On what basis? Have you checked their plans? I think they would have to go a long way to sustain the current prices. The equity dilution over the last 18 months has been humongous.

if lasa is listed on 140 currently 156 why sequent is at low price , can someone throw some light in comparison

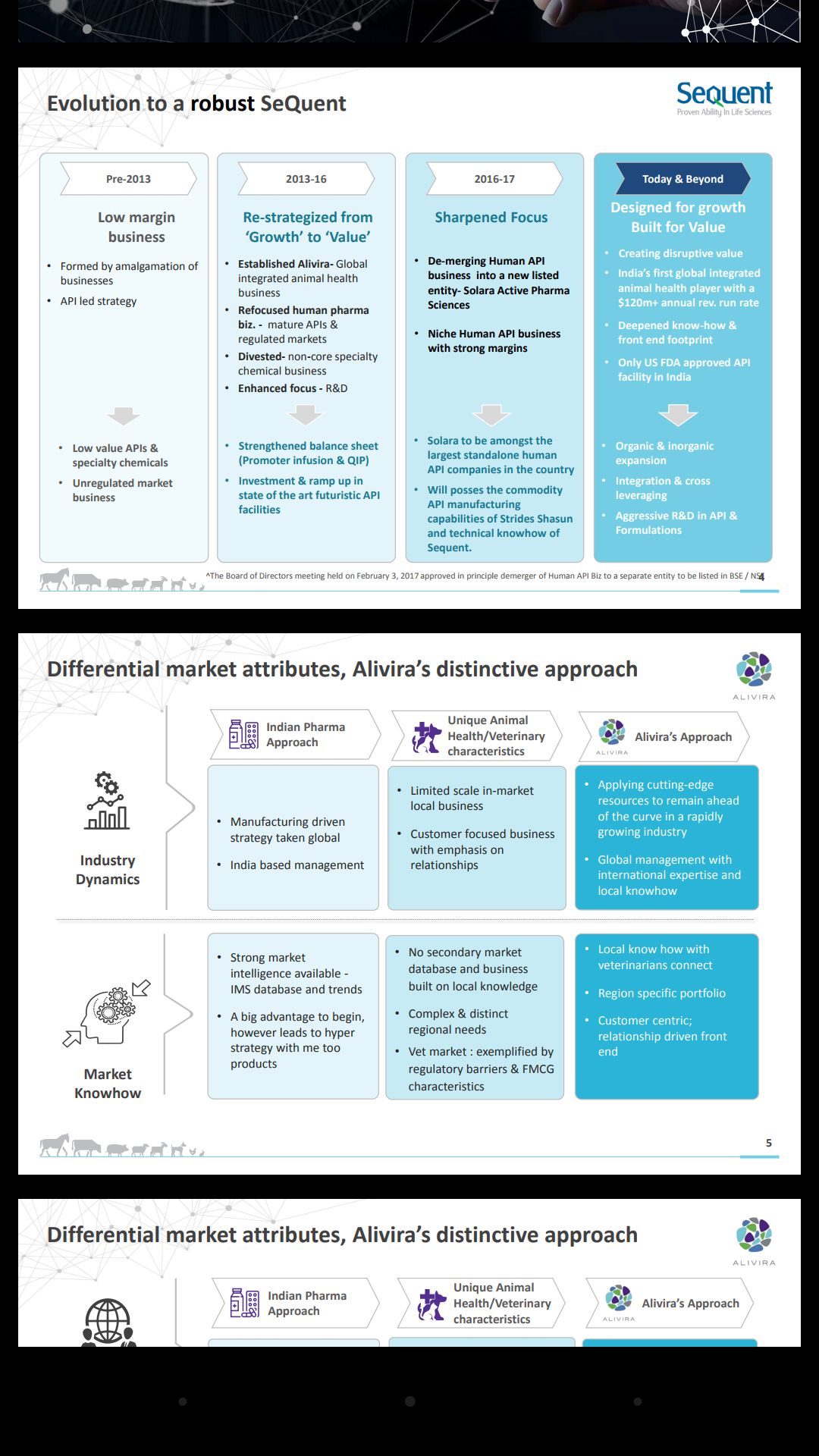

Sequent is due to de merge its Human API business and list it independently along with carve out from strides. Management has been active over the last few years on acquisition spree but this year has been very subdued. Looks like they are focussing on the vet biz going forward. Top line is not bad however EPS is very lacklustre and they need to do a lot to improve the margins. I would say even a the current market price which is almost a 60 percent drop it looks quite richly valued. I remain invested for Long term. Perhaps post de merger management will be able to drive growth in the animal health biz.

1 Like

I learnt it the hard way that estimating what Arun Kumar will do next is waste of time and has opportunity cost. One has to think like a PE investor while investing in this promoter group. Was lucky to make some money here.

Disc: No holding

1 Like

The worst seems over. I believe the NCLT meeting for demerger is next week. If approved this might be a trigger for short term buying at least. Does anyone know if production is running at capacity and if any additional capacity will come onstream and what would the impact on profits?

Another positive is the QIP investors who subscribed at about 107 rs per share post split?pls correct if im wrong. It has been over few years since and would be due for a return as well.

Besides these points would be helpful if management is more robust.

2 Likes

As per AR 2017, both CFO and CS resigned on Feb 10, 2017. Any idea why both resigned on same day?

Disc: No holding.

1 Like

I think they took up different position with promoter group. Their departure is immaterial.

Problem is the biz going forward. Earlier post i stated worst is over, however i may take another step back.

What happens to the already fragile eps post demerger?

Even i see red flag in disinvestment of ‘Nari Pharma’. It was acquired in March 2016 with Goodwill payment of Rs 4 crores. During 2016-17 there was lot of investment in the company. Borrowings increased and loss of Rs 17 crores incurred and surprisingly within 1 year they are finding it not related to company and now planned to sell it to a promoter company.

1 Like

Great Point. Would you consider it a buy at CMP? I am now a bit anxious how long it will take to grow the Animal biz. The counter may lose further value or stagnate for a few quarters before EPS growth. What if there are losses? The stock is already quite richly valued trading at 3 x book value.

Sequent constantly losing value of late. This week has been tough with the strides result slippage. Result both have been hammered.

Have a decent holding but do not have the conviction to buy more as a contra bet.

Planning to meet the CEO post Q2 results on 9th Nov. Will pen down my thoughts.

Disc : Invested from 2013 (at different levels).

good! can you please ask them one thing. will they ever stop M&A and start working on whatever they have. I have lost count of assets they sold, demerged or acquired.

2 Likes

Sure, I will certainly do that. In fact if you have more questions pls let me know. I will pen them down and ask Manish Gupta.

They are 3 broker meetings post Q2 board meeting on Nov 9, hosted by axis, icici and idfc respectively.

The results seem to be good. Operational performance is coming back…Why are we at a 52 week low?

I had a good meeting with the CEO Manish Gupta today. Despite the hammering on the share which has been punished severely over the last few years for different reasons, i am optimistic for the short to medium term at least. Beyond that I am wiling to stay invested for 3-5 years depending on how their animal health business plays out.

Some key observations -

- Q2 results were good and EBITDA positive. This may not reflect consistently as Sequent may enter a new country and lose money for a while. Hence we may seen inconsistent margins.

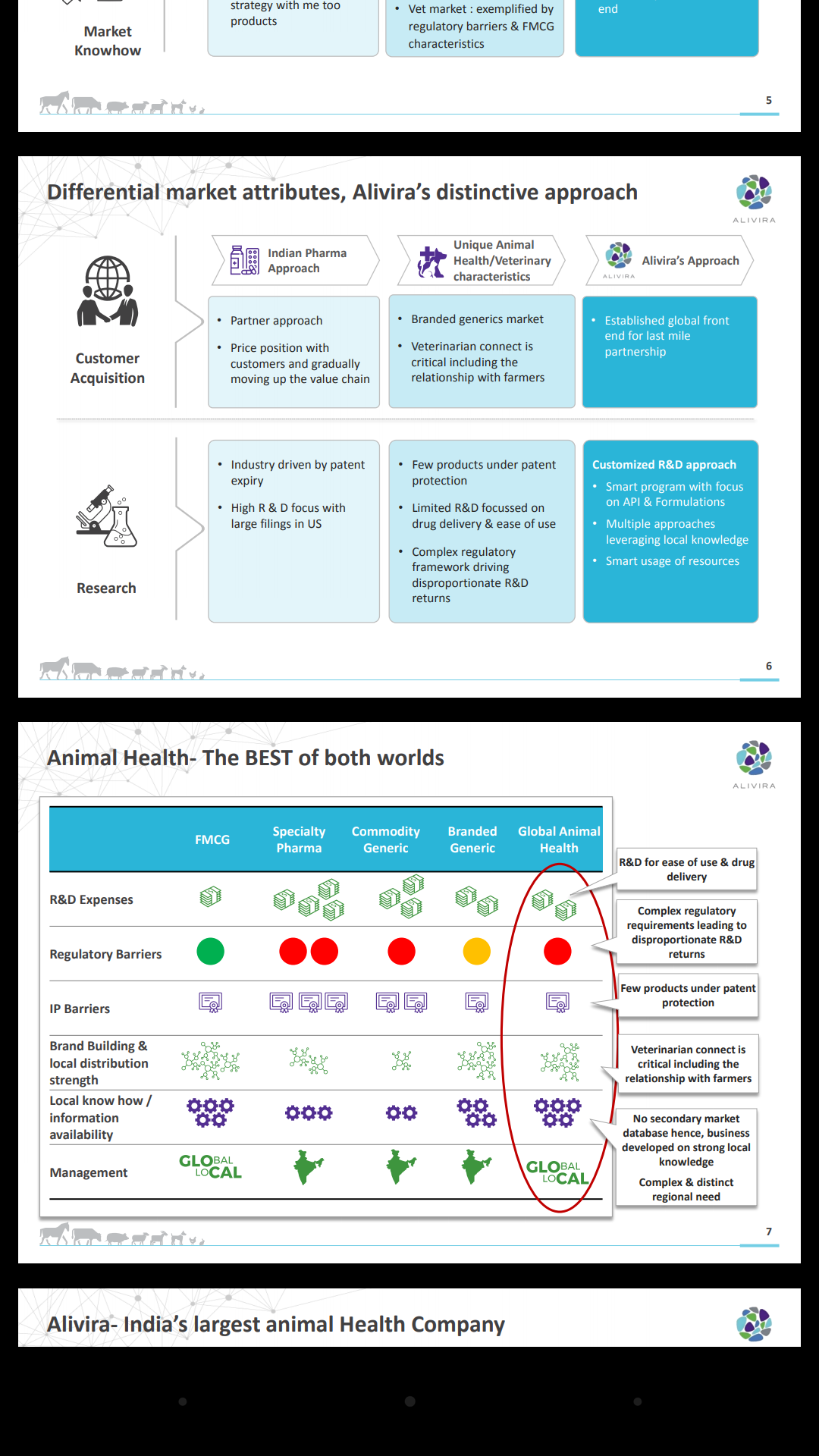

- Animal health biz revenues are growing steadily in India.

- there is no real competition in India. Sequent is the only pure play animal health. Hester and Lasa are not in the same sector and not comparable.

- professor Mankekar exited Sequent as well as Strides. These were 2 laggards in his portfolio and after few years of negative returns he has sold his stake.

- performance is actually better than the current valuation (For the first time!)

Would i buy at CMP?

Yes, i am convinced to add more to my holdings asap. I feel the demerger entity has huge potential (Solara) and value is not embedded in the price. Therefore, i expect significant upside from CMP 100 in the short to medium term. In the longer term i would like to see consistent margins and profitability and only then can it would be potentially become a multibagger.

3 Likes

Dears,

I look all past message and try to evaluate “Sequent Scientific” with past and current performance…

Current performance:

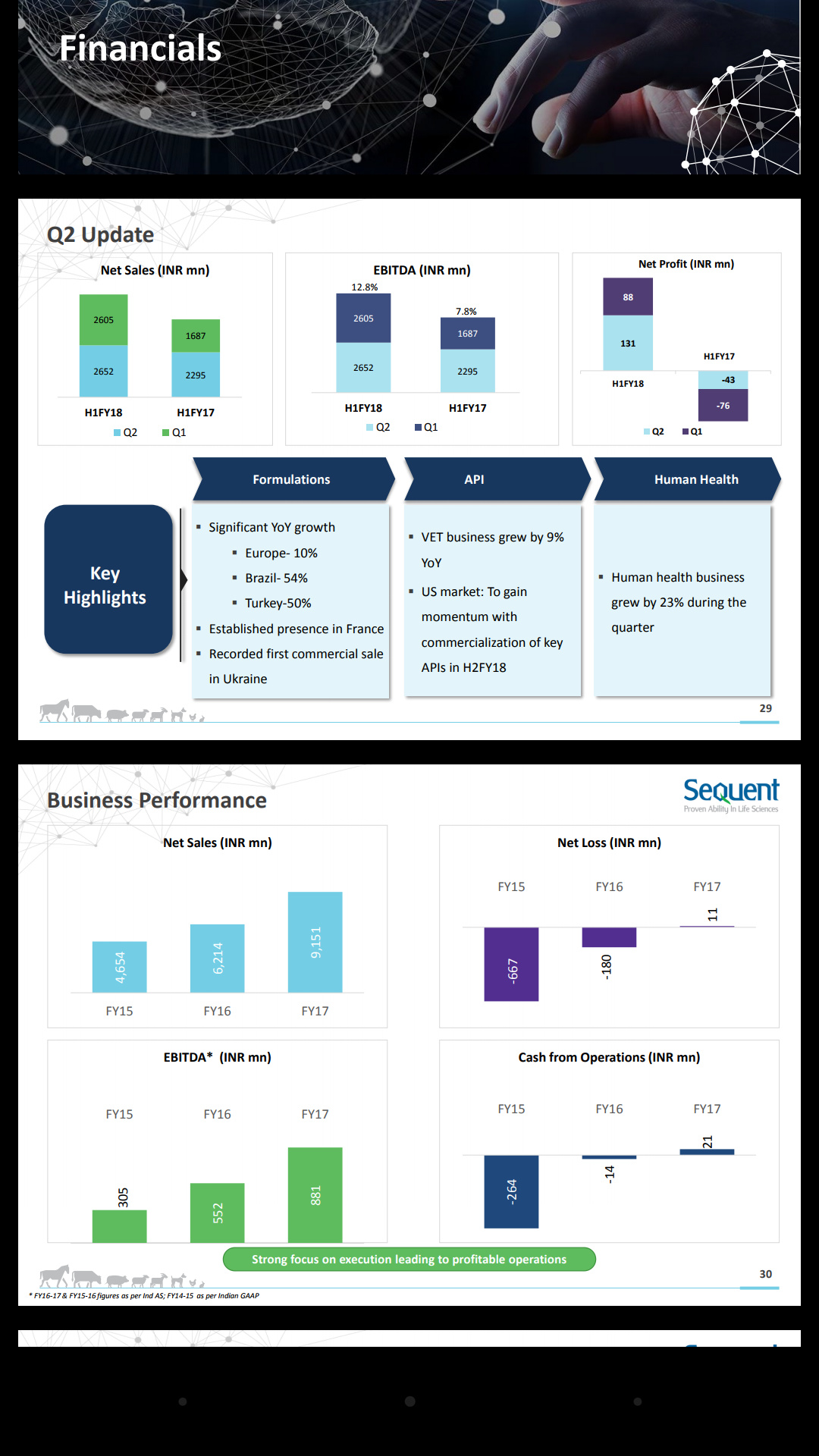

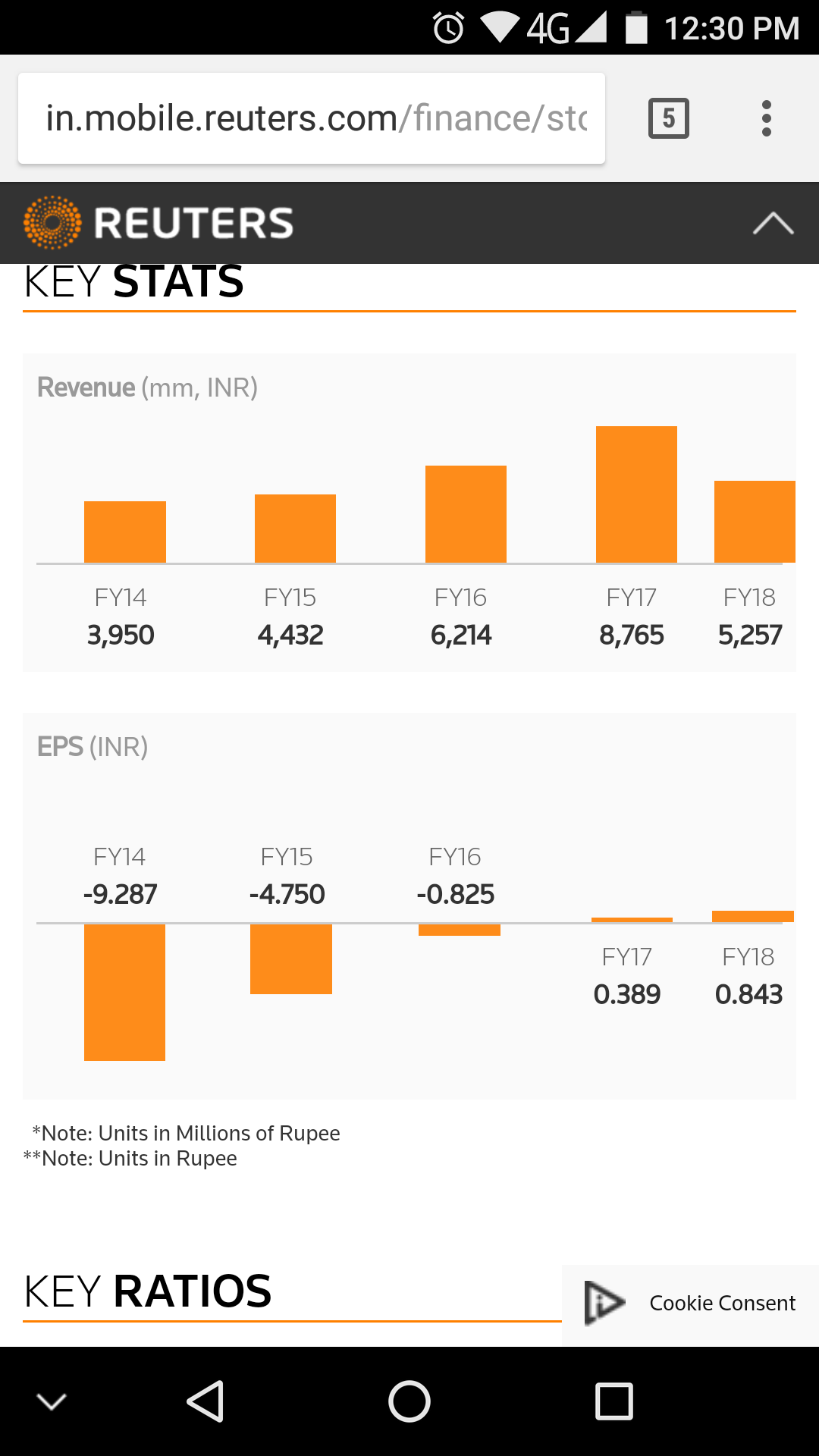

1)Sequent Scientific Ltd ::Sept quarter profit 305.4 million rupees versus loss 44.5 million rupees year ago.Sept quarter revenue from operations 2.65 billion rupees versus 2.29 billion rupees year ago.

-

first time after 2011; Declared interim dividend of 0.20 rupees per share.

-

company going turnaround slowly with all past investment resulted.

New Development:

- Sequent scientific arm alivira registers 3-products in Ukraine

**Competition Commission of India (CCI) approves Scheme of Arrangement between Strides Shasun, Sequent Scientific and Solara Active Pharma Sciences.

** Divesting women health business and concentrate only animal health , reduced debt…its market leader

→ CMP is stable close to 100 and should move up slowly.

Declaimer:

With all recent development and resulted turnaround financial performance, I have started to investment from CMP 98 and like to continue to buy.

5 Likes

Can someone pls give insight why this is not moving up post Q2. Is the pledged shares hurting this stock? Will it remain an opportunity cost? Today pharma ralliied including promoter related company Strides shasun

1 Like

Very disappointed with sequent and their management. Despite reassurances over the last few years that they will turnaround kept hopes high but now lost conviction. Why would someone buy a pharma stock trading at 80 x when there is an abundance of oppurtunity in market. Today biocons PE Multiple is 70 odd. Would much rather invest there given the approvals, earnings and track record. than keep hoping here. Sequent is a pure play animal health, so if you wish to give it a competitive edge of PE multiple around 25/30 then it still has a way to fall. Operators are possibly keeping it around 100 so pledged holdings are not compromised.

Very sad state of Affairs here!!

1 Like

Check out @shareduniaindia’s Tweet: https://twitter.com/shareduniaindia/status/945986949596270592?s=08

1 Like

The shareholder approval is just routine. Remember the profitable component is getting demerged into solara so Sequent will have to start from scratch as a pure player animal health.

It has reached the pledged level. Volumes have been very high in recent days. Hope the banks are not selling the pledged shares. Is anyone looking took buy this stock? Stuck at higher levels, wondering if I should average.