so present capacity is 5 lakh and 100 % utilization gives around Rs 2,500 crore top line and grossly realization per pumps set(including solar pv) would be Rs 50,000 !

if my calculations are correct then per pump realization is very low !!

can anyone throw some light on this would be helpful in my analysis!!

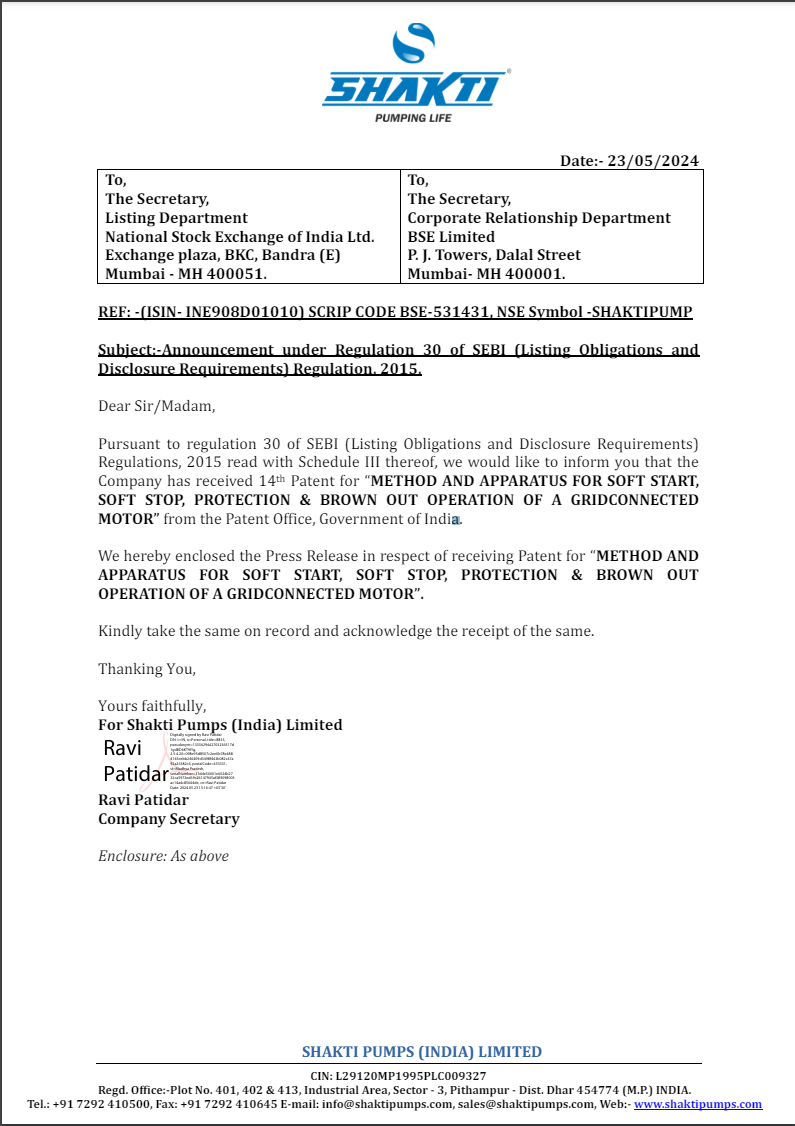

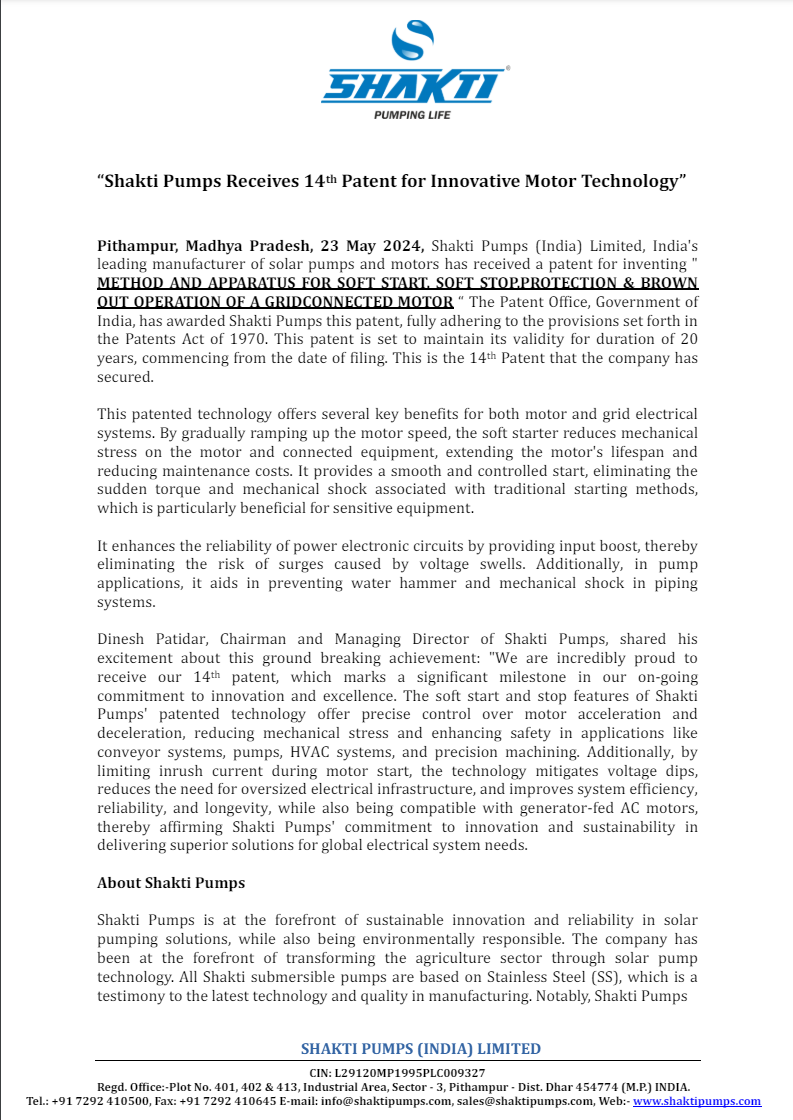

Shakti Pumps has been granted its 14th patent for a technology named “METHOD AND APPARATUS FOR SOFT START, SOFT STOP, PROTECTION & BROWN OUT OPERATION OF A GRIDCONNECTED MOTOR” by the Indian Patent Office.

This technology helps motors start and stop smoothly, reducing stress and maintenance costs, and preventing electrical surges and mechanical shocks.

Chairman and Managing Director, Dinesh Patidar: Expressed pride in receiving the 14th patent, emphasizing its benefits in various applications like conveyor systems, pumps, HVAC systems, and precision machining. The technology improves system efficiency, reliability, and longevity, and is compatible with generator-fed AC motors.

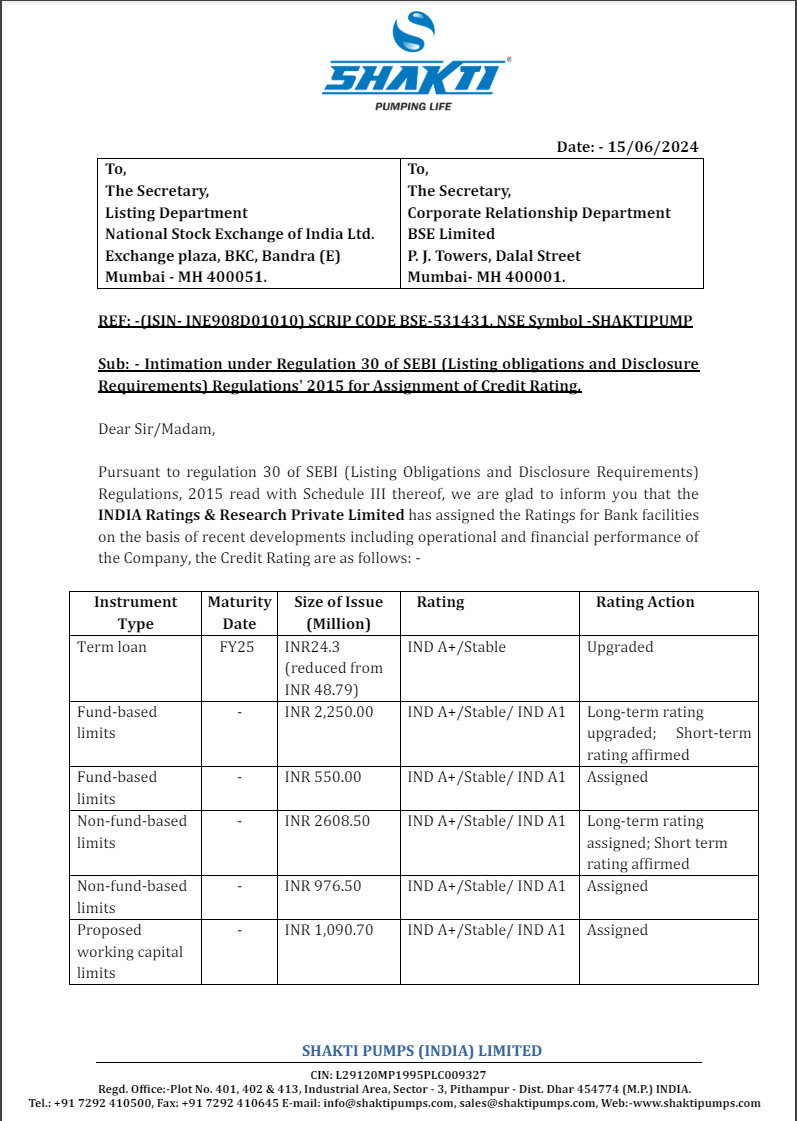

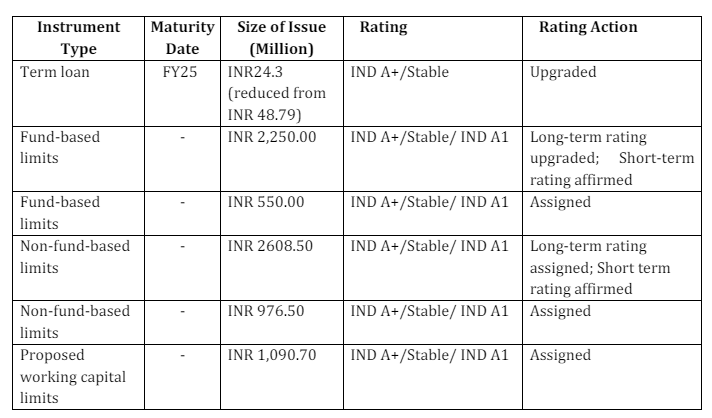

Credit Rating Assignment: Shakti Pumps has received updated credit ratings from India Ratings & Research Private Limited based on recent operational and financial performance. The ratings for various bank facilities are as follows:

Management had guided for 30% revenue growth. Not sure where this 3000cr number is coming from. Even in the investor ppt they claim to exhaust the current 2000cr orderbook in 15 months. By your projections they will do 2400cr+ in next 9 months.

Projections should be backed by logic and when they are against what management said, should accompany caution and disclaimers. Very irresponsible statements.

On YoY comparison, Company posted 1 Cr profit last year and this year it posted 93 Crores Profit, still you expecting 30% growth only ? Don’t you see management is very conservative in providing guidance, as latest blockbuster results shows company already passed the 30% growth projections, plz go through govt website https://pmkusum.mnre.gov.in/#/landing and pull all data on solar pumps installations across different states and consolidate than you will get to know the huge total addressable market potential for shakti pumps.

Shakti Pumps - Potential

Comp B - 9.57L pumps remaining

Comp C - 35L pumps So total - 44.57L pumps and cost of each pump is 3L.

Total mkt size - 1.33L Cr

Shakti mkt share - 25% of 44L - 11L pumps in 5-6 yrs -

33K Cr or higher Rev potential !

Feel free to make projections and speculations but state so explicitly. I see you have now edited your posts. I 100% agree that management is conservative but saying company will make 3000cr this year without backing it up with any source or saying that this is your thinking, is what i objected to.

If you don’t agree with below data, Why don’t you pull data by yourself and show everyone that this are incorrect projections ?

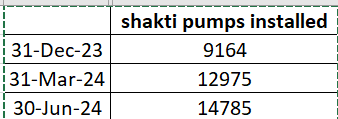

Shakti Pumps Q1 revenue excellent. PAT margin improved to 16.3% vs people expecting EBITDA to be 15%. From solar pumps installation data we got 16001 pumps installed in Q1. Co installed 14785 pumps as per their own investor presentation.

So no of pumps installed is more even QoQ. B2G is their highest revenue earner. Means q1 should be higher than q4. But it didn’t happen? Really (all doubters will run away now) Lets’ compare their 2 investor presentations only. Anyone can do this comparison from the investor presentations.

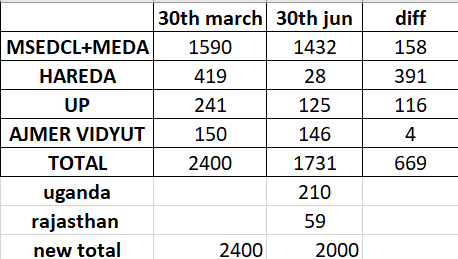

Difference of orderbook between 30th march and 30th june. Only 4 agencies MSEDCL, HAREDA, UP AJMER VIDYUT shows that 670 crores of orders already executed in Q1. On top of this, the export for full year in FY23 was 286 crores so 70 crores per quarter. This quarter declared is just 22 crores. And add the B2B vertical which in Q4 was 130 cr. Add all of these and you would know how much revenue was generated in Q1. Exports aur B2B ko side bhi rakh do. Just the difference of their govt orderbook executed in Q1 is 670 crores.

Bottomline. Expect q2, q3, q4 to be even more blockbusters.

For full year yahi aayega, 3000 cr revenue,

600 cr pat

300 eps available at just pe of 13 vs KSB at 74.

Ajmer Comp C pilot project should get over in next 2 quarters. It will help all stakeholders to learn from this pilot project and move forward with expanding it to the wider audience.

Ajmer project includes solarization of 200-250 feeder pumps. So their capability is good for both Individual Pump Solarization and Feeder Level Solarization.

Shakti Pumps seems to be having an edge in Comp C through their patent. Their technology allows the system to transfer solar energy (electricity) to the grid automatically post pump has been used to draw the water. Where as, according to the management, for competitor’s grid connected solar pump, a human has to go and flip the switch to start the transfer of solar energy (electricity) to the grid. This can be a strong competitive advantage for farmers to choose only Shakti Pumps for their Comp C investment.

Tendering process for fixing solar pump prices are completed with 5 more quarters to go before next round of tender bidding starts for next leg of Comp B. So there is good chance that windfall margins might continue for next few quarters if solar panel prices remain subdued. There is good chance that to bid competitively, management might bid at lower prices and effectively we should see 16-17% kind of EBITDA from H2 of FY26.

New capacity to go live from FY27.

One thing which I am not able to digest is that management has guided 30% growth in FY25. So that means about 1800cr topline. Management has already guided for 500cr in Q2. Bringing total to 1070cr for H1FY25. This leaves about 360cr in Q3 and Q4 which would be very poor Q3 and Q4 given current strong tailwinds in Kusum scheme. Either management is being super conservative or there is something that management is hiding from investors.

Disc: invested with no transactions in last 30 days.

There seems to be an allocation of 2 lakh pumps (grid connected) under Kusum C scheme in the budget. The company claims that they only have technology for this (patent). The pilot is undergoing in Ajmer. If this means that 100% allocation of this will go to Shakti Pumps then it is huge.

In case anyone has more information towards this, please share.

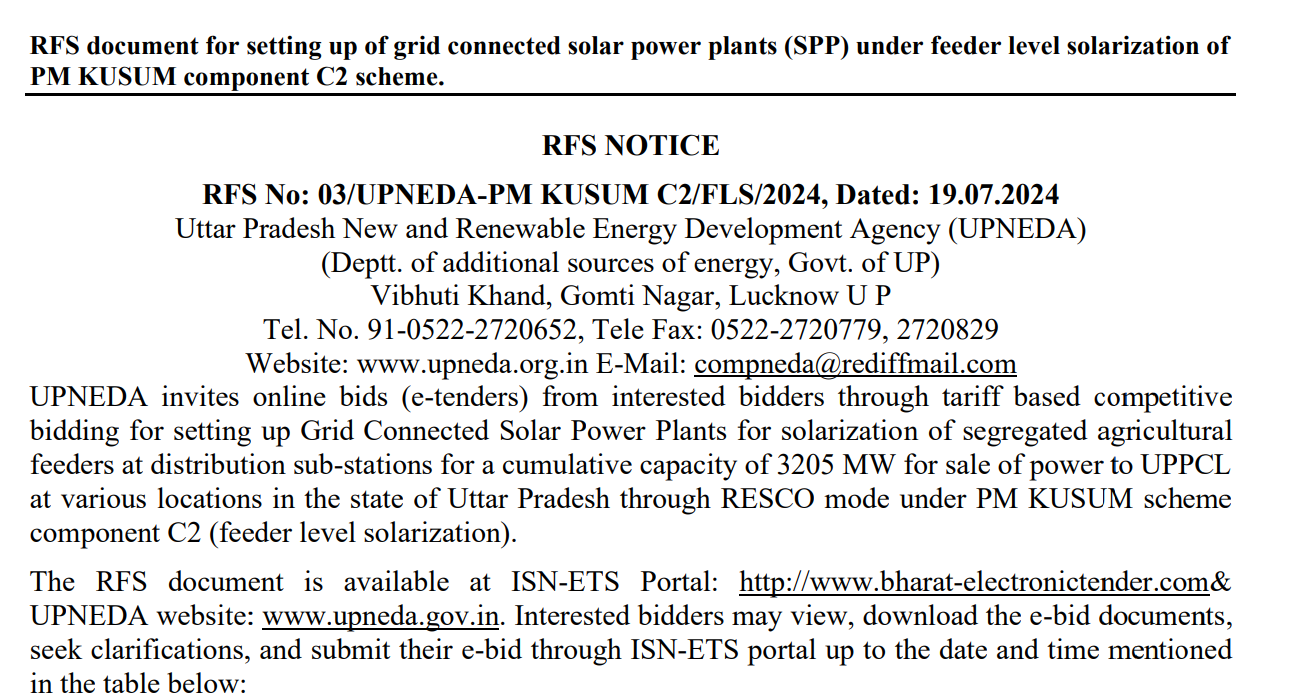

Also, found one more tender which is currently open in UP for Component C2 (feeder level solarization) with cumulative capacity of 3205 MW. Setting up one MW would cost around 4cr. So total tender size is huge but we would not know how many total feeders are supposed to be solarized to assess the size of scope for Shakti Pumps. Its good to see activity in Component C here.

Shakti Pumps has secured its first order from the state of Uttarakhand under the PMKUSUM scheme.

The company has been awarded a contract worth approximately Rs. 8.5 crores to supply 200 solar-powered water pumping systems to the state’s Minor Irrigation Department.

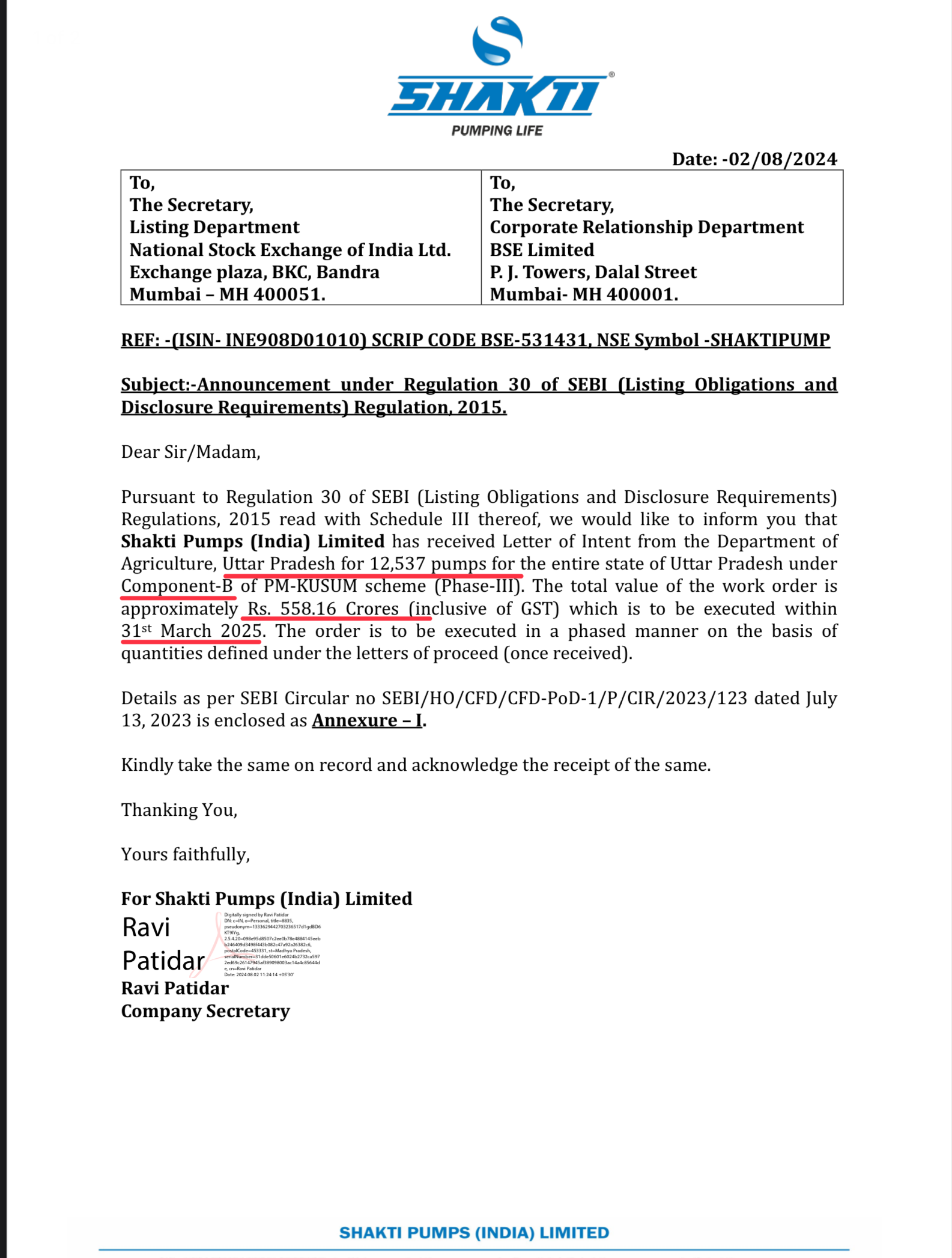

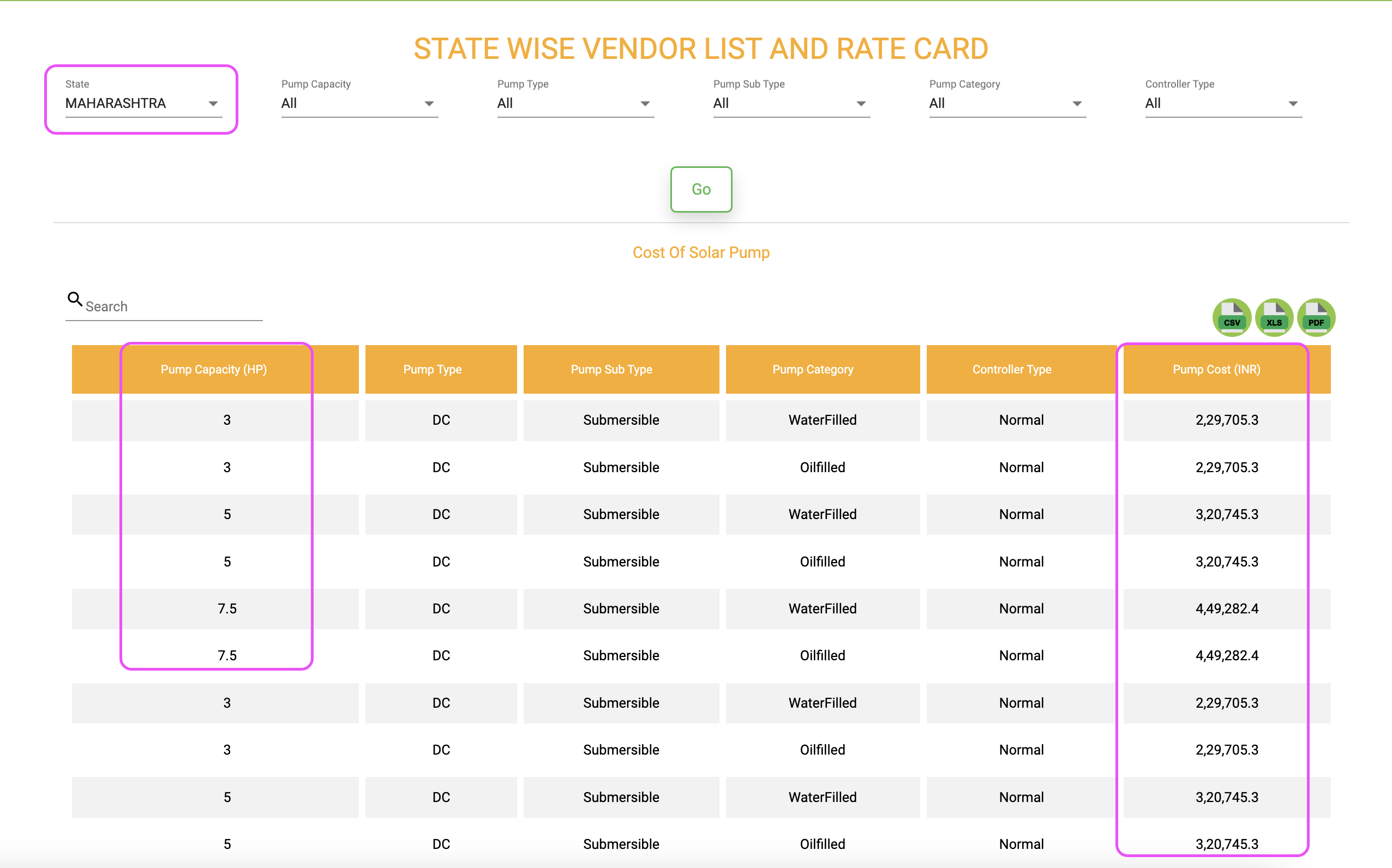

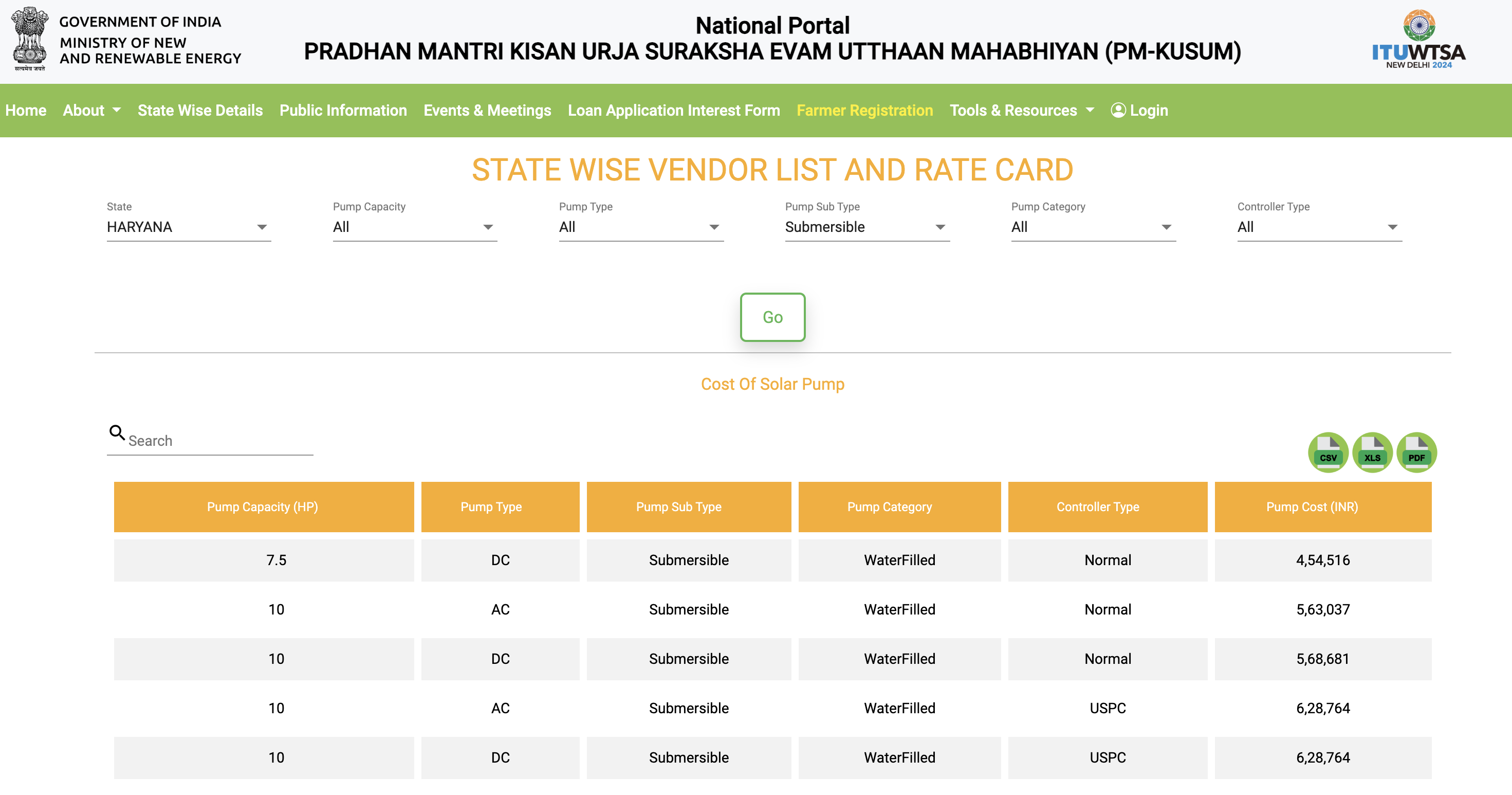

Can someone help me understand why the per-unit solar pump rate varies significantly across different tenders? For instance, the rate is INR 45 lakhs per pump in some cases, while it’s INR 35 lakhs in others, as seen in the three examples: INR 33.5 cr for 1,200 SPWPS pumps in Maharashtra, INR 8.5 cr for 200 SPWPS pumps in Uttarakhand, and INR 558 cr for 12,537 pumps in UP.

New tender has been floated by Punjab Renewable Energy Development Agency for solarization of 75000 grid connected pumps under feeder level solarization of Component C. The scope of work involves providing Remote Monitoring capability for the government agencies to the solar power plant.

If it was a straightforward component B tender - rough tender size would be in ballpark range of 1800-1900cr for 75000 pumps. But I will not be surprised if the size of Component C order for 75000 pumps is much higher than 1900cr because it is more complex with many parties involved.

Its nice to see the movement in Component C space for PM Kusum Scheme, but would be skeptic until the execution starts happening at the ground level for Component C.