Rating upgrade: https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/Shankara_Building_Products_Limited_September_05_2018_RR.html

1 Like

While i was going through screener couldn’t help but notice with it’s new feature on how the December buying frenzy was accompanied with very low deliverable quantity (red bars below)

2 Likes

No concall…fy19 q1…investors feeling spooky plus fpi sentiments. First support at 1000 and next support at 695. Heavy foreign holding selling and unreasonable valuations, margins took a dip.

Hi Amit, it appears they did conduct a con call. They uploaded the transcript on 5th Sept (which says con call was done on 16th Aug).

This is one of the stocks on my watch list considering the similarity with Home Depot. However, if the margin improvement with improving retail sale does not play out as it was initially projected, current valuation is also quite expensive.

In the concall, management said Q2 is seasonally weak. They also gave details of cash and credit sales, which I had not paid attention before.

Kotak gave FY19 estimated EPS of Rs. 44 in one of their recent reports. I fail to understand how it is possible given q1 was Rs. 8.5 and q2 is going to be weak.

Do you have any idea if they are moving ahead with the QIP? After Manpasand’s fiasco of raising QIP money just after a year of listing, Shankara’s QIP I think spooked the market and it has been falling since then. Let me know if you have any updates.

Regards

Kanv

300 Crores they are planning to raise from institutional buyers. For retail expansion.

There are a few red flags raised by Nitin Mangal. More details here (requires subscription). @aammiitt2 @diffsoft @varadharajanr

This stock has been hitting new lows regularly. Though I don’t own, I remember this being talked about almost as highly as D’mart. What has gone wrong?. Is anyone tracking this closely?

1 Like

It is not DMART…Comparisons would be just a waste. different business.

Kerala flood hit on revenue - Temporary

No pricing power - drag on margins

Slow down in Real estate, Infrastructure and construction activity.

South focussed

Future Expansion to North and other geos but then expansion comes at a further drag on margins and cost

Management is good and they are conservative in taking debt.

Valuations were overstretched and results were flat to little negative which causing the correction. Its a long term play and if you are after quick money this is not the counter for you. We are at the foundation laying stage of the business.

Disc: Remain invested. No change to holding.

4 Likes

Thank you for the insight. Remember Amanda buying around 1800 and averaging close to 1000. On radar. Waiting for it to stabilise.

3 Likes

Amansa has increased stake to more than 6% now according to latest stock holding pattern.

1 Like

Has anyone attended the concall or has concall transcript for q2 result? Notes?

Hi,

Though I do not track this closely, I came across this article a few days ago. Hope it might help you understand the reasons of downfall…

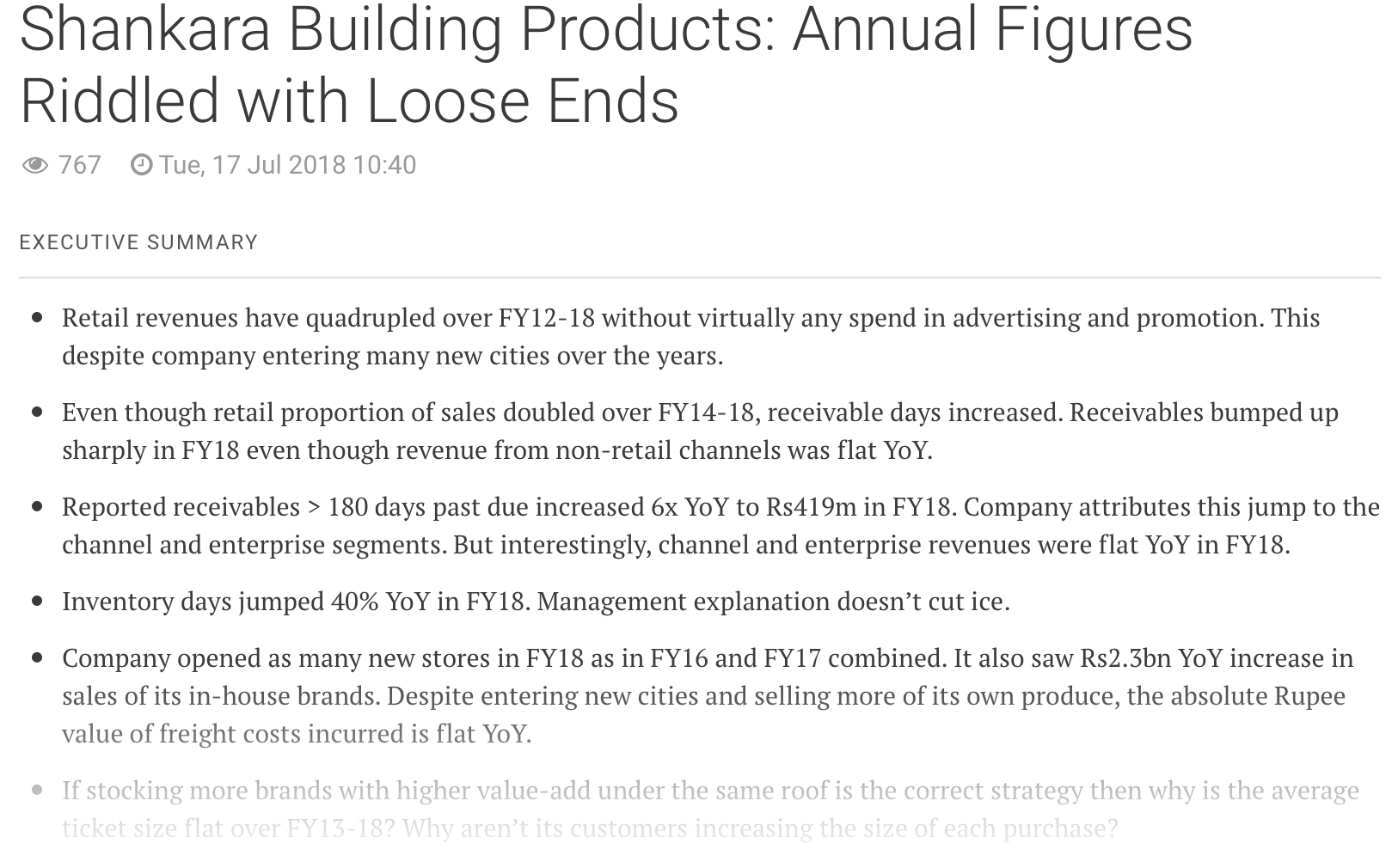

Shankara Building Products: Annual Figures Riddled with Loose Ends.

Read more: https://www.smartkarma.com/insights/shankara-building-products-annual-figures-riddled-with-loose-ends?utm_campaign=insight%2Bsharing&utm_content=sharing%2Blink&utm_medium=direct%2Blink&utm_source=direct

Regards

Can you please summarise the significant portion of the article if different from the executive summary?

Can’t afford to pay $7500 for subscription ![]()

Looks like a click and bait scam to me. It is ridiculous that someone charges $7500 for an yearly subscription.

2 Likes

It’s an institutional research portal. So naturally it’s going to be costly. Nitin Mangal is the man who took down India Bulls.

Important to note that Amansa added substantial quantity at very high valuation at least on near term earnings while Akash Prakash was complaining about very high valuation and lack of options during the discussion around Motilal’s wealth creation study. What is it that they see which Mr. Market is ignoring or rejecting so spectacularly? I personally failed to find anything great so far. It has halved since I included it in my watchlist.

1 Like

Well said. I too watched that video. In fact I have seen several smart investors complaining about valuation of quality companies( Which i agree) and ended up buying such businesses.

Coming back to this company, I never understand why this company is rated so high. Nothing special in the track record or product portfolio.

I guess this company has speciality retail in niche area of home improvements. If company can execute it opportunity size is huge. Besides it is convenient for consumers to buy their home construction solution from one shop then go to multiple shops for each items like paint sanitary ware steel cement etc which can increase bargaining power of the company from multiple brand vendors. Also unlike traditional retail rent cost is very small of less than 1 perc of revenue and ticket size is also higher than traditional retail shop. Also this retail segment don’t easily get affected by online retail players like Amazon or Flipkart’s of the world. As ndia has shortage of new homes and this company can capture all segment of housing and real estate without significant risk associated with real estate sector Also promoters have good predigree however in recent times some doubt about corporate governance issue has cropped in mind of some market players which is creating pressure on stock prices. Also company was trying to do too many things too fast which increases need for external funding and qip which further increasing market suspicion about corporate governance in the company. However my observation is even during ipo time money raised by company is just to give exist to investor and no money is received by company for growth etc so if promoters intention is not right they might have raised much more money into company in place of giving exit to investors.

4 Likes

SHANKARA - Announcement Under Regulation 30 (LODR)-Schedule Of Business Update Call https://t.co/LliO8BXz5p

Shankara Building Products is coming up with a business update call on Friday Nov 30th. Too much rumours have been floating around and management is looking to put them to rest. Let us hear to the management.