Housing sales fall 31%, launches dip 40% in Dec quarter: Report

The stock of unsold houses however fell marginally by 1 per cent to 4,53,592 units in Gurgaon, Noida, Mumbai, Kolkata, Pune, Hyderabad, Bengaluru and Chennai from 4,59,067 units in the previous quarter, said PropEquity, a real estate data, research and analytics firm.

I doubt about reliability of HFC stock price rally and euphoria

You can have excellent loan growth in any landing bussiness but the most important is asset quality and NPA over period. Current loan growth without improvement of borrowers repayment capacity could result in NPA. Don’t forget RBI’s 90 days flexibility to recognize NPA. Q4 and Q1FY17-18 will show real picture

Bank GNPAs may rise to 16-17% of loans in 1-2 yrs: Credit Suisse

At the end of Q3, a whopping 41 percent of corporate debt is with companies whose earnings are less than their interest outgo. Credit Suisse’s MD and Head of Research Ashish Gupta shares his detailed analysis with CNBC-TV18’s Latha Venkatesh on a special show - Indianomics.

The cycle of HFC: Easy money at lower cost available to landers (HFC/NBFC/MFI) without any restrictions due to ample liquidity in syste >>>> all landers have money to deploy and want loan book growth >>>> landers need to find opportunities to deploy the money to borrowers in cut throat competition >>>> borrowers take money as it available easily without much check on repayment capacity. Now when liquidity dry out…Landers growth depends on collection from borrowers…borrowers repayment capacity doesn’t improve…default…NPA on lander account

this is backward looking with no new data, as credit agencies are known to be. key question is how much they can recover. Satin CEO in ET interview last week said UP collections were at 92%.

With Farm loan waiver looming this is the period of maximum pessmism for Satin in my view.

I think the story is playing to script, I expect March quarter will be the bottom and recovery will start playing out in June quarter. Issue is two fold - one disbursements have dipped dramatically and two collection efficiency numbers are worse than how they are being presented. On an absolute basis I reckon there is a hit on the other income, due to loss of securitisation income and hit on TSPL’s book as well.

For March quarter I estimate a dip in AUM, fall in other income, large provision hit ( I reckon a 10% hit on AUM if they were marking it to actuals and not taking the RBI window, even otherwise I dont see how they dont take atleast a 5% hit.

I suspect they will want to use this as a dumping quarter and get all the bad book out so June can be fully up and ready.

I am hoping the market will give us nicer entry points.

From the recent mgmt interview, we can get an idea that the situation is improving gradually post UP Elections, with collection efficiency right now at 90-92%. As per Mr. Singh, within the next few months (one-two), Satin collection efficiency will be back to pre-demonetization levels. Probably we all know that Q4 won’t be good, as Jan-Feb weren’t good due to state elections and demonetization. But things are improving on the ground.

ICRA outlook is not a news, and is something that is already been reflected in the share price. There might be some more downside, who knows, due to probable poor q4, but if we look ahead, Satin can attain its past growth trajectory (and that too in a much more vigorous manner with online disbursements coming mainstream, new home finance segment coming to speed, and much more regulated MFI industry framework with lesser interference from states).

Regarding farm loan waivers, mgmt commented that these issues are kind of difficult for them to make the borrowers understand the differentiation between them and organised financial institutions…the public sector and the private sector. This would depend on how they navigate through this. There might be some initial hiccups, but this should be okay as time passes by and as the borrowers understand the difference.

Regarding BJP coming to power in UP, management is optimistic about company’s prospects as BJP had “financial inclusion” as their main election theme. So, this is going to play out well for MFIs.

Regarding disbursements and guidance, mgmt gave guided for 5500 cr AUM by March 2018 (at present, it’s 3200 cr). They are much ahead of the curve, as disbursements are picking up big time in Feb and March of this year (700 cr). Dec/Jan were sort of aberration due to obvious reasons, when they did close to 100 odd cr disbursements. They are projecting close to 60% revenue growth in full fiscal 2018.

Company has well liquidated with CAR close to 30 odd percent, and promoters and fund houses are willing to buy more (subscribing to preferential shares and warrants) at 415/450. Not to forget QIP at 550 odd levels to raise 250 cr in October last year.

Would be interesting to see how Satin manage NPAs going forward. Mgmt was pretty optimistic that there might be some more releif coming from RBI in regard to this (any rating downgrades can lead to increase in lending costs, which may negatively impact large segment of borrowers dependent solely on MFIs like Satin). RBI must take cognizance of the fact!

This to me looks like a very good investment from a risk-reward perspective from these levels going forward. Business fundamentals are in tact and the runway seems long, especially due to Satin being present in states which are least penetrated as far as MFI industry is concerned. Buying a good company in distressed time (not owing to its own fault) is what is value investing. It has got good value if you look one year ahead.

Agree with all you mentioned but where I disagree is that the current price isn’t reflecting the challenges in the current biz model.

With Dec book value at 680 crores and March quarter not expected to really contribute much PAT, it is safe to assume March book value will be the same.

Private deals in the the micro finance space of similar scale as Satin are happening at ~2x book even if they have much more diversified books and are now banks.

In my opinion, satin should correct to these valuations to reflect its weakened position which would imply ~1300 - 1400 crore market cap (2x book) which is where it trades today i.e stock is at fair value.

A 10-15% correction from here which would imply stock correcting to 300 - 325 levels where value starts to emerge from a 1 year hold perspective.

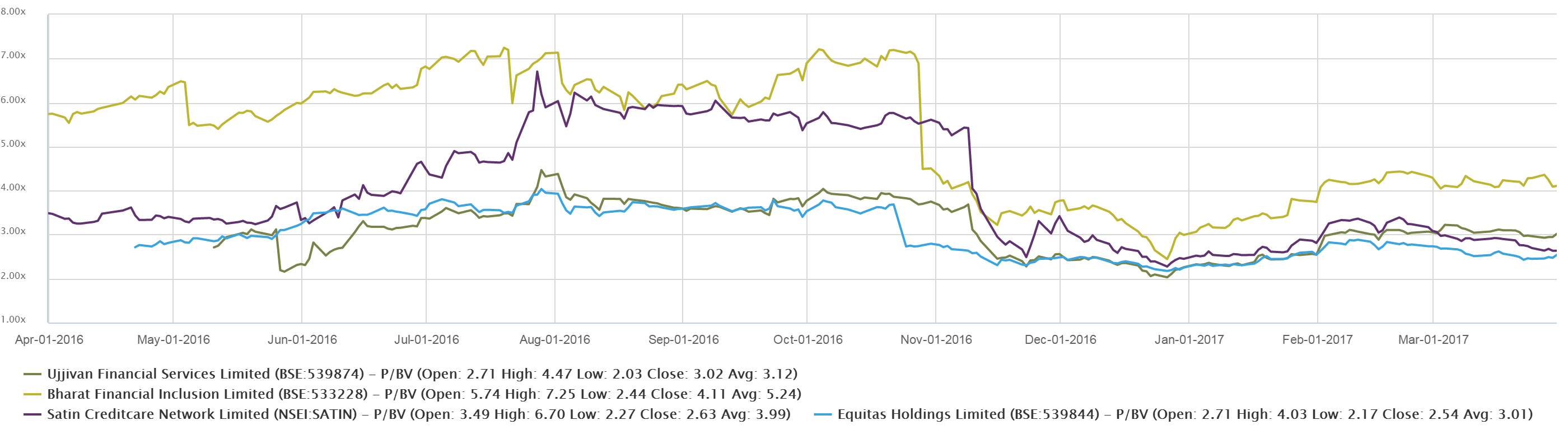

All 10 small finance bank applicants have raised money in the last 12 months. Barring Ujjivan and equitas which went public others ended up raising private capital from largely domestic sources.

What i said in my post is that it can still correct post q4 result, but that should be the bottom. I completely agree that we can still have 10% correction (if the market corrects from here, or if q4 result is poor). Though, regarding value, i am already seeing good value emerging even at these levels. Valuation it will fetch and the p/b it can command is rather subjective (depending on bear/bull market, and peer valuation). Currently, SKS is trading at trailing 8.3 (understandable, being market leader), Satin is around 4.1. I would just like to look one year ahead, by when they are predicting 65-70% AUM growth. Also, the reason i see good value emerging here is their presence in north India where the states are highly under-penetrated, so the runway is longer. On the contrary, in southern state, where many of its peers are operating are getting saturated. This is advantage Satin!

That is a contingent event. I wouldn’t bet on M&A valuations. There aren’t too many buyers out there, and I wouldn’t want to punt on Kotak or Indusind getting excited about this one.

Also we should be careful on using latest book values to make this work. SKS trades at 4.1x Dec 2016 book value while Satin trades at ~2x along with ujjivan and equitas. SKS will command a premium on account of its market leadership superior ROEs and diversification.

In my head, fair valuation for this sector is 2.5x - 3x P/B (~12-15x P/E at 20% ROE) given the basic fragility of the business model inspite of the high growth and ROEs.

Once the business cleans up the deometisation mess, it should settle down at ~600 crore book value and then raise some equity from there to trade at ~2500 crore market cap in the next year which would imply share price rising ~2x from here (unadjusted for dilution, so actual rise may be 60-70%). I am definitely a buyer, but just think that the flow of bad news will create better entry points

Book value will rise going forward, company has good presence in North, growth has come back already, waiting for results will not get you bottom as current prices are also very good. I hold all three ujjivan, equitas & satin, all three can double topline by 100% in 2-3 years.