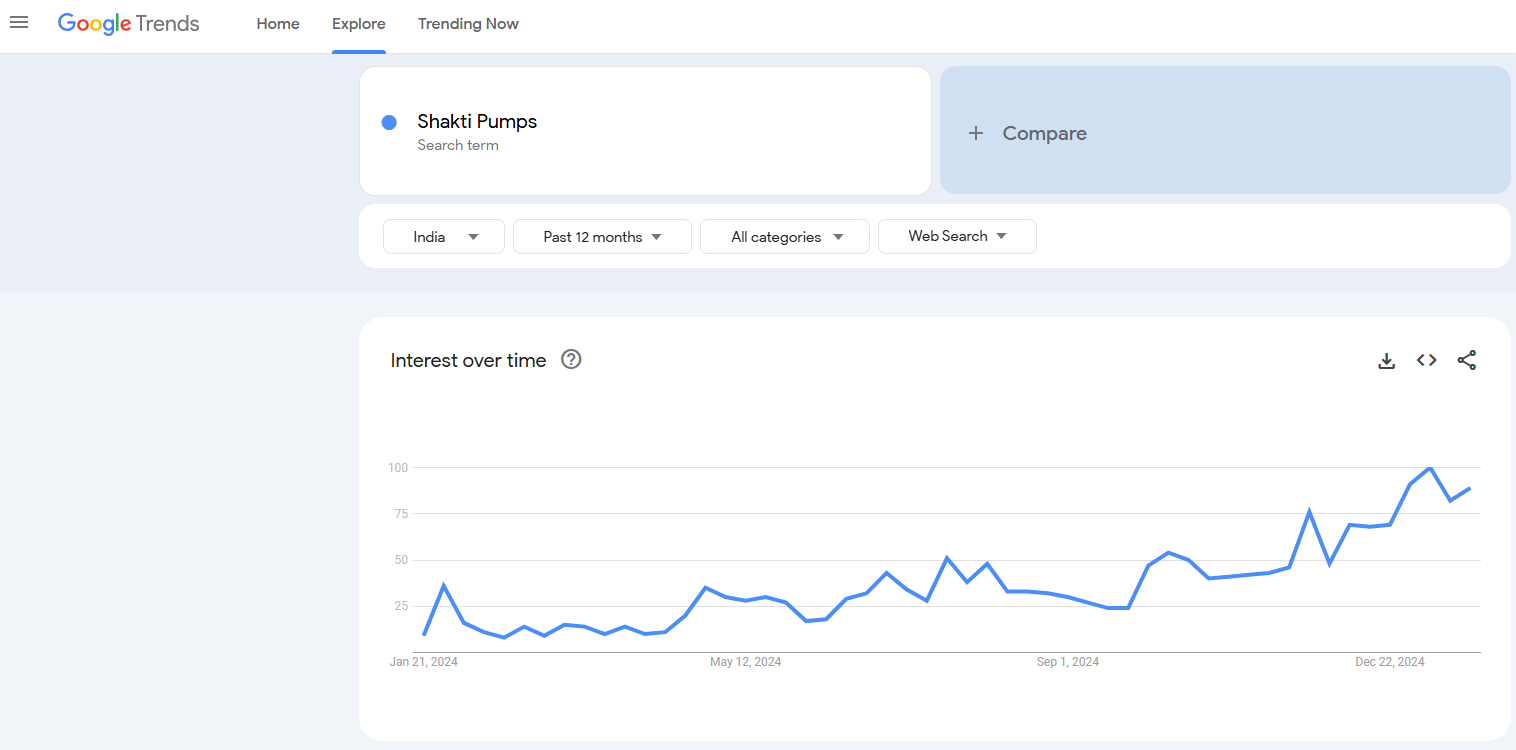

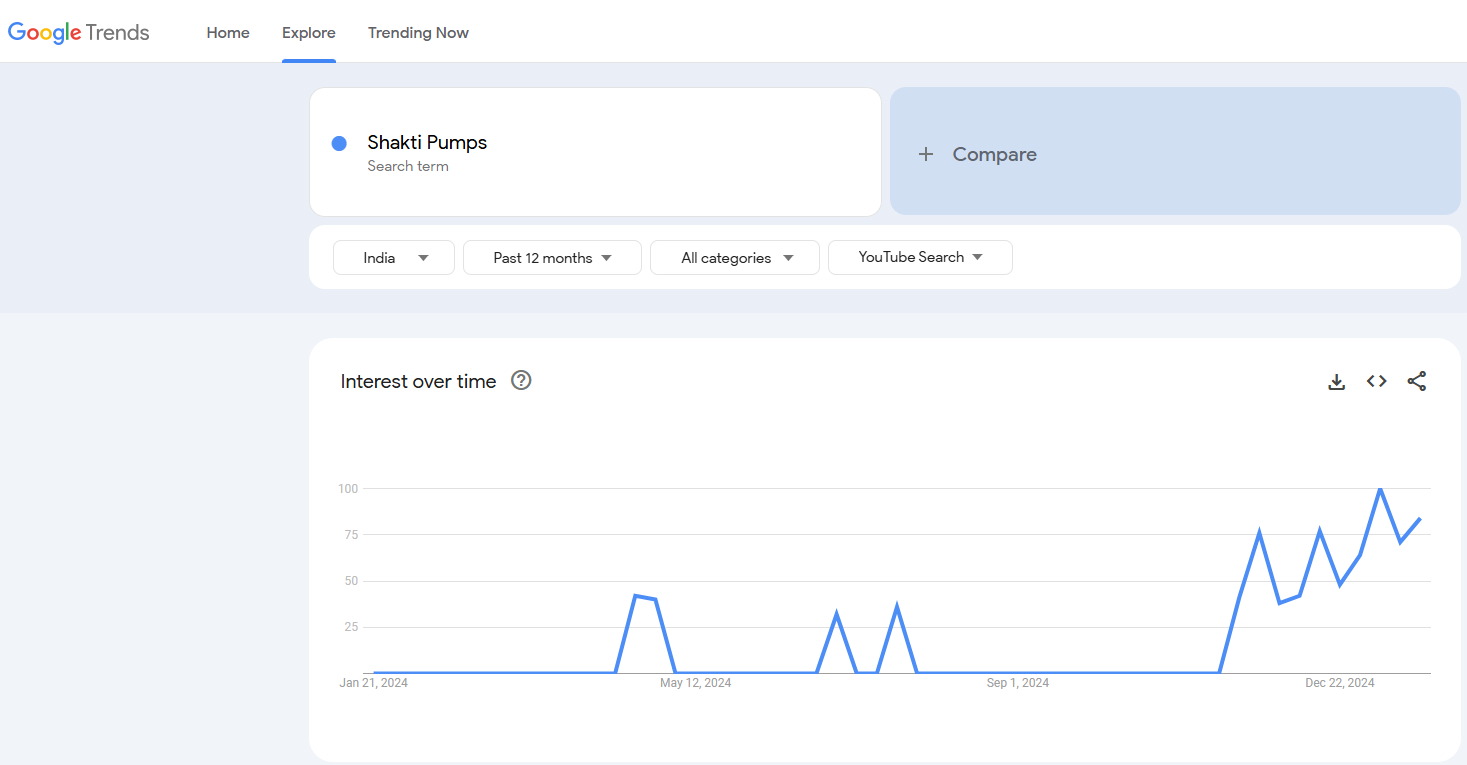

Near term triggers in Shakti pumps:-

-

In Q2 FY 25 earning call management has said that they wont let capacity contraint affect the growth. They said that within next 3 months they will be able to enhance thier annual sales capacity from 2500 crores to 3000-3200 crores just by adding few more machines in the existing facility.

-

Though they are giving a very conservative guidance of 500 crores for Q3, when grilled by investors, they accepted that this is the minimum guidance. They also said that last quarter they gave guidance of 500 crores but achieved 640 crores. Remember, last quarter was affected by monsoons. The way implementation of Component B under Kusum scheme is picking up pace along with rising orderbook, it is likely that Shakti pump may be able to reach quarterly sales run rate of 750-800 crores within next 2 quarters. That would mean quarterly bottomline run rate inching towards 125 crores if margin sustains.

-

Shakti pump board has approved capital raise of 400 crores. Last quarter P&L statement shows 11 crores of interest outgo, which corresponds to 300-400 crores of working capital loan. Balance sheet shows short term borrowings of 132 crores and other short term liabilities of similar amount. Managenent has also confirmed that they have approved overdraft facility of 1000 crores from banks for working capital requirements. Probably this capital raise will reduce interest outgo and further improve the bottomline.

-

Annual Indian budget of 2025 may increase the allocation for Kusum scheme because current Kusum project is very small compared to the total requirement of the agricultural sector. Many state governments may also start to allocate thier seperate budget for solarisation of agricultural pumps like Maharashtra.

-

Regarding comonent C, company said that currently they are facing challenges regarding connectivity of the grid in thier Ajmer pilot project but claims that they have a patented technology which will help them gain a significant market share in componect C in coming time. Management also said that true effect of component C will not come without replacing the pump. The payback period will only be 3 years if the pump is replaced othetwise it will be 20 years. If component C starts picking momentum, that can be a big opportunity because the market size of Compnent C is 2.5 times larger than component B.

Long term triggers:-

-

They have already raised 200 crores in March 2024 for a major capex which will enhance thier annual sales capacity to 5000 crores. The greenfield capex will go live in two years.

-

As per Shakti Pumps management there are 4.5 crore off grid pumps in India and similar no. of grid connected pumps. However, this no. appears too high. Most other sources states a total of 3.2 crore agricultural pumps in India. About 1 crore of them are still diesel operated and rest are electric. Solar pumps have just started getting traction. The benefit of solar pumps is so high that eventually it will end up becoming a norm. If we compare the size of opportunity to the current Kusum scheme numbers, it appears that this is just the beginning. This theme is likely to turn out into a decadal theme much beyond government backed Kusum.

-

Shakti pumps has incorporated a wholy owned subsidiary called Shakti EV mobility where they intend to manufacture EV motors, controllers, BMS and chargers. They have started sale to some of the manufacturers while testing is going on with others like Tata, Ashok Leyland, Eicher. Currently looks like a long shot but managenent is confident that by March 2025 the EV controller and motors anti-

dumping duty could be effected. That can change the game because currently majority of such parts are being imported from China. Management also said that recently they have been granted a patent for their ground-breaking invention of “Stack Assembly for Permanent Magnet Rotor”. This innovation is a significant advancement that promises to revolutionize the performance and efficiency of electric vehicles. This part of business may turn out to be be a huge optionality 2 years down the line.

Risk:-

-

The valuations are now on a higher side.

-

Current EBIDTA margins of 23% appears to be peak margins. Margins are likely to normalise after this theme matures and competition intensifies.

Disclosure:-

Invested from lower levels, but not part of core holdings. Currently 3% of portfolio. I have tried to mention all the facts and possible future outcomes as percieved by me. Just writing it for my own clarity, should not be taken as recommendation.