Hi All, company has come out with outstanding set of numbers for Q1 FY 2016. Below is the quick analysis of numbers -

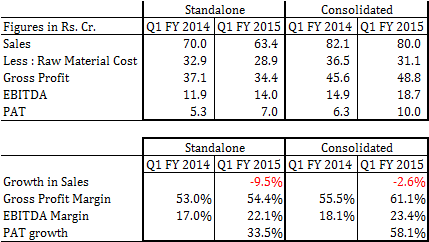

+5.1% and +5.3% y-o-y improvement in EBITDA margin in standalone and consolidated resp.

+33.5% and +58.1% growth in PAT in standalone and consolidated resp.

very sizeable improvement in gross profit margin

It is important to track following things now -

- how is the USA plant picking up - expected capacity utilization this year and hence revenue. And how has been client reaction for supplies from USA plant?

- are the margins sustainable (gross profit margin and EBITDA margin)

- Is relationship with Hanes auguring well for business at USA plant ?

- Co. expected to sign up major client by Q1 FY2016 (as indicated in Q3 FY 2015 con call) - any update

- any plans to increases capacity at pilot plant set up at Silvassa for Nylon 66