Neetu Yoshi Ltd has announced that its Board has approved raising around ₹27.48 crore via preferential allotment of convertible warrants at ₹104 each, subject to shareholder approval.Notably, Mr. Subodh Lohia has been allotted 6,00,000 warrants (~₹6.24 crore), making him the largest participant in this round; indicating continued confidence in the company.

@satishwe Satish ji, If you have studied or have office visit or direct input on ASM technologies. In Ems and semiconductor space, but promoters give no information. No orders are updated. No projects overview, no client name. All secretive for what reason. Mr Mukul Agarwal has big holding in it. Promoter is technocrat.

Anyone following this thread with some positive direct inputs, kindly share ,not investor presentation, agm or concall as i have seen that already. I am unable to figure out prominent area of their work and the scale now and ahead.

@Anuj I haven’t arranged any visits on my own, So far I tagged along others whenever possible, mostly based on networking and goodwill.

The more you give to the community you will find others willing helping you.

Also, most companies post such visits on the exchange. You could politely email the Company Secretary expressing your interest; sometimes they do accommodate requests. Additionally, try building connections with IR agencies - they may include you if there is low turnout and they need to fill slots.

That said, I don’t plan to visit any company, factory, or management unless I already know it reasonably well. As most of these visits eat up a lot of your time which you could spend on reading, no point visiting if you are not prepared for it well.

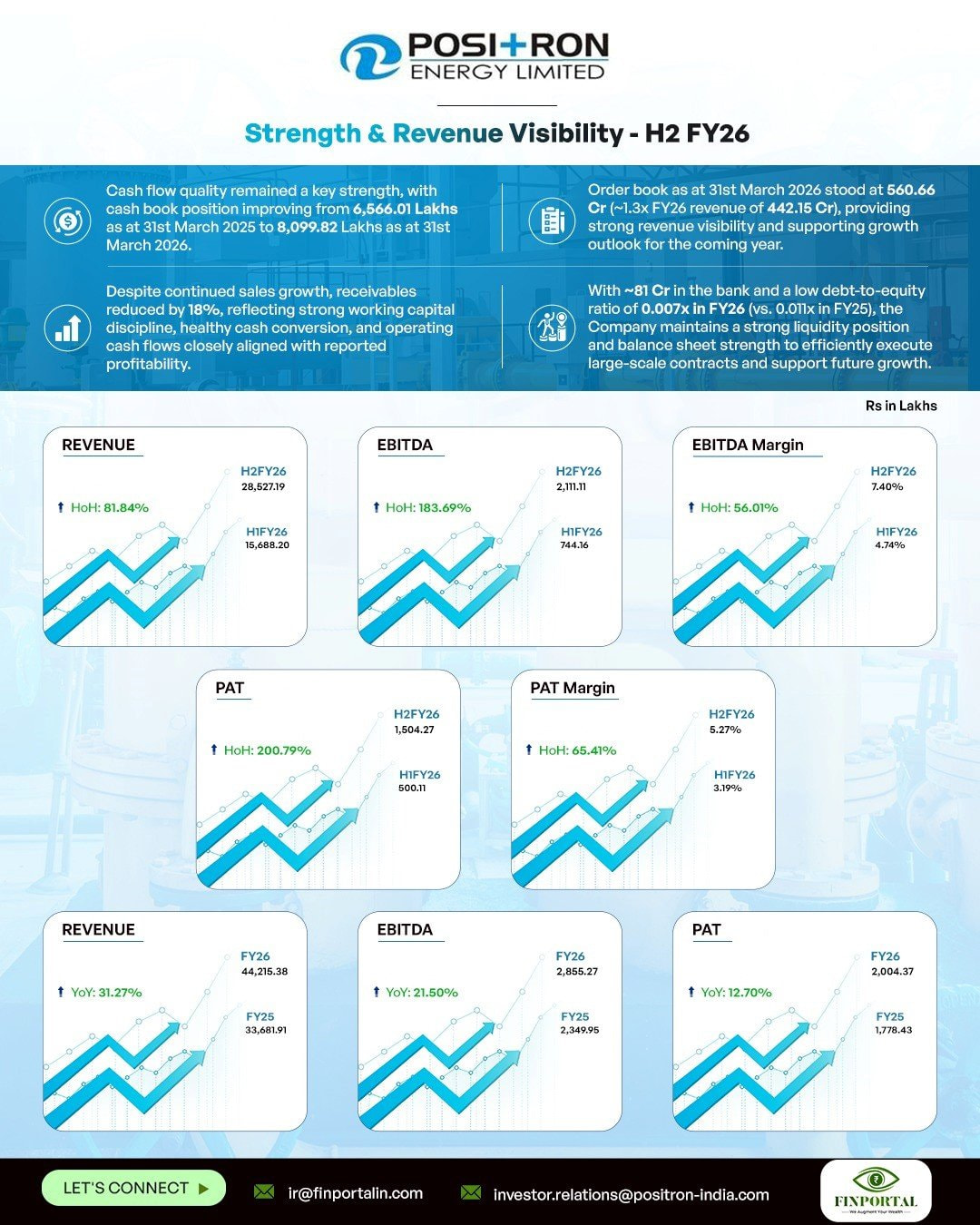

I don’t find strong recovery. It is misleading if you comparelast half year, but if you compare with March, 2025 then it is clear. Topline about 5 percent growth. In the bottomline there is some growth. But there is drastic reduction in employee benefit both from 9/25 and 3/25 level. After recent labour law changes , every company is reporting rise in employee benefit expenses. How come this company is showing reduction? Moreover, it is in natural gas business and actual deterioration in supply started after March 2026. So this result don’t show true picture. True picture will emerge on management con call or in half yearly result of 09/2026.

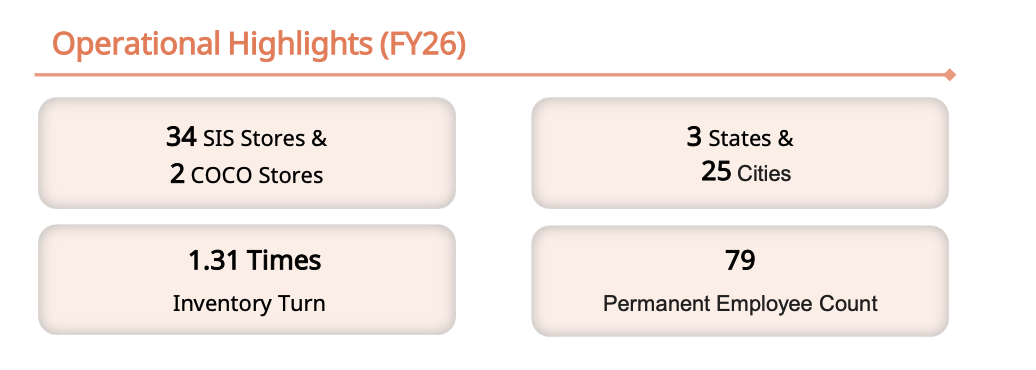

Fy 27 and fy 28 guidance , 30% SSG , 15 new EBO for 24 moths ( 6-7 in fy 27), Expect to generate 9-12 cr at maturity per store ( i guess they meant break even) , for Maharashtra break even is 12 months and Rest of India 24 months on the upper end of time frames.

The 6-7 stores from FY27 will reach maturity, contributing roughly 60 to 75 crore.

FY26 SIS Base: 350 cr

FY27 SIS Projection: 350 crore × 1.30 = 455 cr.

FY28 SIS Projection: 455 crore × 1.30 = 590 cr.

Average billing size grew 41% yoy, from ₹85,000 in FY25 to ₹1,20,000 in FY26.

Gargi focus on lower value diamonds H, I colors, REVA is into higher value Diamonds of E, F colors.

35 cr marked for marketing for 24 months for 15 new EBO stores.

For Growth beyond 2028 ( as ipo money if market fro fy 27 and 28 only) , headroom is 200 cr unused debt plus internal accruals of some 60 cr in fy 26. No plans to dilute equity until fy 30.

NOTE : If I recompute these in numbers we get the below data ( management didnt give the exact absolute number , they asked investors to calculate themselves )

Revenue Segment

FY26 (Actual in Cr)

FY27 (Projected)

FY28 (Projected)

SIS Network

350

455

590

New EBOs

-

25

97

Other (Existing EBOs/Gold)

89

110

140

Total Revenue

439

590

820

EBO Unit Economics:

20-25 cr per store capex cost.

Revenue and Profitability ; Sales 3 lakh per day ( 9 cr per year), 30% Gross margins , ebidta around 1.5 , after 3-4 ebidta expected is 3.5 Cr.

Inventory of 10-20 crore depending on store size.

The company’s overall inventory turn stood at 1.31 times for FY26

How do you guys look at the recent preferential announcement by Neetu Yoshi? Their earlier commentary conveyed to the effect that they don’t need to raise funds for some time to come.

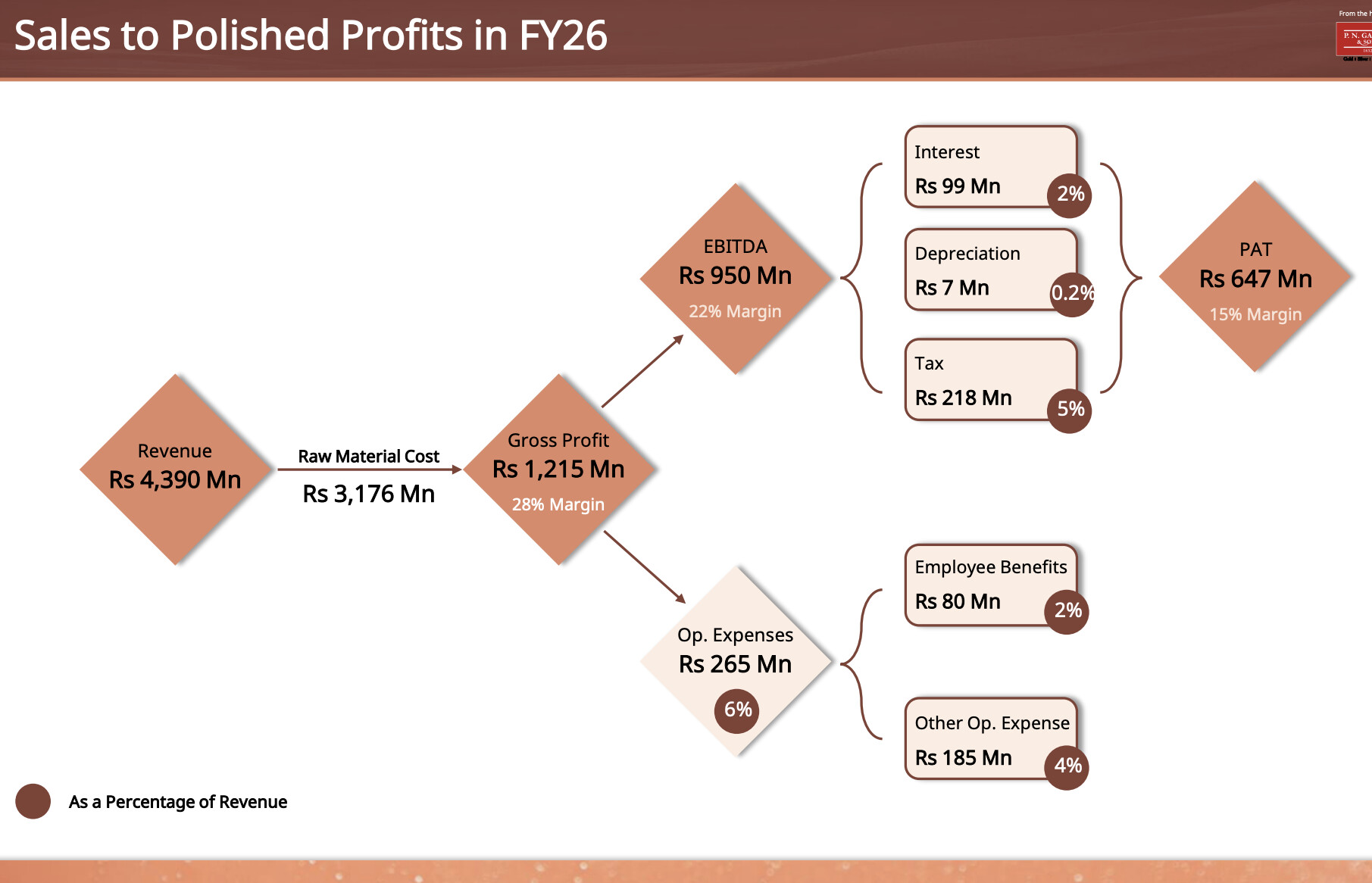

About PNGS Reva - Promoters are buying lots of shares from open market/block deals. In March 26, promoters bought 8,76,424 shares and in May 26 (till 18th May), they have purchased 3,22,000 shares.

It is interesting to note that IPO which came in last week Feb 2026 was entirely fresh issue of 98 Lakh shares. This means promoters did not sell a single share during IPO and are buying large quantities post listing in open market. This is huge vote of confidence shown by promoters.