Welcome news! This will enhance liquidity in stock -

Sarla Performance Fibers Ltd has informed BSE that a meeting of the Board of Directors of the Company will be held on August 12, 2015 to consider sub-division of equity shares -

Company has informed BSE that the Board of Directors at its meeting held on August 12, 2015 has approved Split of face value of ONE Equity Share of Rs. 10/- each into TEN Equity Shares of Rs. 1/- each subject to the shareholder approval.

Heard that the company is totally promoter driven. Any idea about the forward plans for succession/ innovation beyond the US plant.

Also i am also getting skeptical about the scalability of commodity polyester business in US where they further plans to expand.

Actions of management are not indicating anything about ‘promoter driven nature’ -> Management is paying dividend, expansion is conservatively financed, salary numbers are in check, information disclosure and response to investor query is swift. Where did you ‘hear’ that company is promoter driven -> any meaningful instance?

Re innovation beyond US plant -> US plant is big trigger underway. I endorse management strategy of not spreading themselves too thin by first getting US strategy right and then focusing on next big idea. By the way, Nylon 66 is also on cards but in very infancy stage right now.

Scalability of US business is the call to be taken. But from management discussion over investor concall and numbers for US business indicate all is on track.

Just to highlight company is not any other commodity polyester business as they have enjoyed healthy margins over last 10 years - this was highlighted on investor con call as well.

Hi Pratik Vora,

Missed ur prompt reply. Thanks for replying.

What I meant by promoter driven was that the whole control of key strategic decisions is with Mr Krishna Jhunjhunwala, I have recently met the CFo of the company and I also got the same sense.

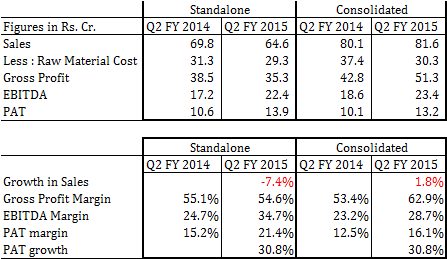

Q2 FY2016 results are out : strong improvement in gross profit margin (all thanks to USA plant) and hence meaningful PAT growth of 30% y-o-y and q-o-q both. In fact, PAT growth is so strong that H1 FY2016 PAT of Rs. 23 cr. is ~42% higher than H1 FY2015 PAT of Rs. 16.5 cr!!

Key questions which come to mind -

Why is there no sales growth from India plant?

Gross profit margin at USA plant seems very high. Are they sustainable?

For FY2016 guidance, it seems management will over achieve its PAT guidance very easily. However, will it be able to achieve sales guidance?

Are we on track to start commercial production of Nylon 66 plant at Silvassa?

The big client from USA, who had approved yarn package supplies from Sarla’s USA plant, did that dialogue progress?

One of the positive factors in recent time is increasing gap between cotton prices and polyester prices. Though cotton prices fell but fall in polyester prices was more steep as it is crude derivative. Polyester is raw material for Sarla. Yes Gaurav, you rightly pointed out about crude tailwind benefits to Sarla. But historically (last 10 years), Sarla has enjoyed 45%+ gross margin, management is of the view they sell value added products which gives them these high margins. In addition, USA plant is also adding to margins as it is stabilizing.

But yes, will surely take your point on concall about volume and realization growth. Thanks

Minutes of concall (note - had to be in/out of concall due to some work)

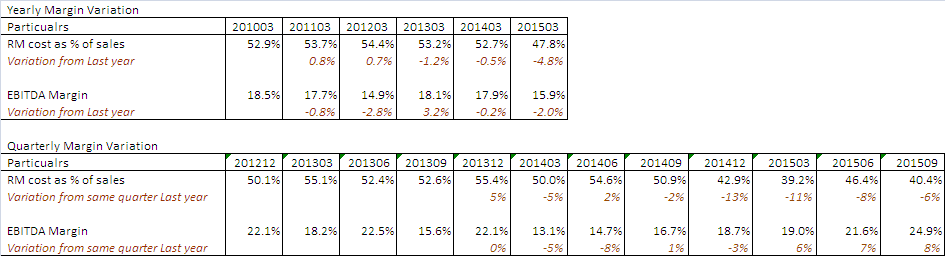

Volume grew marginally by 4% y-o-y

USA plant has broken-even

Company is enjoying gross margin expansion due to crude price fall. Gross margins for H1 FY2016 have been 62%. However, historically gross margins have been ~52%, which is also very appreciable

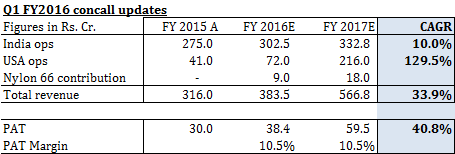

Nylon 66 plant commenced operations. Full year sales from Nylon 66 is expected to be ~INR 15 cr. hence, contribution to H2 FY2016 is INR 7.5 cr. 2 shipments already made till date

RM/sales ratio is USA ops is 30% implying gross margin from USA plant of 70%!! RM/sales ratio from India ops has been ~50% over last decade!

For H1 FY2016, India capacity utilized = 4700 TPA and USA capacity utilized = 1900 TPA

Training manpower in USA ops is creating delay in USA plant’s ramping up

Guidance for FY2016 sales of INR 350 cr. and PAT of ~INR 46 cr.

I am using the Nylon 66 thread now and let me tell you, there is no one who cam make ropes like the ones made by Sarla Flex in the US. There are top quality and as their usage in human life goes up, so shall the stock price, they have just started the US thing and at 59 I took a sizeable position. I am expecting that after these umbers posted in Nov 15, the company can do wonders over the next few quarters till 2020 if it goes to 100% capacity in US too.

Prashanth Jain and Kenneth Andrade have a positive view on this too, just a matter of time before they get in.

If you see the quarterly variation, In the last few quareters the benefit of the lower raw material margin is not flowing in the EBITDA (Because of the operating loss in US plant) but in the last 2 quarters, we can see the full benefit since the plant is broken even. Am i correct to assume if the raw material cost stays the same then the margin will only improve but not go down from this level? What should be the comfortable margin level for the company in the future (Since the US capacity will utilize further)?

Great work Pratik. Some excellent numbers here over last two quarters. The only issue in my mind is the volume growth. Is there a possibility that the Indian business has been shifted to the US plant which caters far better to the clients. The sales of US plant might be at the opportunity cost of the Indian plant sales. Pratik your insights on this issue would be really great.

@ateek_balesaria

Great analysis ateek! As per your working its quite apparent that the utilization levels of US plant is a key factor.

Adding to your point, as per the recent Concall, management too admitted that any increase in utilisation levels will benefit margins.

Though they are preparing themselves for the US market, the utilizations will kick up,say, from next year.

Nylon 66 (with the higher margins) will add to the sales in this Qtr and that would be an additional impetus.

Expect utilization of around 65-70% from Nylon 66 by the year end (ref : Concall).

So, I feel its gonna be the margin game.

1). De- growth at India plant level. This is partially offset by growth at US plant level. But consolidated level sales still is lower than the last year sales. The PAT/EBITDA expansions are not sustainable if the sales doesnt increase.

2). Company has a JV in Honduras (Central America) - where a litigation is going on - and company has decided to discontinue this JV - reference - investor presentation - you can access it on its website. Do not know what exactly the issue is.

3). Company has negative operating cash flows - but on digging further found that it is not of worry. Rather the negative cash flows are because of loans and advances given to subsidiary in US and for advance given for Dadra Nagar haveli plant. These items should have been classified under investing activities (A presentation related issue only).

4). What is the market size of Nylon 66? What is the entry barrier?

@ ateek and abhishek, thank you for your kind words.

On big order at USA plant – Company has dispatched sample quantity to clients and waiting for their revert (reference concall). My understanding is it takes ~2 quarters for test samples to crystallize into final orders. So they might flow in Q1 FY2017

Yes, it’s a fair assumption that if crude stays at same level then margins will at least stay at same levels! Numbers support this hypothesis and I had asked this question on Q2 concall also specifically.

On shifting of orders to USA plant, not sure if this is happening. However, in that case actually margins will bump up as in USA for commodity products also RM/sales ratio is 30% i.e. gross margin of 70%!

I share the concern on flat sales. But only solace is that management candidly admits (and financial numbers also stand by it) that they are focused on profitable franchise rather than sizeable franchisee.

Sarla Performance Fibre was presented award at Karur Vyasa Bank - Dun & Bradstreet SME Business Excellence award under “Mid Corporate” segment in Textile category at the hands of Mr. Jayant Sinha - MoS Finance. I watched it on CNBC TV yesterday night. The news is here. But it does not spell out list of awardees