Hi Ayush ,

Please find the link below .

Hi Ayush ,

Please find the link below .

Why is this business trading so cheap? It has been producing good numbers recently and yet the stock valued at historically low PE.

It’s 8 years average PE is around 15 and current PE is at around 5!

Is the latest result having some exceptional component or is it just trading cheap because of lower liquidity in market and small caps in specific? If later is the case then this might be an opportunity.

The last of big individual investors Yodhan Sachdev and Paulastya Sachdev seem to have exited per latest Shareholding pattern. This, after the likes of Dolly Khanna, Porinju Veliyath etc had already exited. So now the retails and institutions only remaining.

Buyback worth more than 20 cr done at average of approx. 177 per share. Only 5 cr more worth of purchase remaining. Even after these many shares bought by company and dissolved, liquidity still not reducing.

Extremely good fundamentals with low P/E of ~6, excellent profit margins in the range of 60% for 10 years and improved production output, why is this stock not performing? When will the trend reverse?

Is it possible that buyback was a way to give exit route to big investors ?

Fundamentally nothing seems to be wrong. Price has held ground during this carnage. Financially stable and has good track record.

Invested.

Decent results

Company has still not moved to new tax rates

Rs 5 interim dividend

Oil from karjisan field is being sold at 30% discount whereas the discount is generally 2-3%. The output of crude oil has increased significantly and also the prices are being negotiated. Though crude prices are falling but looks like downside is now pretty much limited.

Approx 22 cr spent on buyback. I think company would still have close to 120 cr of cash and cash equivalents on books.

Regards

Krishna

So,

MCap : 215 crs

D/E : Almost zero

Book Value : 388 crs (Out of which 308 crs are from reserves and surplus)

Investment and C & CE : 150 crs

Contingent Liabilities : 0

Dividend Yield > 3 %

Sales : 104 crs (10 crs as other income)

PBT : 51.51 crs

ROE : 15%

ROCE : 15%

So basically you are getting a company in 65 crs which is generating 50 crs as profit before tax.

With NO contingent liabilities, debt to equity equals to zero and generating 100 crs as CFO.

This is all very lucrative numbers, can somebody tracking this for long time put some light on whats the catch (if there is one)

Even if you take EV of Selan as US$ 17.4 Mn, it has P 50 of 78 MMBOE and P 90 of 6.35 MM BOE which gives it EV/2P ratio of .2 , which is way less and EV/P50 ratio of 2.7 only.

There are huge reserves left to be exploited and with gas demand picking up, whats the upside ??

I have been tracking Selan from the days it was in 600 range. Invested at higher levels.

The problem is there Output from fields and hence Sales haven’t picked up as much as expected. Even though reserves are there, until they bring it out, no returns. On top of that, they lost major investors in recent times: Mahajan Family as promoter, Dolly Khanna, Porinju Veliyath, Sachdev brothers in recent buyback and so on. Further the crude price volatility not helping either. And to add to the woes, CEO has left recently, Indroda field lost from hands this quarter and so on.

Everything seems going wrong only.

Don’t take me wrong, fundamentals excellent, OPM of 50%+ and negotiation with IOC are all there. It’s just that the Golden days of Selan are not coming. It is extremely frustrating to hold on to…

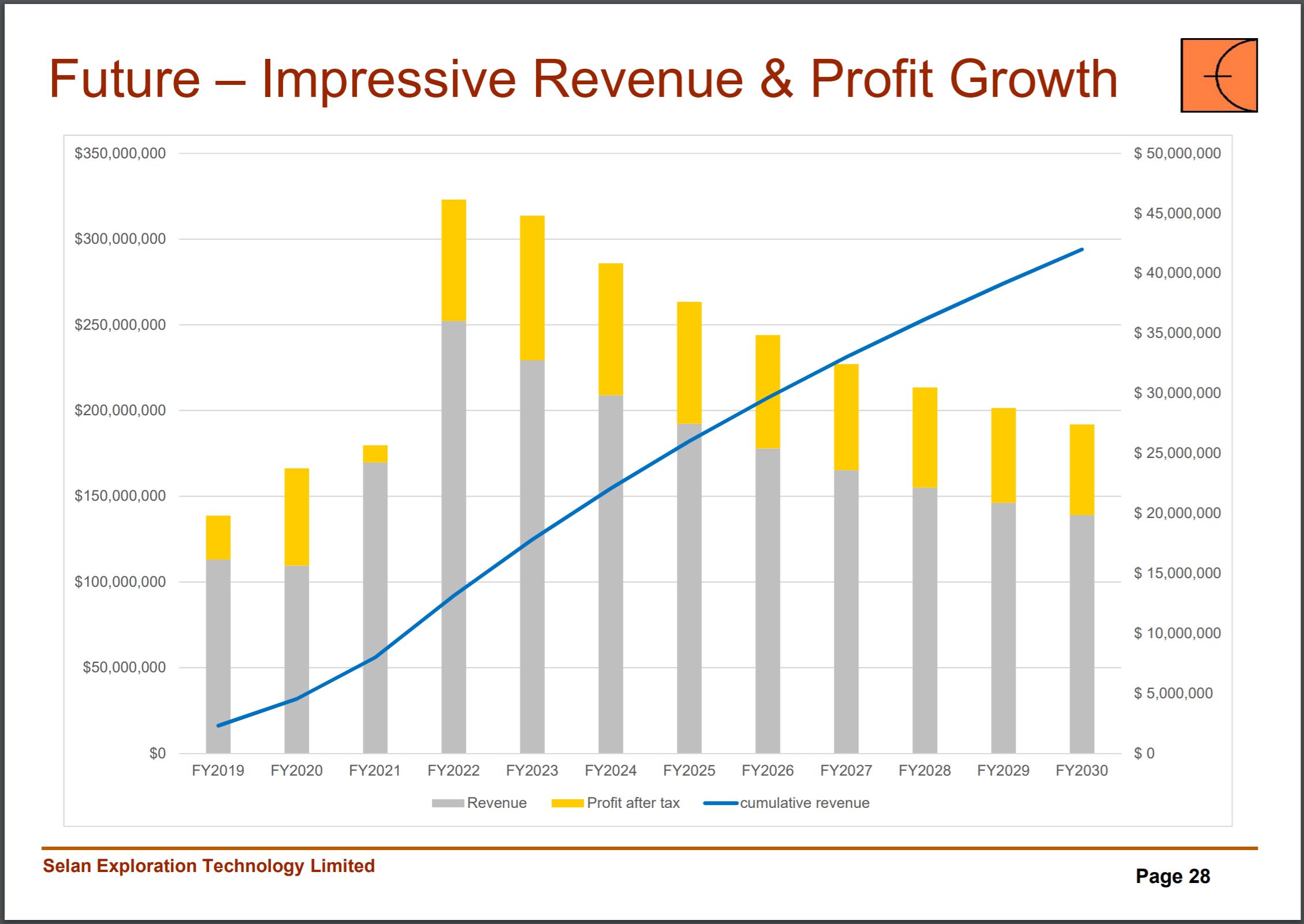

Has anybody gone through the investor presentation in details? Per their own projection, the company is saying that FY21 will have very low PAT while PAT will jump significantly from FY22 onwards? Does that mean we should exit now and invest in FY22 only? What’s really going on in this company?

The ratios that you shared are less, but consider you what benchmarks? Can you share? Also, if you don’t mind, can you share the calculations behind these?

Disc: holding for long, waiting for production ramp up.

Good Morning Everyone,

See, for oil and gas companies the first thing that I look for is EV/2P and EV/1P ratios and they trading at premium.

2p - this means possible + proven reserves. We assign 50% (P50) recovery possibility to these "possible"reserves.

1p - this means proven reserves. We assign 90% (P90) recovery to these reserves.

For Selan - 2P is around 85 MM BOE (78 MM BOE as possible and 6.35 as proven) while 1P is around 6.35 MM BOE

Taking EV as 17 Million

EV/2P : 0.2

EV/1P : 2.7

For many oil and gas companies, these ratios are above 2 and 15. ONGC 2P reserves are around 450 MMBOE to 300 MMBOE , you can calculate the EV value of ONGC (In Millions on standalone basis) and get the ratio. I will work out the ratios of other firms.

Though these ratios are not just the only criteria. What’s important is the effectiveness of exploration that needs to be studied. I need to study in detail about their rational behind those projections and best is to get in touch with the management. Will post once I have clarity.

Agree with @jigyasu_investor.

However, would like to add two red flags here (from screener)

In my opinion, one should not value this company based on comparable EV/1P or EV/2P multiple for 2 main reasons:

Thus, this method would lead to a significant overestimation of Selan’s equity. A cash-flow based valuation would be much more apt.

Latest presentation from company with lifting cost details http://www.selanoil.com/wp-content/uploads/2020/03/Corporate-Presentation-1.pdf

Recommend you remove the persons personal identification details like Email ID and Phone number

Mr Talukdar is Selan employee who has graduated as Mechanical Engineer in 2016. He is being too warmly treated by Selan management. ₹500000 was donated as CSR to his ‘Rajnusa Foundation’ for social welfare.

Any Update on the Bakrol Oil Field , why cant they partner with any niche Oil Player like HOEC or HARDY OIL , to improve there assets

just a thought i feel Vedanta Oil Division and HOEC , may surprise the market with there earnings Growth.