9% and NNPA at 3.4%, while the company expects to reduce NPA ratio in FY2019.

- Interest income reversals stood at Rs 29.2 crore in Q4FY2018.

- The company is looking at rationalization of 1500-2000 of its employee, while expects to reduce operating expense to AUM ratio by 25-30 bps FY2019.

- The off-book AUM stands at mere 0.3-0.4% of AUM end March 2018.

- The housing finance subsidiary has exhibited improvement in asset quality and disbursements in Q4FY2018.

Latest Credit Rating Report of the company. http://www.careratings.com/upload/CompanyFiles/PR/Shriram%20City%20Union%20Finance%20Limited-08-27-2018.pdf

Key Points.

- Total AUM of Rs. 29,193 crore as on June 30, 2018.

- Company has witnessed AUM growth with CAGR of around 18% for the last three years ending March 2018.

- In FY18, the total AUM grew by 20% YoY aided by 54% growth in Personal Loans, 24% growth in 2W and 22% growth in SME loans.

- As on March 31, 2018, the company’s funding profile is comprised of bank loans occupying 60% of overall funding, followed by NCDs and Sub debts aggregating 15%, Commercial paper 11% respectively and fixed deposit programme 14%.

- The average cost of borrowings reduced to 8.9% during FY18 from 9.8% during FY17 due to run down of older borrowings.

- Total CAR stood at 21.40% as on March 31, 2018 (23.91% as on March 31, 2017) and Tier I CAR stood at 20.60% as on March 31, 2018 (22.25% as on March 31, 2017). The CAR and Tier I CAR as on June 30, 2018 was 20.98% and 20.30% respectively. The current capital is sufficient for the company for the next 3-5 years by maintaining CAR more than 15% while growing their book by around 18-20%.

- South occupying 67% of the overall AUM followed by West with 23%, North occupied remaining 10% of the overall AUM as on June 30, 2018.

- Top 4 states (Tamil Nadu, Andhra Pradesh, Maharashtra and Karnataka) occupied 79% of the total AUM as on March 31, 2018 as against 82% as on March 31, 2017.

- With migration on NPA recognition norms from 120 dpd to 90 dpd by end of March 31, 2018 gross NPA increased from 6.73% as on March 31, 2017 to 9.01% as on March 31, 2018.

Regards

Harshit

Disclosure: Not Invested

Financier Shriram Capital Ltd plans to merge two of its listed units with itself to help investors Piramal Enterprises Ltd and TPG Capital to easily sell their stakes in Shriram Group companies.

The plan entails merging Shriram Transport Finance Co. Ltd and Shriram City Union Finance Ltd with parent Shriram Capital to create a simpler shareholding structure, three people familiar with the plan said.

“We are looking at a few options like merging both the entities to the parent company and thereby listing it. Also we are still looking at an individual investor who can pick up the entire stake of Piramal and TPG. However, this is going to take a few weeks,” said R. Thyagarajan, founder of Shriram Group.

Kotak Mahindra Capital Co. Ltd has been hired to advise on the planned merger and shortlist buyers for Piramal and TPG’s stakes.

Emails sent to Shriram Capital and Kotak Mahindra Capital went unanswered.

On Friday, Ajay Piramal, chairman of Piramal Group, told Mint in an interview that the group’s planned exit from Shriram Capital was on track. “We are going through many different combinations, we have not yet decided. One thing is clear that we will exit. Which is the best way forward for Shriram, that we are discussing,” Piramal said.

Piramal bought a 20% stake in Shriram Capital for ₹2,014 crore in 2014. Piramal also holds 10% in Shriram City Union. Over the past few months, Piramal has been looking for a buyer for these stakes.

TPG Capital holds a 9.4% stake in Shriram Capital, while South Africa-based Sanlam Group owns 26% and Shriram Ownership Trust and Shriwell Trust hold 30.7% and 13.4%, respectively, according to a Crisil ratings report.

“The value of the stake in Shriram being planned to be sold by Piramal is quoted at ₹4,500-5,000 crore for the prospective buyers, which in turn will value Shriram Capital at around ₹25,000 crore,” one of the people familiar with the development said on condition of anonymity.

If the deal goes through, the proceeds from the stake sale will be used by Piramal to infuse capital into its lending businesses, repay debts of Piramal Group’s promoter entities and provide capital for organic growth.

Piramal had a 9.97% stake in Shriram Transport Finance, but in June sold this stake for ₹2,300 crore to several institutional investors.

The proposed three-way merger will result in the automatic listing of Shriram Capital, as Shriram City Union and Shriram Transport are both listed entities.

“Private equity firms and foreign sovereign funds have shown a lot of interest to buy stakes in Shriram Group from Piramal and TPG,” said the second person, declining to be named.

I started analyzing this recently and sense a historic pattern here :-

1990-91 :- Warren Buffett investment in Wells Fargo

During the U.S recession of 1990-91, California Real Estate market suffered badly. Wells Fargo, a conservative, well-run bank, set aside $1.3 Bill for future loan losses. Wall Street reacted as though Wells Fargo were a regional savings and loan on the brink of insolvency and in four months hammered its stock price from $86 down to $41.30 a share. Wells Fargo lost 52÷ of its per share market price because essentially it was not going to make any money in 1991. Warren responded by buying at an average price of $57.80 a share.

Based on 1989 financials, he paid an approx PER of 5 and P\B of 1.1. This was for a bank that had a 20+ ROE over previous 5-yr period.

Warren held WFC for the next 3 decades and is one of the prominent BRK holdings today delivering huge gains over this entire period.

Circa 2019-20 : -Shriram City Union Finance

Doing some reverse-engineering :-

SCUF is currently trading and consolidated P/B - 0.69 and PER of 4.

A well-managed, conservative, south-focused NBFC which got hammered due to major issues- 1) NBFC industry collapse 2) Stress in MSME segment to which they primarily lend to & 3) Lockdown due to COVID-19 pandemic

The market reaction seems to be factoring in almost zero earnings for 3 months and a write-off of around 1/3 of Book Value. Though the company might see a jump in NPAs in coming quarters, I believe the impact will be minimized due to 1) The co’s pre-dominant area of operations are semi-urban and rural areas, where COVID cases and impact in not that severe 2) Phased re-opening of SMEs already started & 3) The Co’s better access to liquidity due to its credit-rating.

Taking aside this period of stress, which I believe the company will be able to withstand, The co. earns a consistent ROE of 18-20% and should thus trade around 1.5 times Book Value. At present, it is available at 50% discount to that value similar to WFC case mentioned above.

So, is this a Warren Buffett type Well Fargo bet, or not?? Thoughts\views invited ![]()

Disclosure:- No holdings. Currently analysis in progress. While, I have mentioned the similarities in the 2 cases, I’m now looking for points where the 2 cases are not similar.

The data for WElls Fargo case study has been taken from books - Warren Buffett way, Buffettology and Inside the investments of Warren Buffett

The data points for SCUF have been taken from this thread, last years annual report and con-call transcripts.

This Company has a significant moat due to their team on the ground and processes that are hard to replicate especially on collections, origination etc. There is a great Ambit report on them, see that.

Also 20% of the book is for 2WL which should see big demand due to a move towards personal transportation.

Thanks @Puch. Have gone thru the moat and management checks for the company. To complete the analysis, however, I’m more specifically looking for counter-points - Why this investment is not similar to Buffett’s WFC investment mentioned above?

As always, Its the non-confirmation evidence that’s hard to find ![]()

![]()

Hi All,

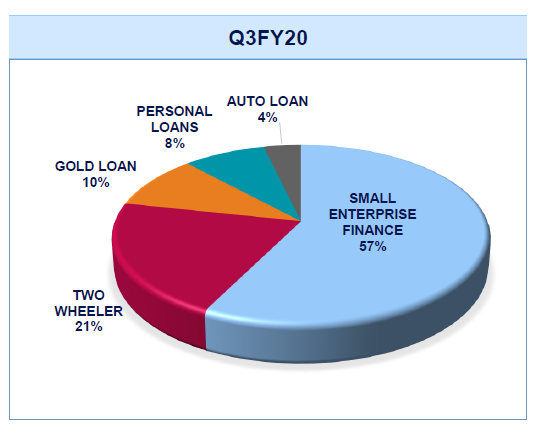

Earlier from the management commentary I found that they have around 1/4 th og their business in gold loan also.In this environment that seems to be a good business.But they wanted to decrease the gold business and increase the consumer business.Anyone knows how much is the gold loan book?

Thanks,

Deb

Hi,

The gold loan book is 23.8% of total loan book.

Which equates to about 6420 cr as of March 2019

Think you need to check your figures.

Q4FY20 Earnings Call Highlights:

Participants:

- ICICI Securities

- Motilal Oswal

- SBI Mutual Fund

- BOB Capital Markets

- IIFL Securities

- HSBC Asset Management

Business Overview:

- Disbursement at Rs 5,416 crore vs Rs 6,610 crore YoY

- AUM at Rs 29,085 crore vs Rs 29,582 crore YoY

- With the introduction of pre-owned 2Wheeler loans in FY20, disbursements in Auto Loans grew by 140% in Q4 on YoY basis and 65% in FY20 over FY19

- SCUF raised resources worth Rs. 3638 Crores in Q4

ConCall highlights:

- Shriram City Union Finance (SCUF) typically collects Rs 380-400 crore cash (only cash collection part) per month from customer; during April company were able to collect Rs 250 crore through digital mode

- SUCH has made Rs 426 crore provision for Covid. Company is hopeful that it will be able to write back 80-90% of that amount in coming years

- Transaction through digital mode jumped to 400,000 customer in the month of April from an average of 40,000 per month

- Collection during April was 34% and in May was 52%

- SCUF has collected total Rs 689 crore (ex-gold collection) during May; collection for gold loan business was around Rs 300 crore

- Company has started disbursement and in the month of May disbursed 50,000 2-Wheeler loan amounting to Rs 270 crore; industry volume was 240,000-250,000

- SCUF has disbursed 10,000 2-Wheeler loan in the first 10 days of June

- SCUF has also disbursed Rs 220 crore of Gold loan in May

- Company will start disbursing MSME loan from July

- Cost of fund for the quarter reduced to 9.35% from 9.71 on sequential basis

- Housing Finance: Disbursements at Rs 400 crore in Q4 were the highest ever despite the nationwide Lockdown. GNPA of 2.4% was the lowest in the last five years; made additional provision of Rs 10 crore in view of the impact of Covid-19

- Company not raised any money in April and May but has raised Rs 350 crore in June till date; liquidity position is very comfortable at over Rs 2,000 crore

- Quality of the personal loan book has improved in last one year; LGD has come down. In last one year entire personal loan book is built on existing customer base, those who have finished a loan cycle with the company. New customer base comprises 40% of total book

- 85% of SCUF’s book is secured; 80% of MSME book is collateralized

- Gold Loan: Company is currently offering gold loan in just five states. Yield is lower than pure play gold loan players

- SUCF will start gold loan business in 20-25 outlets in north India by end of June and by end of this year company will extend it to all 900+ branches. Gold loan LTV is 60%

- Company has not witnessed any deposit outflow in recent month; deposit rate is 8.25-8.3%. Net inflow in the month of April and May was Rs 113 crore and Rs 119 crore respectively

- As gold price increasing company has taken a little relaxed approach towards gold auctioning

- SCUF has also applied for moratorium from banks and received from HSBC, Indian Bank, Union Bank; the amount is very negligible

Hi Shardhr,

Hope you are doing well.Good comparison.I have a question here how you arrived that considering ROE around 18%,price should be 1.5 times of the book value?

In my view also the company will bounce back strongly in the pandemic and it seems its a great buy at this price,however I wanted your views of the long term story the company?

And also please share us your current views on the company as the situation has improved from the month of April.

Thanks,

Deb

The rule of thumb is that a Bank earning its cost of capital only sells at Book Value. Now, SCUF consistently has an ROE of 13-18% against cost of capital 8-10%(this is subjective). So it deserves a multiple of 1.3-1.6x Book Value. Nd it fulfills most of quality checklist criteria as well, so there’s no reason for it to sell 0.6x BV. Now, currently these factors are weighing in : -

- COVID hit SME lending segment

- Overall slow economy\NBFC crisis which was pre-COVID

- Piramal stake sale overhang

Mkt currently expects a huge write-off of its BV but as mentioned by u and mgmt commentary, the situation is not as bad as expected. The mgmt clearly stated that thr lending profile is mainly of traders whereas the COVID problem has hit mostly manufacturers. Meanwhile, it also seems they’re pivoting more towards 2W financing and Gold Loans.

Mgmt took some prudent calls over last 2 yrs which is serving them well. Also, its one of those reputed and not over-leveraged NBFC which will have access to capital in worst-case-scenario as well. So that’s margin of safety for you.

Considering Piramal’s fund raising , I dont think they’ll need this stake sale now and they won’t\shouldn’t anyways sell at this price  And as mentioned earlier, this situation is very much analogous to Buffett’s Wells Fargo investment. Study that in-depth for reference.

And as mentioned earlier, this situation is very much analogous to Buffett’s Wells Fargo investment. Study that in-depth for reference.

Disc : I’m holding it as part of statistically cheap undervalued Financial picks. I view this and 3 other Finance holdings as 1 stock and bet on Financial damage survivors.

Hi,

A pretty detailed article how MSME sectors are facing issue in this Covid Era.

It also highlights credit crunch as NBFC are in wait and watch mode instead of giving loans in the fear of them getting turned into NPA.

Thanks,

Deb

Hi All,

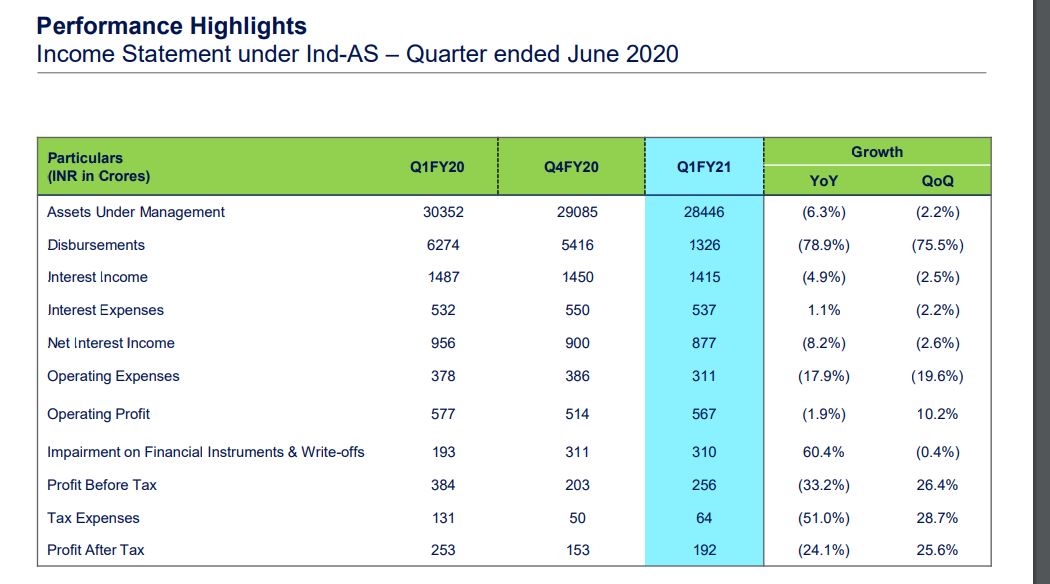

Results for the 1st quarter are out.

Below screenshot summarizes the results in a nutshell.In my view results are good considering the company mostly caters to MSME sector which is the worst sufferer in this pandemic.

I would have loved to see the loan book for Gold under AUM to increase but it is stagnant to earlier of 10%.Earlier it was a conscious decision for the management,not sure if they have the same stance now.

Result detailed can be found in the below link

https://www.bseindia.com/xml-data/corpfiling/AttachLive/2af76537-3ea6-48f6-ad02-894ceb554c4e.pdf

Disc:Recently picked up shares.

Please provide your views also.

Thanks,

Deb