It will be great if you can answer one more of my questions relating to political risk.

Is it possible for a particular state government to impart control over the lendings made by the MFIs?I.e. waivers of loans types.

What I understand it won’t be that easy for the govt. these days after RBIs involvement.

As long as they remain as “NBFC-MFI”, there could be political interference. But with active RBI these days and with passage of MFI bill, these risks would come down. Also, MFI industry does a lot of good for its customers who otherwise have to fall prey to loan sharks. RBI as well as government knows this very well after the AP fiasco. Recent call money scam in AP must also do a lot of good to MFI industry as people would get to know about MFIs who lend with proper regulations in place.

Once these NBFC-MFIs get converted to small bank finance companies and later into universal banks, the political risks will die down. But, for me personally, the moolah is in MFI lending as long as you can keep the NPAs in check and follow proper risk management principles.

Any investment is fraught with inherent risks, we need to take a call weighing the risks vs. reward, according to one’s own risk taking ability and knowledge of that particular sector.

I could find this article, it is old 23/Sep/14 but it says that Central Govt. bill tabled in Lok Sabha in May-12 was rejected by the standing committee on finance. Therefore is right to conclude there is no law governing MFI till a bill is passed by Parliament.

RBI is a regulator which regulates NBFC-MFI and not the MFI registered as society in the States.

Therefore it may be right to speculated that NBFC-MFI may be less susceptible to State Govt. interference.

Key Points from the link:- 1."Afterthe AP crisis, RBI has handled the sector very vigilantly, carefully and very thoughtfully. The kind of policy and intervention that it brought in to satisfy all the critics of microfinance is really commendable. It gave a framework, brought in a different setup for NBFC-MFIs and now it is regularly reviewing the quality as per the requirement and the fact that Bandhan got a banking licence and RBI came up with the small bank concept, encouraging MFIs to convert themselves, shows that RBI is serious about the sector,” said Dibyajyoti Pattnaik, director at Annapurna Microfinance Pvt. Ltd.

2. Ind-Rabelieves that competition from Jan-Dhan-driven bank credit, given that banks would provide overdraft facility to account holders, may hamper the growth of MFIs as loan demands take a hit. While**Annapurna Microfinance’s Pattnaik says,"Idon’t see competition; rather I see these as complementing one another as the space is so large. There is still space for innovation and because there is a large population of the country is out of the formal financial network, the only way forward would be through microfinance."

*3. The report by Ind-Ra points to this contingency indicating that RBI rules have transformed the policy to favour the incumbents. The report indicates that the gross loan portfolio of large MFIs has increased from 79.6 per cent in FY14 to 83.2 per cent in Q2 FY15 while that of small players decreased from 3.4 per cent to 2.6 per cent for the corresponding period.

4. The report also mentioned the high barriers to entry which has constrained the MFI sector.

Sorry Anand, missed out that the shares were listed on NSE 4 months back.

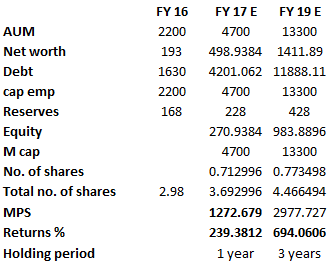

Till what I understand -

Assumptions -

1). Debt - Equity ratio is constant and is of 8.42:1 (from screener)

2). Company shall be diluting its share capital every year to pump in fresh funds to increase AUM. Fresh equity will be issued at the then CMP.

3). Stock will be fully valued in coming time, hereby AUM/Mcap will be 1 (like SKS microfinance).

4). Reserves for 2017 and 2019 includes expected profits of 60cr and 200cr(80 for 2018 and 120 for 2019) respectively.

5). Estimation of AUM of 4700 and 13300cr has been based upon the info gathered from the religare research report attached by jatin.

Request people to cross check and suggest any modification here.

Ujjivan Financial Services - an MFI has filed for IPO.

In due course I expect Equitas and Janalakshmi MFIs too to get listed on Indian bourses.

This should help Satin Creditcare narrow the current valuation gap between SKS and itself depending on valuations accorded to these IPOs. The bigger SKS is trading at 6 times the market cap of Satin Creditcare at current prices. While SKS is a market leader in South India, Satin is a leader in North India in most of the states it operates in.

Should we value such companies basis PEs or AUM/M.Cap?

If AUM/M.Cap, why the same and not PE?

Satin and SKS both are trading at PE of 26-27 (odd levels). But, based on AUM/Mcap - Satin is undervalued and SKS is perfectly valued. What is correct?

When I feel AUM/Mcap - I see an issue. A company having high AUM but generating less profitability (OPM and NPM) tend to have lower Mcap compared to an equivalent peer (having same AUM but more profitability). In that sense satin having lower mcap is justifiable (having less margins compared to SKS). I might be wrong, but just want to understand.

I think it depends on the cost of capital also. Better cost of capital for SKS and the least loan interest rate in the market(as they claim) with highest profitability suggests that the business is far better than Satin (assuming what you have said is right). So, if the company is in the same sector, doing the same thing in a better way, deserves better valuation than other company. Remember that AUM can become NPA with a blink of an eye with the sector we are talking about. I think risk management of SKS must be better than Satin and that is why they are getting cheaper loans than Satin. Just trying to add something to the discussion.

General points, not that you all do not know, but may be a reminder -

More money is made by arriving at what future would look like based on past data. The increasing slope of various metrics like RoE, RoA, OPMs, Operational leverage etc. is more important than absolute numbers. If they likely converge in future, there will be re-rating.

Betting only on past data for comparing 2 companies is half the analysis. If you have an edge by reading the industry analysis, you can foresee what others who only depend on research reports cannot and that is a real edge to bet big!

In NBFCs, scale brings ‘operating leverage’, reduce cost of borrowing and also get a better credit rating. If you are on the right path, credit rating improvements come and along with it the reduction in cost of funds. Getting cheaper loans is also a function of your credit rating profile.

SKS Micro would also do well (I’m positive on microfinance as a sector as per the current situations), but you could have bet on SKS when it was languishing at 100 per share by predicting rationally the improvement in its metrics over the past 2-3 years.

SKS Micro has deferred tax ‘assets’ due to its past losses which it can use slowly to reduce its effective tax rate.

It is like Repco vs. Gruh 3 years back to an extent.

Read the report by Religare which was shared earlier, it has all the necessary information.

Having said this, you need to be aware of the risks present in the sector and risks particular to the companies which you are tracking. Whenever the risk vs. reward is skewed towards you irrationally, make an investment.

Edit: SKS Micro came with very good set of results which goes to show that microfinance sector would continue to outperform and its business would be insulate to global conditions.

I am alright with getting 50% CAGR as SKS is doing, if they are disbursing loans carefully(they learnt from their mistake).

Agreed but in this segment I think I would go with the company which is well settled and well diversified (as mentioned in Religare report) and which has ROE of 20.

As I said, the company is in the sector where one big drought (we have had 2 recently) can screw up the things pretty badly. So the improvement hypothesis needs some time to pan out, which the company might or might not get. (randomness you can’t control).

Yes SKS Micro has deferred tax assets to the tune of 600cr and I think that can cover taxes for a lot of years to come. Presently, they are paying taxes at the rate of 23%. I just checked their results which came today.

I agree to that. What I like about Satin is there tie up with Yes and RBL. Religare pointed out about the book value to market price as a negative for SKS but I think that number is comfortably defied by HDFC Bank for long time. A lot of companies till a few years back use to give sell rating on HDFC bank just on that parameters.

Religare’s estimate of EPS has gone for a toss. The were expecting an EPS of 18 for this FY but they will be reporting around 24 this year.

I think concentration can act as a boon as well as a bust. I tend to believe in diversification more.

I might have missed a point here and I would love to hear some key differences or positives of Satin over SKS.

Disc. Invested in SKS from 440 levels and it forms after this recent correction 10% of my portfolio.

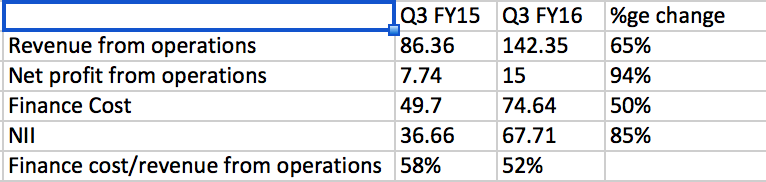

Satin Creditcare came out with the results and they are outstanding and I was expecting such increase in profits anyway given the scorching pace at which the selective MFIs are growing. I think they are the best results that I have come across so far, except for increase in NPA provisions. I believe this quarter most banks and NBFCs are proactively providing a buffer for provisions which I think are reflected in increase in provisions.

I think, I should reserve further adjectives and not go over board given the turbulent times, sentimentally speaking.

Given the results of other companies, I think home finance companies (selectively) and MFIs (selectively) have shown relatively much better results and should most probably the first ones to recover given the quality of earnings and the visibility. Selectively is the key word here.

On any other day, I’m sure such results would have been welcomed with good uptick, but not today! Excellent results are given mild correction and bad results are handed out with deep correction and worse results, let’s not talk about them! The company has converted quarter of the warrants issued last year at a price of 130 (against SEBI mandated price of 105, which is a sign of good corporate governance as warrants are issued above the mandated price)

65% increase in revenue from operations. 94% increase in profit after tax. 85% increase in NII (Net Interest Income).

The EPS for 9M FY16 is 13.39 vs. 9M FY15 EPS of 8.23. Full year FY15 EPS is 11.93. The company is likely to end the FY16 with an EPS of around 20-21. Q4 is the better quarter.

The provisions are higher by ~6 crs this quarter than the previous quarter. Provisions are four times of the previous quarter number, while revenue increase by ~13%. The jump in provisions led to flat net profits of ~15 crores quarter on quarter, in-spite of a healthy increase in revenues. Had the provisioning been at similar levels, the profit would have been ~19 crores, that is, 25-30% higher.