The letter is about Shakti Pumps receiving its 6th patent for a technology related to “STACK ASSEMBLY FOR PERMANENT MAGNET ROTOR.”

Key Details:

Shakti Pumps has received a patent for their innovation related to electric vehicle (EV) motor technology.

This patent will be valid for 20 years.

This is the 6th patent the company has received.

Impact of the Innovation:

The technology improves the efficiency of electric motors used in vehicles, leading to better energy conversion and longer driving range for electric vehicles.

It reduces energy losses in the motor and improves power factor, making the motor more efficient.

Lower operating temperatures of the motor can extend its life, reduce maintenance costs, and increase durability.

The innovation also enhances the motor’s load capacity and torque, making it more powerful and versatile.

About Shakti Pumps:

Shakti Pumps is known for its sustainable and reliable solar pumping solutions.

They are committed to transforming the agriculture sector with their solar pump technology.

The company manufactures products like solar pumps, motors, structures, controllers, and VFDs.

Shakti Pumps is focused on helping India meet its energy goals and promoting sustainable transportation.

In simple terms, Shakti Pumps has received a patent for an innovative technology related to electric vehicle motors. This technology makes electric vehicles more efficient, increases their range, reduces energy waste, and extends the life of the motors. It has the potential to make electric vehicles more practical and reliable, contributing to sustainable transportation and reduced reliance on fossil fuels.

Can any body who has technical know how advise regarding the significance of these patents and potential products or revenue which Company can generate in future or outcome of theses patents vis a vis existing technology…

Shakti Pumps (India) Limited, a company that makes energy-efficient pumps and motors, has been granted its 7th patent by the Government of India. This patent is for a “Grinder Pump Assembly with Adjustable Impeller.” The new technology helps grind and process solid waste in wastewater more efficiently. It reduces the size of solid materials, making them easier to manage in subsequent treatment processes. This innovation is valuable for wastewater treatment and various industrial applications, as it minimizes blockages and maintenance costs.

Shakti Pumps Chairman, Mr. Dinesh Patidar, explained that the technology effectively prevents blockages in wastewater lines caused by solid waste, reducing maintenance needs and operational downtime. The company is known for its solar pumping solutions and environmentally responsible practices, serving the agriculture sector and manufacturing its own products. They are committed to helping India achieve its energy goals.

In simple terms, Shakti Pumps has received a patent for a new technology that makes wastewater treatment more efficient by grinding solid waste, reducing blockages, and cutting maintenance costs. This technology is valuable for various industrial applications and aligns with the company’s focus on sustainability and innovation.

Shakti Pumps has renewed the recognition of its In-House Research and Development (R&D) Unit(s) by the Department of Scientific and Industrial Research. This renewal is valid until March 31, 2026. The company had initially received this recognition in 2018, and it was extended until March 31, 2023.

Shakti Pumps Limited, a prominent manufacturer of stainless-steel submersible pumps, pressure booster pumps, pump-motors, controllers, and inverters, released its financial results for the quarter and half-year ending on September 30, 2023. The company’s Chairman, Mr. Dinesh Patidar, highlighted the significant achievements and developments during this period in a letter addressed to the Listing Department of the National Stock Exchange of India Ltd. and the Corporate Relationship Department of BSE Limited.

The key points from the letter and the financial results are as follows:

Key Developments:

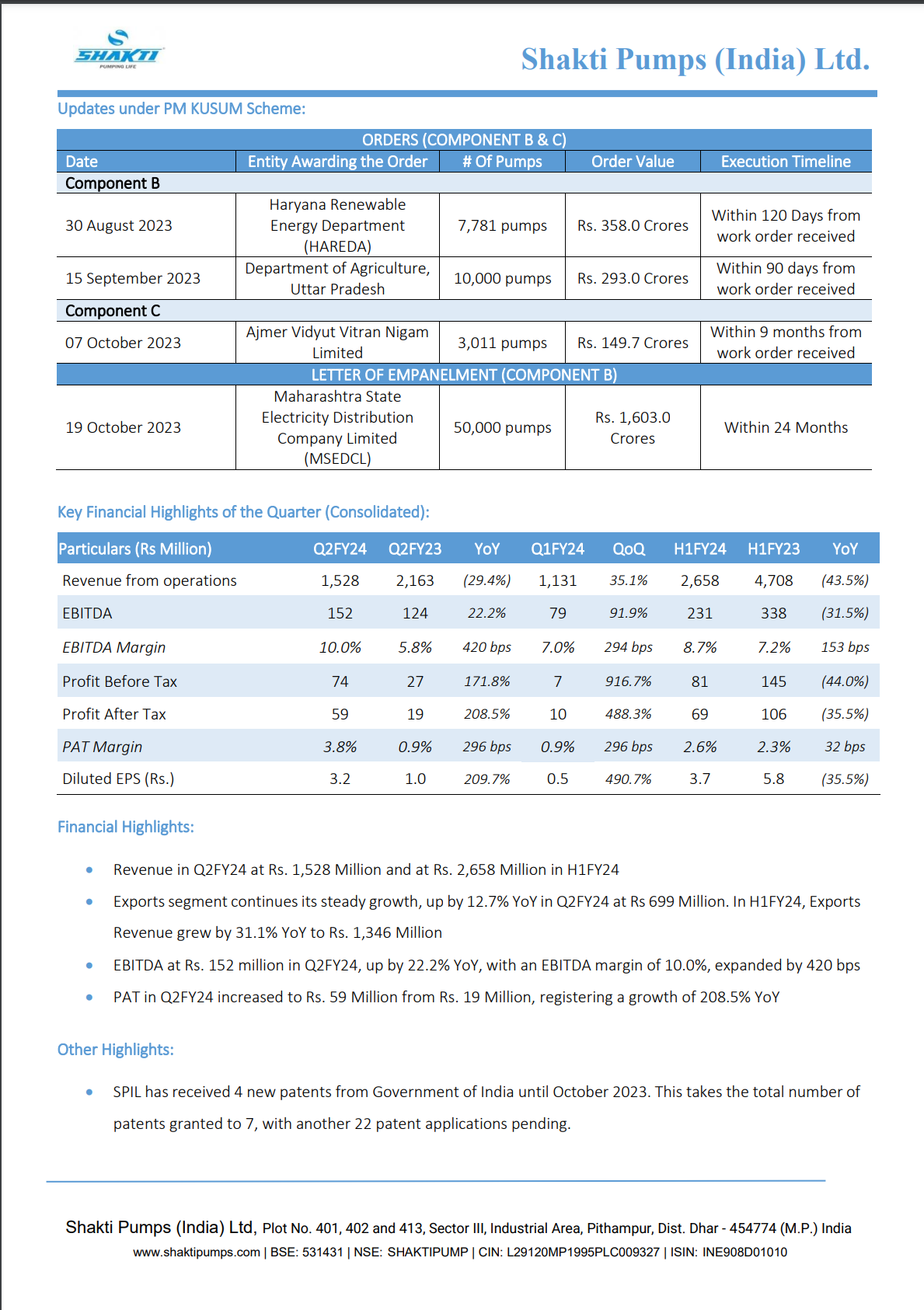

Shakti Pumps received notable orders under the PM KUSUM III Scheme:

Two orders for 17,781 Off-Grid Solar Photovoltaic Water Pumping Systems (SPWPS) worth Rs. 651.0 Crores from Haryana Renewable Energy Department and the Department of Agriculture, UP.

A Letter of Empanelment for 50,000 SPWPS pumps amounting to Rs. 1,603.0 Crores from Maharashtra State Electricity Distribution Company Limited.

The company also received its first order under Component C from Ajmer Vidyut Vitran Nigam Limited for the implementation of 3,011 Grid Connected Solar Water Pumping Systems for Rs. 149.7 Crores.

Shakti Pumps demonstrated its commitment to innovation by securing four new patents, taking their total patent count to seven. One of these patents relates to their innovations in the electric vehicle (EV) space, where their subsidiary, Shakti EV Mobility Pvt. Ltd., is making progress. The company board has approved an investment of Rs. 114.29 Crores over the next five years in this subsidiary, anticipating growth in the EV industry.

The current surge in orders is expected to drive a business upturn in the second half of FY24, with additional orders from various states expected to support this trend.

Financial Highlights:

Revenue from operations in Q2FY24 was Rs. 1,528 Million and Rs. 2,658 Million in H1FY24.

The exports segment showed steady growth, with a 12.7% YoY increase in Q2FY24 at Rs. 699 Million. In H1FY24, exports revenue grew by 31.1% YoY to Rs. 1,346 Million.

EBITDA for Q2FY24 was Rs. 152 million, representing a 22.2% YoY increase, with an EBITDA margin of 10.0% (expanded by 420 basis points).

Profit after tax (PAT) for Q2FY24 increased to Rs. 59 Million from Rs. 19 Million, a growth of 208.5% YoY.

Other Highlights:

Shakti Pumps has received four new patents, bringing the total number of granted patents to seven, with 22 patent applications still pending.

The company has approved investments of Rs. 114.29 Crores in Shakti EV Mobility Private Limited, involved in manufacturing EV chargers, motors, and controllers.

The Recognition of In-House R&D Unit(s) from the Department of Scientific and Industrial Research has been renewed until March 31, 2026.

In summary, Shakti Pumps reported a successful quarter and half-year with substantial orders under the PM KUSUM III Scheme and advancements in technology, including patents and investments in the EV industry. The company anticipates a strong business upturn in the coming months.

Management clarification about Maha order. Huge in my opinion

Edit: further management guided for 400cr and 500 cr revenue in q3 and q4 with full year ebidta margin @12% . So PAT should easily be 80cr+. That bring FY24 pe to around 23. So further rerating should happen in my opinion since there is visibility for fy25 as well.

12% ebidta margin for full year meams that company would need to exceed margins by 12+ for next 2 qtrs which would be interesting to see

Haryana orders can come next month…more clarity is required on Maharashtra orders.

Disclosure: Invested but trimmed my positions as there were other good opportunities in the market and now waiting for reflection of narratives in numbers.

I think it is clear from the con call that for this 50k pumps, shakti will going to be sole supplier and for that portal is getting ready. Otherwise management would have stated it in con call.

My view is that this is old analysis. And you can’t really find integrity anywhere if you look hard enough. The company has been doing a lot of investors presentation and meets right now, so don’t think there should be obvious red flags at the moment. With that being said i am fairly new and have minimal knowledge of financial shenanigans. Invested